Election years are always fun. Complex, emotional, exhausting — but fun. The news cycle can cause a certain myopia, however, and investors with longer-term goals would do well to consider the U.S. elections in a broader context. The BMO Multi-Asset Solutions Team’s disciplined process is to develop views through a framework of valuation, the economy and policy (both monetary and fiscal) around the world. We are positioned with a slight overweight to equities versus fixed income, and within equities an overweight to U.S. equities versus international developed markets. Within fixed income, we prefer high-yield bonds to core bonds, though we are reassessing this preference daily. Here is a look at what is driving these views looking into the fourth quarter of 2016.

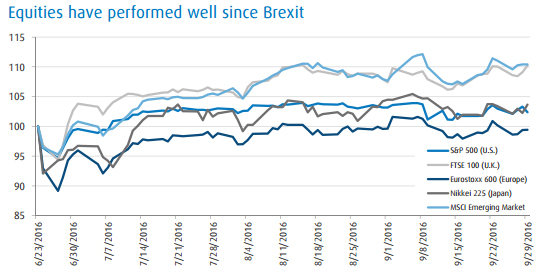

Post-Brexit rally may signal complacency

In the uncertainty surrounding the future of the European Union, which may weigh down business confidence and investment, we see risks that have not been fully priced in by the markets and maintain a slight underweight to European equities.

After an initial shock following June’s Brexit vote, markets recovered and performed well over the third quarter. Equities on the whole have done well, and some may be surprised to see the U.K. leading the pack. There may be some complacency behind this, particularly in the U.K. and Europe, where substantial policy risk remains. For one, the U.K.’s exit from the European Union has barely begun. Theresa May, the newly elected British prime minister, has been quiet on the details beyond plans to open talks in April 2017, so British voters know little about the negotiations. From what they do know, only 16% think May is doing well, according to a recent YouGov poll.

Sources: Bloomberg, BMO Asset Management. Returns are based on total return and include dividends.

A number of populist parties also continue to gain traction across Europe, adding to policy uncertainty. Austria’s Freedom Party leads in the second round of presidential elections in December, and with the growth of France’s National Front and Germany’s Alternative for Germany parties, populist sentiments are shaping more of the national discussions on open borders, immigration and, ultimately, membership in the European Union. Spain, meanwhile, has not had an elected government all year.

Italy will hold a referendum on constitutional reform in December; a vote for constitutional reform would redesign some government responsibilities and perhaps lend some stability to the Italian government, which has seen frequent turnover since the Republic began in 1946. But it risks giving the prime minister too much power, and some who will use the referendum to protest the status quo, which in Italy is sluggish growth with little wiggle room for fiscal stimulus amid EU austerity. A vote against the reform could mean the resignation of Matteo Renzi, the Italian prime minister, and potential for disarray in Italy, with ripple effects across Europe.

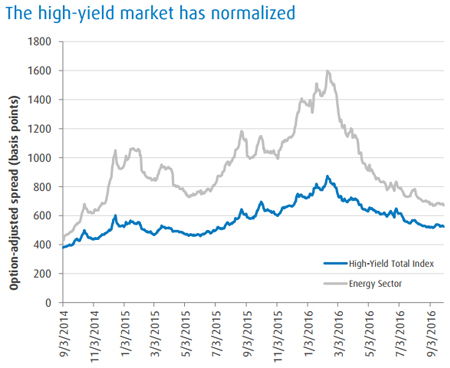

High-yield run nearing a conclusion?

Sources: Bloomberg L.P., Eurostat

Early in 2016 we made the decision to increase our overweight position in high-yield bonds. We traded on a risk-neutral basis, and so far the trade has been successful. Supporting our decision at the time was a market in disarray, with relatively low liquidity, and with energy and materials concerns having an outsized effect on high-yield index returns. High-yield spreads reached a high of 900 basis points early in the year, which we found relatively attractive from a valuation perspective. Finding such a spread was not supported by fundamentals (ex-energy spreads rose along with energy spreads, and overall default rates remained low), we deemed it an exceptional opportunity.

Looking to the fourth quarter, we find our thesis getting closer to its conclusion: the dislocation between energy and the rest of high yield has narrowed, and the high-yield market is largely back to normal. As trading on the sector becomes more orderly, we will consider reducing our exposure in this area.

U.S. solid despite drama

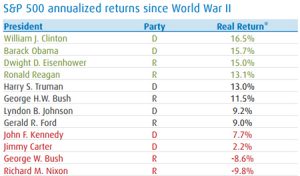

Policy risk in the U.S. poses less of a threat than in Europe, which leaves the U.S. slightly more supportive of risk assets. As we noted in a third-quarter MAST Strategy Spotlight, although the presidential election is certainly dramatic, there are reasons to think the effect of its outcome on markets may be muted, notwithstanding some short-term volatility. From the perspectives of the markets, the president’s political affiliation tends to have little effect on them over the long term. Since World War II, the four best and four worst presidents for stock market returns have both included two Democrats and two Republicans.

*Return above the rate of inflation. Source: Bloomberg, BMO Global Asset Management

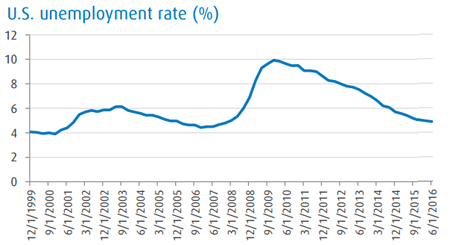

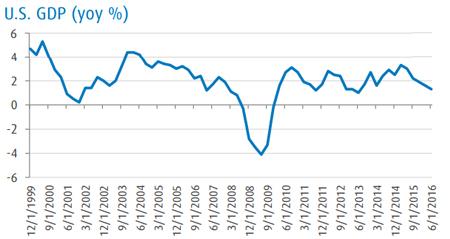

As of early October, the markets are predicting a Clinton victory and a divided government. A divided government could also greet a Trump victory, however; so no matter who wins, there should be a victory for gridlock. While we expect some volatility surrounding the election, over the medium term we don’t expect it to have a major impact on broad asset classes. With modest positive signs — GDP growing at an average of 2% over the last five years and low unemployment — the U.S. should continue its slow but steady growth.

Source: Bloomberg L.P., BMO Global Asset ManagementSource: Bloomberg L.P., BMO Global Asset Management

Highlights from Global Investment Forum

In September BMO Global Asset Management held its Global Investment Forum in London. The event is a gathering of senior BMO investors from around the world to discuss topics that will affect portfolios over the next three to five years. On the whole, we found that while policy risks remain elevated and there are few undervalued asset classes, global growth remains just strong enough to support risk assets. Below are a few highlights of our discussion, which will be presented in more detail in BMO’s Secular Forum later in the year.

Old populism in new suits

In our last quarterly review and outlook, we discussed growing populism in terms of the gains a number of fringe political parties have made in the polls in Europe and in terms of new strains in both Republican and Democratic parties in the U.S. Today some of this populist sentiment is also playing out in concrete policy decisions.

In September Congress voted to override a veto by President Obama on a bill that would allow families of victims of the 9/11 terrorist attacks to sue Saudi Arabia for any role it had in the attacks. The law will allow U.S. courts to seize Saudi assets to pay for any judgments against Saudi Arabia if necessary. Some worry the U.S. could face similar suits for past activities abroad.

The U.S. is also seeking punitive damages from Deutsche Bank over its selling of mortgage-backed securities prior to the financial crisis of 2008; at the same time, the European Commission ordered Ireland to collect roughly $14 billion in back taxes from Apple, after Ireland allegedly gave Apple undue tax benefits. Both moves seem calculated for public impact, and neither is isolated: the U.S. is also looking at Barclays and Credit Suisse alongside Deutsche Bank, while the EU also has ongoing tax investigations into Amazon and McDonald’s that could make headlines similar to Apple’s.

These events raise the possibility of a more litigious international business environment, which could discourage foreign investment and slow growth.

Energy demand should steady

A year ago, most predictions about where the market would be in the next six to 12 months began with the caveat: depending on the price of oil. Today these words are heard a little less. In late September, OPEC announced a decision to cut production; the move surprised markets momentarily, first to the upside, then downward. But we are skeptical about OPEC’s follow-through and its ability to control the market as it has before. It remains unclear which members would cut production and by how much. On top of that, member countries have not done a great job sticking to promises in the past.

As consumers walking into auto dealerships today may be looking at the last new gas-powered car they will ever buy — at the Paris Motor Show in September auto makers debuted roughly two dozen new electric vehicles — it’s reasonable to think oil’s ability to drive the markets will wane somewhat. With a slow structural shift in demand underway, a reasonable base case would be that oil remains in the $40–$60 per barrel range, with Asia remaining the key contributor to energy demand growth.

Technology and productivity changes increasing

The changes in technology behind the slow shift in auto demand is also playing out in the job market, as automation continues to grow: it is estimated that 47% of jobs in the U.S. are susceptible to automation. Automation has had a significant impact on manufacturing — more so than trade has, according to a study by the Center for Business and Economic Research at Ball State University in Indiana. “Almost 88% of job losses in manufacturing in recent years can be attributable to productivity growth, and the long-term changes to manufacturing employment are mostly linked to the productivity of American factories,” the study says. If technological advancement is left unmanaged — or poorly managed — these changes could be disruptive in the future.

Source: “The Myth and the Reality of Manufacturing in America,” 2015

Conclusion: Risk assets still strong

As we look to the fourth quarter of 2016, we believe broader growth trends should be able to withstand the risks outlined here. While growth is slow, context is important. Amid worsening demographic trends and weak global productivity, it may be unrealistic to expect historical trend growth to continue. With an expected lower trend growth rate, however, the scale may need to be relabeled somewhat: there will be more “recessionary” periods in which GDP growth momentarily dips below zero. When two consecutive quarters of negative GDP growth — the textbook definition of a recession — does not seem so far-fetched, and yet growth is on the whole slow and steady, perhaps we should rethink our definition of recession.

In a longer-than-textbook business cycle, under monetary policy that remains accommodative (even with the possibility of a December hike in the U.S.) and with some slack still in the labor market, we see just enough more positives than negatives in the numbers. An environment of lower interest rates for longer and slower but still persistent growth is positive for an overweight to equities, and for a risk friendly position in fixed income.

Definitions and disclosure

This is not intended to serve as a complete analysis of every material fact regarding any company, industry or security. The opinions expressed here reflect our judgment at this date and are subject to change. Information has been obtained from sources we consider to be reliable, but we cannot guarantee the accuracy. This publication is prepared for general information only. This material does not constitute investment advice and is not intended as an endorsement of any specific investment. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. Investors should seek advice regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Investment involves risk. Market conditions and trends will fluctuate. The value of an investment as well as income associated with investments may rise or fall. Accordingly, investors may receive back less than originally invested.

Past performance is not necessarily a guide to future performance.

BMO Global Asset Management is the brand name for various affiliated entities of BMO Financial Group that provide investment management and trust and custody services. Certain of the products and services offered under the brand name BMO Global Asset Management are designed specifically for various categories of investors in a number of different countries and regions and may not be available to all investors. Products and services are only offered to such investors in those countries and regions in accordance with applicable laws and regulations. BMO Financial Group is a service mark of Bank of Montreal (BMO).

Investment products are: NOT FDIC INSURED — NO BANK GUARANTEE — MAY LOSE VALUE.