After leading the market for much of the year, defensive stocks such as consumer staples and utilities have been sliding since mid-summer. The S&P 500 Utilities Index is down 10% from its July peak, while consumer staples companies are down 6% (source: Bloomberg). Minimum volatility strategies, which often emphasize these “low beta” names, are also underperforming after a strong start to the year.

Given the recent retreat and more reasonable valuations, should investors be giving these sectors another look? Not yet. Here’s why.

No good bargains after all

Utilities, consumer staples and other defensive names are still expensive relative to their history, and in many cases, their fundamentals. Large cap utilities stocks are trading at a premium to their 20-year average relative price-to-earnings (P/E)and price-to-book (P/B) ratios (source: Bloomberg). For example, over the past 20 years the S&P 500 Utilities Index has typically traded at around a 25% discount to the broader market. Today the discount is less than 20%.

Nor do the valuations look any better when adjusted for fundamentals. Comparing U.S. consumer staples stocks to the broader global market based on profitability—one of the factors that investors usually note to justify the premium—these stocks appear to be some of the most richly valued in the world.

A modest rise in rates could bring hurt

I believe we’re in a “low for long” world, with interest rates unlikely to revert to their pre-crisis norms any time soon. That said, it will not take a sharp rise in rates to inflict more pain on the defensive stocks; even a small increase should be enough.

While utilities and staples companies have always been valued for their steady, reliable yield, the dividend on these stocks has become even more important in a low yield world. “Bond market refugees” have been flooding into these sectors as one of the last bastions of a +3% yield. This trend has exacerbated the sensitivity of these stocks to even a small change in interest rates.

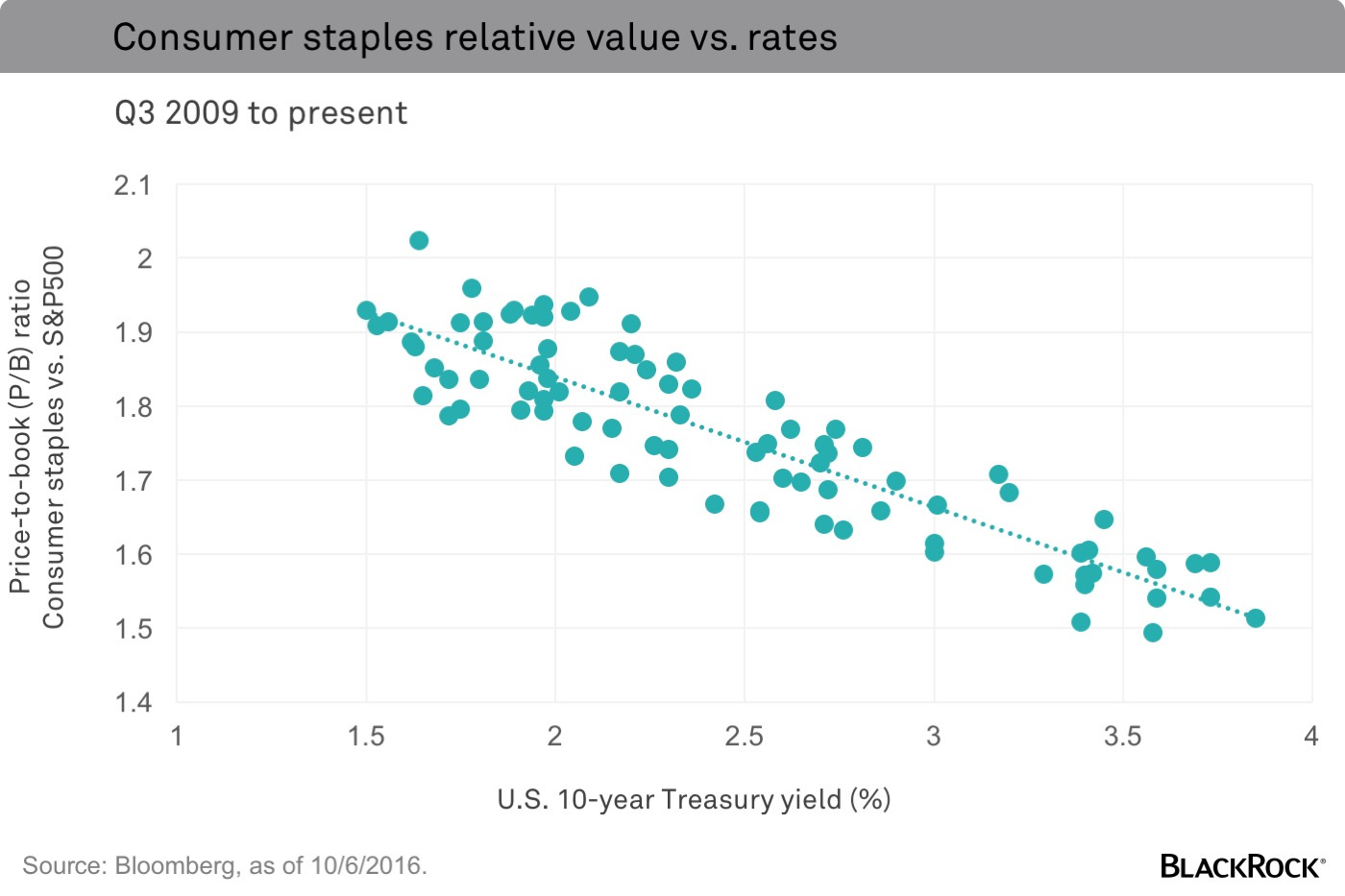

Since coming out of the recession, the rate on the 10-year Treasury note has explained roughly 80% of the relative value (the P/B of the sector versus the P/B for the S&P 500) for consumer staples companies. See the chart below. It won’t take a return to 5% on the 10-year yield to push the sector lower. Even a 50-basis-point backup in rates (0.50%)—which would put the 10-year yield back to where it started the year—would likely put downward pressure on valuations.

At some point we will likely see value return to this segment of the market, but we’re not there yet. High yield, low beta stocks remain vulnerable based on still elevated valuations and hypersensitivity to even small changes in interest rates. I see better value in other sectors such as technology, which are reasonably priced and better positioned to grow in a slow growth world.

Russ Koesterich, CFA, is Head of Asset Allocation for BlackRock’s Global Allocation team and is a regular contributor to The Blog.