Although I have lived just outside of Washington, DC for over twenty-five years now, I have never been a huge fan of politics (which is blasphemy around here). Politicians can have a positive impact on our lives, and even be transformational on occasion, but too often they are a bit manipulative, disingenuous, divisive, and hypocritical (I apologize for the early negative tone of this quarter’s musings, but I am writing this after just watching the latest presidential debate). As Groucho Marx once quipped, “Politics is the art of looking for trouble, finding it everywhere, diagnosing it incorrectly and applying the wrong remedies.”

Well, regardless of my feelings towards politics and politicians, as we quickly approach Election Day, I thought it relevant to review some of the tax proposals of the two major party candidates, Hillary Clinton and Donald Trump. As a quick aside, in speaking with a colleague the other day about this commentary, he reminded me that federal income tax is not a permanent fixture in the US. There was no income tax in the United States until 1861. Income taxes disappeared again from 1872-1894, and only came back for one year before being declared unconstitutional by the Supreme Court in Pollock v. Farmers’ Loan & Trust Co., 1895. This decision stood until the ratification of the 16th Amendment in 1913. Now I know why they called them “the good old days.”

As the current favorite to win the Oval Office, Hillary Clinton has proposed a number of law changes that would increase taxes on high-income taxpayers as well as increase estate and gift taxes. In summary (and it is not pretty for higher income taxpayers, so you better sit down):

- Impose a 30% minimum tax on taxpayers with an Adjusted Gross Income (“AGI”) above $1 million (the “Buffett Rule”)

- Enact a further 4% surcharge on taxpayers with an AGI over $5 million (so a Federal top tax rate of 43.6%)

- Limit the value of itemized deductions and exclusions to 28% (a further tax increase, really)

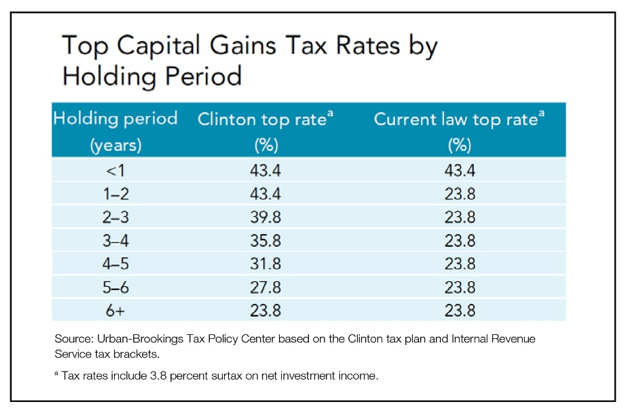

- Create a new (and rather complicated) tax schedule for capital gains, with rates declining over substantially longer periods of time than current law (in the chart below, the surtax mentioned is the 3.8% tax on investment income (for higher income taxpayers) passed as part of the Health Care and Education Reconciliation Act of 2010, also known as “Obamacare”):

- Tax carried interest as ordinary income

- Prevent taxpayers with high balances in tax-deferred accounts from making additional contributions

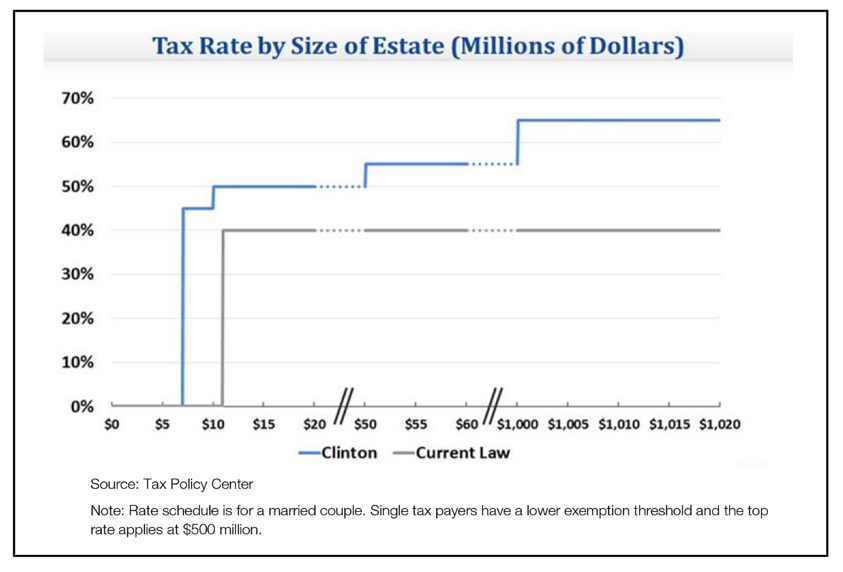

- Permanently reduce the tax threshold for estates from $5.45 million to $3.5 million ($7 million for married couples) with no adjustment for future inflation, increase the top rate to 65%, and set the lifetime gift exemption at $1 million

- Eliminate the “step-up” in basis at death

- Provide tax credits for caregiving expenses for elderly family members

In comparison, Donald Trump has proposed tax reforms that would significantly reduce Federal income tax rates for individuals, repeal the Alternative Minimum Tax (AMT), and repeal Federal estate and gift taxes. In summary:

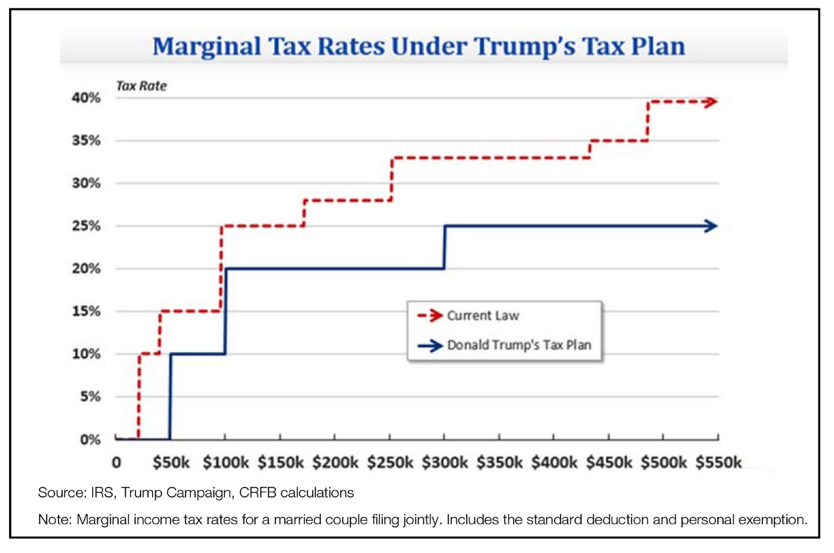

- Collapse the current seven tax brackets into three brackets of 10%, 20% and 25% (see graph below).

- Increase the standard deduction to $25,000 for single filers and $50,000 for joint filers, indexed for inflation thereafter

- Tax dividends and capital gains at a maximum 20% rate

- Repeal the 3.8% surtax on investment income of high-income taxpayers described above

- Limit the tax value of itemized deductions (other than charitable contributions and mortgage interest)

- Repeal the Alternative Minimum Tax (AMT)

- Tax carried interest as ordinary income Repeal Federal estate and gift taxes

So, not surprisingly, the two candidates disagree on tax policy, with progressives tending to argue that higher taxation and government spending will help the economy while conservatives maintaining that lower taxes are the key for future prosperity.

While we do not know which, if any, of these tax proposals will ultimately be enacted, at least from a capital gains perspective, investors (and advisors) will be well served to keep these points in mind:

- Active managers will potentially have even larger hurdles to overcome (as compared to passive strategies) when looking at after-tax returns

- Capital losses will become even more valuable as rates go up, so a consistent tax loss harvesting strategy is valuable

- Holding periods will have to be monitored even more closely when making sell decisions over time

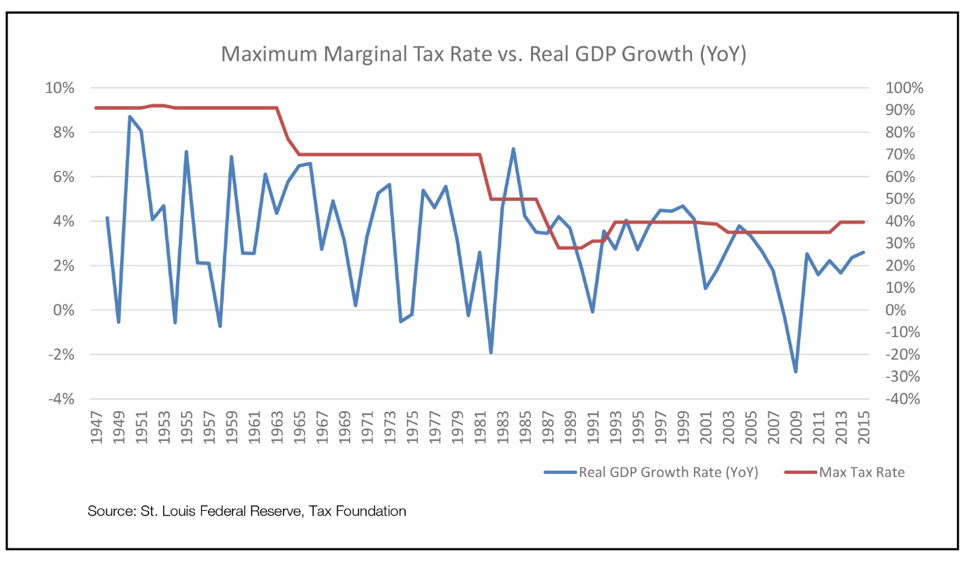

How either of these tax proposals will affect the overall economy is really anyone’s guess. Historically, there has been little correlation between tax rates and GDP growth:

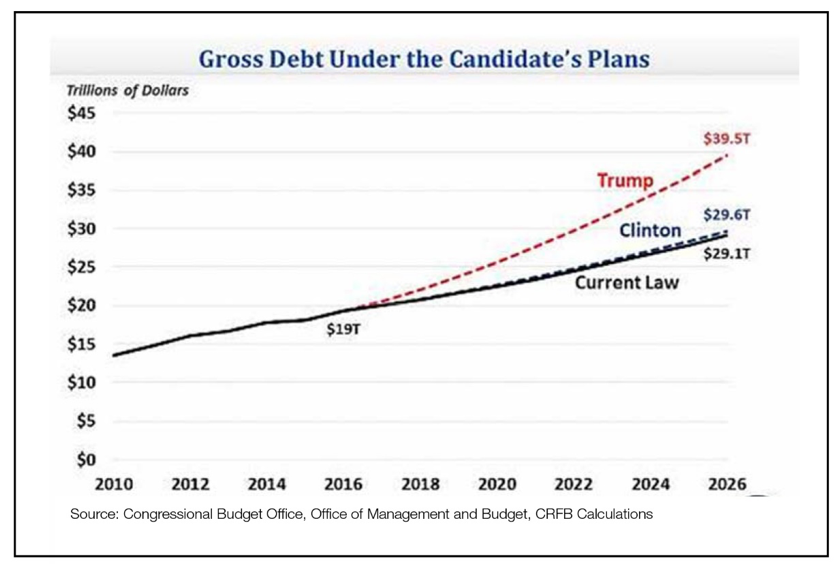

One (not very conservative) aspect of Donald Trump’s tax plan is its impact on our Federal deficits and debt. While it is believed that Hillary Clinton’s tax and spending proposals would cause a relatively modest increase of our national debt, Donald Trump’s proposals would sharply boost deficits and debt over the next decade - the yin and yang of taxes and debt.

As Richard Lamm (the former Governor of Colorado) once said, “Christmas is a time when kids tell Santa what they want, and adults pay for it. Deficits are when adults tell the government what they want, and their kids pay for it.”

The Markets

“One of the funny things about the stock market is that every time one person buys, another sells, and both think they are astute.” William Feather

Brexit concerns temporarily relegated to the fine print of “objects in mirror are closer than they appear”, the markets turned their attention back to Janet Yellen hoping to decipher treasury futures markets and Federal Reserve meeting minutes. The latest non-move by the Fed in September prompted markets to assign a high probability of a rate hike by year end. This subsequently had a negative impact on bonds and high dividend yielding equities.

US large company stocks (represented by the S&P 500 Index) rose 3.9% for the quarter while US small-mid company stocks (represented by the Russell 2500 Index) rose 6.6%. International stocks (represented by the MSCI ACWI ex US IMI Index) topped 7.1%, while emerging market stocks (represented by the MSCI EM IMI Index) rose 9.0%. The positive numbers hid a fair amount of volatility. Interest rate sensitive sectors like utilities and telecommunications sold down nearly 6% in Q3, while tech companies rallied in excess of 12%.

Part of the Fed concern came from the dissent of three Fed members (i.e. they wanted to raise rates in September and not wait). Abroad, central bank angst subsided. The ECB left rates unchanged, the UK cut rates by 0.25%, while Japan tweaked their QE policy to keep rates steady but began targeting higher inflation. As this transpired in August and September, the value of the US Dollar rose approximately 3% against other major currencies. More tangibly, the Barclays Capital US Aggregate Bond Index rose 0.5% for the quarter, most of that in post-Brexit July. Muni bonds (which are not in the aforementioned Aggregate index) and Treasuries (which are) did not fare as well, both falling 0.3% in Q3. Abroad, while UK Gilts fell 0.5% (primarily due to weakening currency), European Union Government Bonds continued to benefit from ECB buying, rising 1.4%. Lastly, high-yield bonds continued the rally that began in Q1, finishing up approximately 5.5% for the quarter.

Alternative investment performance varied across strategies in Q3. Multi-strategy funds (represented by the HFRI FoF Diversified Index) rose 2.1% for the quarter. Hedged equity managers (represented by the HFRX Equity Hedge Index) rose 3.4%, with growth biased strategies outperforming value (reversing course from earlier this year). REITs on the other hand had a mixed quarter with positives abroad (+4.9%) offset by weakness in the US (-0.8%). Global Infrastructure finished up 1.9% in Q3, despite a rough go for aforementioned US utilities. Commodities lagged (-3.9%) for the quarter, with natural gas down 7.9% and WTI oil down 4.9%. Grains also struggled, with bumper crops in corn and wheat pushing both more than 10% lower. Positives in industrial metals (e.g. Nickel +11.6%) and softs (e.g. sugar +9.9% and cotton +6.2%) were not strong enough to overcome their smaller weight in the global commodities trade.

Some Thoughts

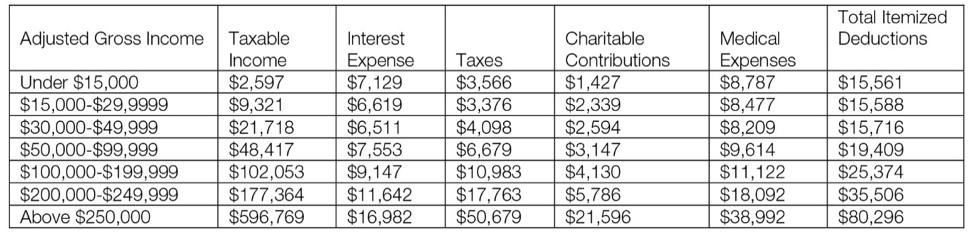

With all of this talk about taxes, every year the government releases data on the “average” deductions taken on individual returns filed in previous years. We think the below numbers for 2014 are interesting.

Source: Kiplinger

Some of my favorite political quotes (some more cynical than others):

- “In politics, stupidity is not a handicap.” Napoleon Bonaparte

- “It has been said that politics is the second oldest profession. I have learned that it bears a striking resemblance to the first.” – Ronald Reagan

- “Since a politician never believes what he says, he is quite surprised to be taken at his word.” – Charles de Gaulle

- “When I was a boy I was told that anybody could become President; I'm beginning to believe it.” – Clarence Darrow

- “Politicians and diapers must be changed often, and for the same reason.” – Mark Twain

- “No man's life, liberty, or property are safe while the legislature is in session.” – Mark Twain

- “When they call the roll in the Senate, the Senators do not know whether to answer 'Present' or 'Not Guilty'.” – Theodore Roosevelt

- “In my many years I have come to a conclusion that one useless man is a shame, two is a law firm, and three or more is Congress.” – Peter Stone

- “We hang the petty thieves and appoint the great ones to public office.” – Aesop

- “Politics is the art of choosing between the disastrous and the unpalatable.” – John Kenneth Galbraith

- “The Constitution is not an instrument for the government to restrain the people, it is an instrument for the people to restrain the government - lest it come to dominate our lives and interests.” – Patrick Henry

- “I predict future happiness for Americans, if they can prevent the government from wasting the labors of the people under the pretense of taking care of them.” – Thomas Jefferson

- “Let us not seek the Republican answer or the Democratic answer, but the right answer. Let us not seek to fix the blame for the past. Let us accept our own responsibility for the future.” – John F. Kennedy

Bill Schwartz is Managing Director, Principal & Co-Chief Investment Officer of Bronfman E.L. Rothschild

Bruce R. Laning, CFA, Managing Director and Principal, and Dmitriy Katsnelson, Director, Investment Research contributed to this report

http://www.belr.com/

Certified Financial Planner Board of Standards, Inc. owns the certification marks CFP®, Certified Financial Planner™ and federally registered CFP (with flame design) in the U.S., which it awards to individuals who successfully complete CFP Board’s initial and ongoing certification requirements.

Bronfman E.L. Rothschild is a registered investment advisor. Securities, when offered, are offered through an affiliate, Bronfman E.L. Rothschild Capital, LLC (dba BELR Capital, LLC), member FINRA/SIPC.

This publication should not be viewed as a recommendation, an offer to sell, or a solicitation of an offer to buy a particular security or service. The commentary provided is for informational purposes only and should not be relied on for accounting, legal, tax, or investment advice. Financial information is from third-party sources. While such information is believed to be reliable, it is not verified or guaranteed. Performance of any indexes is provided for reference and competitive purposes only without factoring any fees, commissions, and other charges. Individual results achieved by investors will be different from those of the indexes. Indexes are unmanaged; one cannot invest directly into an index. The views and opinions expressed are those of Bronfman E.L. Rothschild, LP, and they are subject to change at any time. Past performance does not imply or guarantee future results. Investing in securities involves risks, including possible loss of principal. Diversification cannot assure a profit or guarantee against a loss. Investing involves other forms of risk that are not described here. For that reason, you should contact an investment professional before acting on any information in this publication.

© 2016 Bronfman E.L. Rothschild, LP

Read more commentaries by Bronfman E.L. Rothschild