We’ve annoyed a few media outlets by admitting to having no clue as to which of the presidential candidates would be “better” for the stock market. There are just too many variables at work, not the least of which relates to initial conditions. Those conditions, for example, were ideal for Barack Obama— who entered his first term with the S&P 500 trading at just 12x 5-Year Normalized EPS. That’s more than 60% below the level prevailing at the 2001 inauguration of George W. Bush (31x). The excellent returns achieved over Obama’s reign were therefore practically baked in the cake (...Mr. Obama himself might say “he didn’t build that”).

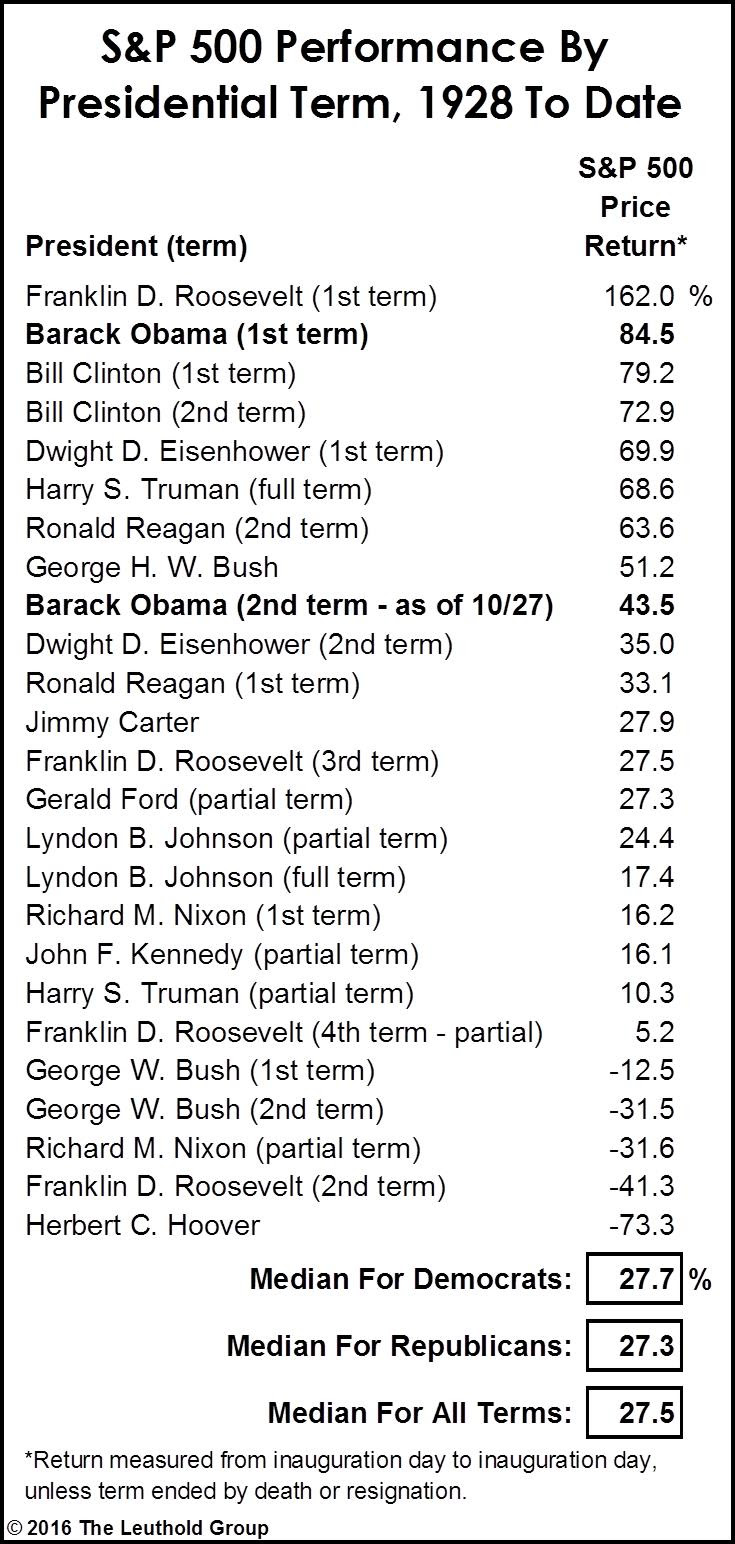

The S&P 500 gain of +44.0% during Obama’s second term ranks well ahead of the median of +27.5% gain for all presidential terms (included truncated ones) since 1928. The market’s first-term gain of +84.5% is the second-best on record, joining three other Democratic administrations among the top four spots. Meanwhile, four of the five presidential terms associated with a cumulative loss in the S&P 500 occurred with Republicans at the helm—with “W” making the list two times.

A tally of all terms since 1928 provides no basis for partisanship, however. The median S&P 500 gain under Democratic presidential terms has been +27.7%, practically identical to the +27.5% earned during Republication terms. The results suggest that policy differences between the parties are either (1) fully reflected in stock prices by the time a candidate officially takes office; (2) overwhelmed by larger cyclical forces; or (3) fundamentally indistinguishable from one another. In practice, all three factors are likely at work.