In our alternative portfolios, we have the flexibility to use a range of sophisticated strategies—bullish, neutral and bearish hedges, convertible arbitrage and covered call writing, etc. While the tools we use can seem complex at times, our guiding principles are straightforward:

- Take advantage of opportunities the market presents. This includes changing our overall hedge stance (bearish, neutral or bullish), and adjusting our convertible arbitrage positioning, among other strategies.

- Focus on being as advantageously positioned for as many outcomes as possible.

Our investment philosophy can help us capitalize on market volatility, and we are positioned to apply the same approach in the post-U.S. presidential election market.

For a real-life example of how we pursue opportunities, here’s a review of the weeks before and after Brexit.

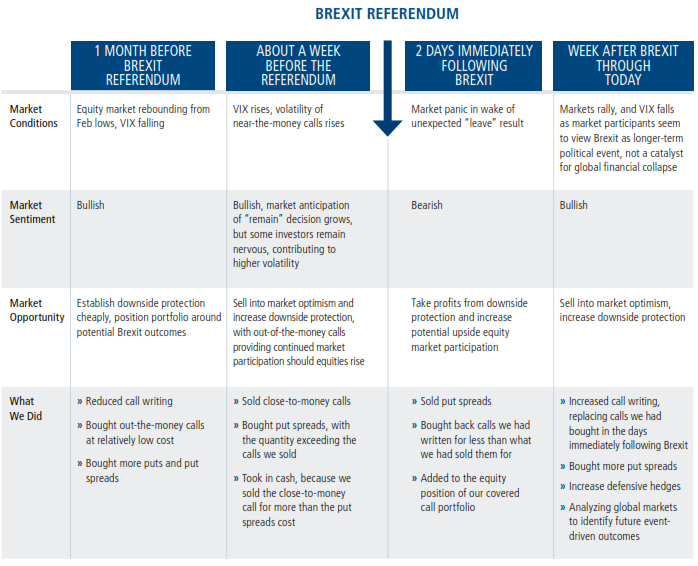

The Pre-Brexit Environment

About a month or so before Brexit, the U.S. equity market had rebounded from its February lows and was back near recent highs and the VIX had fallen from its February spike. While we typically have a hedge profile and structure we may prefer for our funds, it is important to focus on whether that is ideal in the current market environment. We continually search for a hedge that gives us as much downside protection as possible, while giving up as little participation as possible in a market rally. Depending on the market environment, this could mean using shorter-dated or longer-dated options, as well as increasing or decreasing our use of spreads, puts, or calls. These moves are incremental to our core hedge, which we use to maintain a base of downside protection at all times.

In the month before Brexit, the compensation for writing calls had dropped to a level that compelled us to explore different strategies. More specifically:

- We reduced our call writing activity and chose to increase our hedge through put spreads and buying outright puts.

- We bought out-of-the-money calls at a relatively low cost. Our rational was that if the market moved higher or call volatility rose back to attractive levels, these upside tail calls would allow us to sell more aggressively into the move.

A little over a week ahead of the vote, the VIX rose. Also, perhaps due to rising market expectations for a remain vote and a relief rally, volatility for near-the-money calls increased as well. As a result of having purchased out-of-the-money calls and having a slight underweight to calls, we were positioned to sell into this call rally. More specifically, we sold some close-to-the-money calls and used the proceeds to purchase put spreads, thereby enhancing our downside protection at a low cost. We were able to purchase 1.5 puts spreads for every call we sold, and still take in cash.

Market Dislocation

As a result of our positioning, we headed into a major event with more downside protection than normal and an asymmetric profile that we believed provided us with a better probability-weighted return profile independent of the referendum’s outcome. If the market rallied, we could lean on our long calls and if the vote came back in favor of exit and the markets sold off subsequently, the hedge we added would also allow us greater flexibility trading our convertible arbitrage portfolio. (For more on convertible arbitrage, see our recent blog on gamma trading.)

As the market sold off following the vote, we were able to do just that. We covered shares related to our convertible arbitrage strategy and sold put spreads, and also bought back the calls we had written for a fraction of what we had sold them for. We still felt comfortable with our downside hedge given the higher put protection we had established heading into the vote and now covering these calls gave us clearer runway to the upside in the event the market rallied back. Additionally, because we believed we had sufficient downside protection, we added to the equity portion of our covered call book as equities fell.

And the market did rally back. As this rally occurred, we realized profits by selling stock we had purchased in our convertible arbitrage and covered call portfolios the prior week. We also sold calls to replace the ones we had purchased when the market was lower.

As investment managers, we prefer to have certainty in our convictions, whether those views are about specific stock or bond values or about the outcome of specific events. While we didn’t purport to know what the outcome of the referendum would be, we knew there was an event and there could be a market dislocation, depending on the result. When we manage market neutral and covered call portfolios, we use a variety of strategies to achieve the risk/reward profile we seek. In the weeks before and after Brexit, we sought to capitalize on the opportunities that the markets gave us and to position our portfolios for as many outcomes as possible. As a result, we were able to effectively navigate the market environment as sentiment shifted in response to uncertainties.

Summary: How We Traded Around Brexit

As always, our approach in our market neutral income and covered call strategies includes maintaining a core hedge that provides a base of downside protection. With that base in place, we employ a variety of strategies to capitalize on market opportunities. Below, we outline how we traded around Brexit.

Before investing carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information or call 1-800- 582-6959. Read it carefully before investing.

Disclosure

Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation.

The VIX (CBOE volatility index) is the ticker symbol for the Chicago Board Options Exchange (CBOE) Volatility Index, which shows the market’s expectation of 30-day volatility. It is constructed using the implied volatilities of a wide range of S&P 500 index options.

Important Risk Information. An investment in the Fund(s) is subject to risks, and you could lose money on your investment in the Fund(s). There can be no assurance that the Fund(s) will achieve its investment objective

Investment in the Fund(s) is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. The risks associated with an investment in the Fund(s) can increase during times of significant market volatility. More detailed information regarding these risks can be found in the Fund’s prospectus.

Some of the risks associated with investing in alternatives may include hedging risk, derivative risk, short sale risk, interest rate risk, credit risk, liquidity risk, non-U.S. government obligation risk and portfolio selection risk. Alternative investments may not be suitable for all investors.

Past performance is no guarantee of future results.

The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Information contained herein is for informational purposes only and should not be considered investment advice.

This material is distributed for informational purposes only. The information contained herein is based on internal research derived from various sources and does not purport to be statements of all material facts relating to the information mentioned, and while not guaranteed as to the accuracy or completeness, has been obtained from sources we believe to be reliable.

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE

© Calamos Investments

© Calamos Investments

Read more commentaries by Calamos Investments