3rd Quarter Commentary

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits"I am wiser than this man, for neither of us appears to know anything great and good; but he fancies he knows something, although he knows nothing; whereas I, as I do not know anything, so I do not fancy I do. In this trifling particular, then, I appear to be wiser than he, because I do not fancy I know what I do not know."

Socrates, 5th Century BCPhilosopher

This quarter we’re going to take a break from our usual practice of surveying the investment landscape and instead focus on a single topic which begins on the next page.

We have attempted to write in a manner interesting to students of the markets but still understandable by the layman. Most of the technical details behind our exercise will appear in footnotes at the end of this letter... we suggest casual readers skip these.

“How much should stocks go up when rates go down?”

or

“How I learned to stop worrying about valuation and love stocks.”

It is relatively common knowledge that when interest rates decline stocks ought to rise, and they typically do. We are far from the first investors to ponder the effect of interest rates on valuation, but the majority of the analyses we have seen have been empirical, i.e. more about what happened in the past. A good example is the following graph which compares 10-year treasury rates (bottom axis) with the earnings yield of the S&P 500 (inverse of the P/E) on the side axis. The image contains a linear “best fit” line, but it would be quite a jump to say that the market “ought” to price itself to be on the line.

Given that the market rise of the past few years was probably somewhat justified by the decline in interest rates, we set out to try and demonstrate to ourselves just how much stocks should move when interest rates fall. The analysis is simple enough, but we hadn’t seen anyone else do it and wanted to see for ourselves. From here it is an irresistible step to ask “is the stock market expensive?” In preview, we answer with a rather qualified “no”.

Before we get started we must confess to a number of caveats.1 First off, we are not forecasting future interest rates! We are agnostic, though we have been and continue to be very skeptical of the idea that “rates will rise because they have been lower than they were in the past”, as we have discussed in previous quarterly letters. Rates will definitely change in the future, one way or the other. (Those who believe rates can surely go no lower may wish to examine their rate forecasting track record.)

Secondly, in order to undertake this demonstration we had to make lots of assumptions. We didn’t try to necessarily make the “right” assumptions; we simply attempted to make reasonable and defensible ones. As reasonable minds can and will differ on these assumptions, we have published our data2 and underlying calculations on our website (www.knightsb.com/CRAPE_Data_&_Analysis.xlsx).3

Finally, the biggest caveat is that we are about to demonstrate how value changes when you change one variable (interest rates) and leave all else equal. In the real world, when you change one thing, all else is never equal, and economic variables have a sneaky way of interacting in offsetting ways. Lower interest rates often come with lower accompanying earnings growth, which would have a large effect on stock market value if appropriately predicted. Earnings growth has and will change over time; we have not varied it in our exercise.3

A stock receives its value from the future cash flows it will deliver to the company’s owners. The stock market is just a grouping of individual stocks, and in aggregate receives its value from all the future cash flows of all the underlying companies in the market. Without going through all the basics of the time value of money, one dollar of cash flow ten years from now is worth less than one dollar of cash flow next year. Just how much less is determined by interest rates, or discount rates as they are sometimes called. Thus, the same exact set of future cash flows has a very different present-day-value under a different set of interest rates.

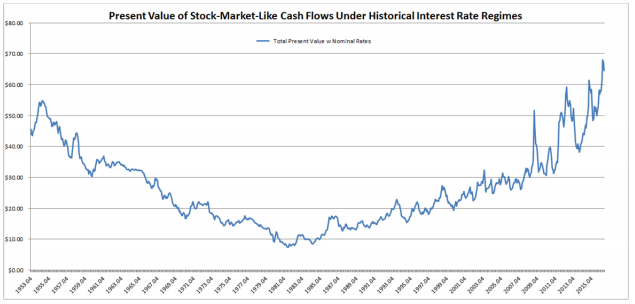

To demonstrate the effect of interest rates on valuation, we constructed a “stock-market-like” set of cash flows growing at the average historical rate of real earnings growth4... and only changed the interest rates we used to value those cash flows.5 We dug up the real world U.S. interest rates that were recorded for every maturity in every month since 1953. We then used each set of different interest rates to value the same set of cash flows to come up with different present values for each historical month (i.e. discounting future period cash flows by the actual interest rates on the yield curve at that time during the 1953 to today period).6 Below we present the value of the “stock-market-like” stream of cash flows under the interest rate regimes which prevailed since 1953.

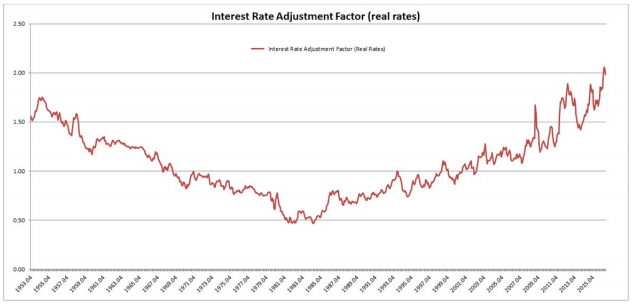

As you can see, changes in the interest rate environment alone have an enormous effect on value, all else equal. Indeed, today’s near-all-time-low rate environment would imply historically lofty valuations. Looking at the above chart, in today’s low discount rate environment a stock-market-like stream of cash flows is worth more than in any period since at least the 1950s. We went on to make a couple adjustments (that require a lot of assumptions) to instead use estimated real (after inflation) interest rates7 and include an equity risk premium.8 This produced the more realistic absolute numbers which appear below… which send the same basic message.

Another way to present these results is to pick a base year and put the valuation implications of interest rates on a relative basis- how much more or less the same set of cash flows is worth under different interest rate environments. We chose March 1971 as our base period because its interest rate environment produced the median present value of cash flows in our above analysis, but choosing March 2000 or September 1993 would have yielded nearly identical results.9 Below is the effect of the interest rate environment on valuation relative to March 1971.

This measure shows the same exact asset would be worth double today what it would have been worth in 1971, 1993, or 2000! In other words it shows the change in interest rates implies a justified doubling of investment multiples such as price to earnings or price to sales. (That being said we’re not suggesting stocks will actually trade to those levels, not least of which because stocks were not necessarily at justified levels previously. Even we admit in the current environment there is more scope for rates to rise which is an increased risk). This magnitude of valuation increase stands in stark contrast to some off-the-cuff estimates we sometime run across which posit that the market should trade 10-15% higher than “normal” due to the current rate environment. Interest rates make a bigger difference than that.

Let’s turn our attention to today’s U.S. stock market... is it expensive or not? First, a short disclaimer on what “expensive” means for the market. Market valuation should not be used as a timing tool! “Expensive” does not mean “will go down in the future”, not least of which because overpriced assets can and do become more overpriced for very long periods of time. Furthermore, the market would be expected to have a general rate of advance over time as the economy grows, and so even a pricey market might still be expected to appreciate, just perhaps not as fast as it would under a less exuberant valuation.

In any case, in our opinion the best measure of whether the stock market is cheap or expensive is Professor Robert Shiller’s “Cyclically Adjusted Price to Earnings Ratio”, or CAPE, which we have mentioned a few times in previous quarterly letters. This measure takes the price of the market and adjusts it for the average earnings of the market for the last ten years (adjusted for inflation), based on the idea that earnings can swing so much from year to year that a longer term average is a better measure of true earnings power going forward. An updated graph appears below.

While not at all-time highs, by this measure the market appears to be in expensive territory.10

However, the CAPE doesn’t take into account the interest rate environment. Isn’t it therefore likely that some of the market’s expensiveness is “justified” by the rate environment? How much? To answer this question we can again choose a base year and then adjust the regular CAPE values up and down according to our earlier exercise demonstrating the effect of interest rates on value.11 This modifies the original CAPE to come up with a “Cyclically Rate Adjusted PE”, or CRAPE. We present the results atop the next page.

In this updated measure, when the interest rate environment is taken into account, today’s market doesn’t look so expensive... in fact the current CRAPE value of 13.51 is below 77% of all the observations since 1953. Despite being near all-time absolute highs, the stock market no longer appears “frothy” or wildly overvalued.

So are stocks expensive? It depends on what you adjust for. If you only adjust for earnings, then yes, stocks do appear expensive. But, if you adjust for earnings as well as interest rates, then stocks do not appear expensive.12

What does this mean? It means that if you believe either 1) rates are staying where they are or 2) rates are equally likely to go down as opposed to up or 3) you have no wish to place a bet on rates because you have no insight better than the bond market’s, then... stocks are reasonably valued and perhaps on the cheap side, when compared to your other main alternative, the bond market.13 There are other conclusions as well. For those who say, “I don’t want to adjust for interest rates”, then yes, stocks are expensive... but bonds are REALLY expensive. If you are worried about stocks because you think rates will rise, then you ought to be even more worried about bonds. Another conclusion is that because our CRAPE measure ends somewhat below the median range, rates could indeed rise to some degree and stocks would still be cheap (our ballpark estimate is that even if rates rose around 1% across all maturities, stocks would still be reasonably valued).14 Alternatively stated: stocks perhaps didn’t rise enough when rates fell so they wouldn’t fall if rates rise (or at least not nearly as much as bonds).

We have heard many complaints in recent years that “stocks are expensive, bonds are expensive, real estate is expensive... everything is expensive.” And...? This is the same thing as saying worldwide interest rates in general are “too low”… and carries few practical implications unless you also believe “this will change”. If assets are too expensive, then must one hold cash or nothing in order to “buy” what’s cheap? Holding cash is only beneficial if asset prices fall... which is possible, but over time that is a losing proposition, and is tantamount to timing the market. (We continue to hold some cash because it allows us to be opportunistic and for risk management purposes).

Finally, we must address those who would protest “but rates ARE going up.” They very well might be… or they might not… or at least even if they do, the pace and magnitude are unknown. Much like Socrates, we do not know, and we are aware that we do not know. Those who think they do know when and how rates will return to “normal” would do well to look at 1) Japan’s ultra-low rates of the past 20 years 2) the even-lower negative rates in Europe and 3) the history of interest rates in the U.S. in the decades around the turn of the 19th century (hint: low for a very long time).

In any case, the real question for equity holders isn’t “are rates going to rise”, it is rather, “are rates going to rise with enough magnitude to send the stock market lower, and in a short enough timeframe such that it will be worth sitting in cash during the wait.” We definitely do not know the answer to this. We do admit that the forward return profile for stocks at present does not match the average of the last 10, 20, or 50 years. Still, when viewed against bonds or cash, we believe stocks are the best game in town.

We thank our clients for the continuing trust you place in us.

Sincerely,

John G. Prichard

Miles E. Yourman

P.S. Special thanks are due to our summer intern, Alex Pearce, who helped extensively with the arranging of the data and the construction of the spreadsheet behind this exercise. Good luck in your senior year!

Past performance is not indicative of future results. The above information is based on internal research derived from various sources and does not purport to be a statement of all material facts relating to the information and markets mentioned. It should not be construed that the information in this commentary is a recommendation to purchase or sell any securities. Opinions expressed herein are subject to change without notice.

1 A couple caveats did not make the cut for inclusion in the body:

We are not academic professionals, or even fixed income specialists! We apologize for shortcomings in data, methods, underlying theory and interpretation.

We assume someone has already done this work elsewhere, so we apologize for not citing it but we couldn’t find it.

2 We are greatly indebted to Professor Robert Shiller for providing most of the data we used in this analysis for free on his website. Data for the S&P pricing, earnings, and inflation come from Professor Shiller’s website. We are also indebted to Professor Aswath Damodaran for providing his estimates of the Equity Risk Premium used in this analysis for free on his website as well.

3 This particular assumption Professor Damodaran would likely find especially egregious, as indicated in an excellent blog post which is available here: http://aswathdamodaran.blogspot.com/2015/04/dealing-with-low-interest-rates.html . We admit some of our main reasons were simplicity and laziness. Adding in varying growth rate assumptions would have entailed a lot of justifications and would have complicated the message we are trying to convey.

4 This stream of cash flows takes the form of $1 next year, which then grows by constant “Long Term Real Earnings Growth Rate Assumption”. The default assumption for this value is the long term 1871-2015 average rate of real earnings growth, 1.70%.

5 An alternate, and perhaps more rigorous approach, would be to have a separate set of underlying cash flows for each year, growing cash flows by historical earnings growth rates in the near terms, while having growth mean revert to some average assumption over the longer term.

6 We had to make a few assumptions to get all the historical interest rates necessary as the data set we downloaded from the Federal Reserve website (thanks to them too for making the data freely available) didn’t contain all maturities.

We used a straight line average to estimate the yield on maturities between two known observations. For example the 4 year rate was calculated as the average between the 3 and 5 year rate. We realize that the yield curve is not typically a straight line but believe this simplifying assumption will only result in the smallest of distortions.

The U.S. government does not issue bonds in maturities longer than 30 years, and didn’t always issue 30 year bonds for that matter. We decided to generate discount rates for periods beyond the last observed maturity (usually 30 years) by adding a constant for each additional year. This seemed to us a reasonable assumption given the general upward sloping nature of yield curves and that at longer and longer durations it is hard to consider anything risk free (you might consider this increase in discount rate with maturity as instead part of an increase in the equity risk premium as opposed to the risk free rate). The default constant used is 0.0166% which is the annual steepness of the yield curve from 10 to 30 years in our dataset for which rates of both maturities were both available. This is one of the metrics you can change in the “Control Panel Inputs” tab. In order to test the effect of our long term interest rate assumptions we did a parallel analysis looking at only the first 20 years of cash flows. The results, which we did not find to 10 be materially different, are available on the spreadsheet posted to our website.

We used the interest rate quoted on the bonds of different maturities instead of the more technically correct rate on “zeros” as a simplifying assumption.

7 Because we are using a full term structure of rates to discount our cash flows, we needed to come up with expected inflation rates over the full range of different time frames. Using the observed inflation rate from the previous year seemed appropriate for short terms but less so for longer terms. We ultimately decided to assume that people would expect inflation to eventually return to a Long Term Inflation Rate Assumption over 15 years. This variable can be altered in the “Control Panel Input” tab.

8 We add a constant equity risk premium across the years and across the maturity spectrum to the discount rates used. The default value is Damodaran’s average estimate of the ERP from 1961-2015 (the time frame available in his dataset).

9 March 1971 was chosen as a base year because under the default assumptions the interest rate regime in force at the time yielded a present value in the median of our sample.

10 It is worth noting that Professor Jeremy Siegel has proposed a tweak to the CAPE to make it based off of allegedly more reliable earnings data from the commerce department along with some other small adjustments. We think both are reasonable and would note that this measure of the modified CAPE has a lower current reading. We used the original because of our familiarity with and availability of Shiller’s data.

11 We take the original CRAPE and divide it by the Interest Rate Adjustment Factor (which is the ratio of present value of the measured period to the base period). We are happy to entertain any suggestions to this method.

12 Note that had we gone the route of adjusting our set of cash flows for different growth rate estimates, these growth estimates would likely be lower today than in the rest of the sample and this method would result in a market that looks less cheap. We held off on this measure of adjustment because, among other reasons noted in the footnotes above, it would have introduced additional subjectivity into the analysis. All other inputs into the process (other than the expected inflation rates used to obtain real rates) or directly observable. Though there clearly is a relationship, we also remain skeptical that there is an ironclad relationship between risk free rates and the future growth in corporate profits, especially in the longer term.

13 We would add that real estate in general looks like an expensive alternative as well.

14 There is a tool on the CRAPE spreadsheet posted on our website where you can evaluate the effects of a change in interest rates in “Future Period” would have on our hypothetical present value calculations and on the CRAPE.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All