As 2016 draws to a close and a Fed hike looms, where should investors hunt for yield now? Terry highlights the case for three income-yielding asset classes.

Today’s low-to-negative interest rate world has sent investors searching far flung corners of the market for yield, driving flows into a range of once obscure, high-yielding asset classes. Attractive income does exist in a host of areas, but not all income-producing assets are created equally in our view, and risks abound.

One such risk: Rising rates on the horizon. We expect the Federal Reserve (Fed) to initiate its first rate hike in a year this December. The pace of Fed rate increases is likely to be gradual, meaning rates should stay low from a historical perspective for the foreseeable future.

Still, some popular high-yielding asset classes (such as traditional dividend-paying stocks and REITs) could potentially suffer as rates begin to slowly trend higher.

What does this mean for investors? Thoughtful diversification is key when it comes to the hunt for yield as 2016 draws to a close. Our colleague Matt Tucker’s recent post echoed the same sentiment. We particularly like these three ways to seek income now.

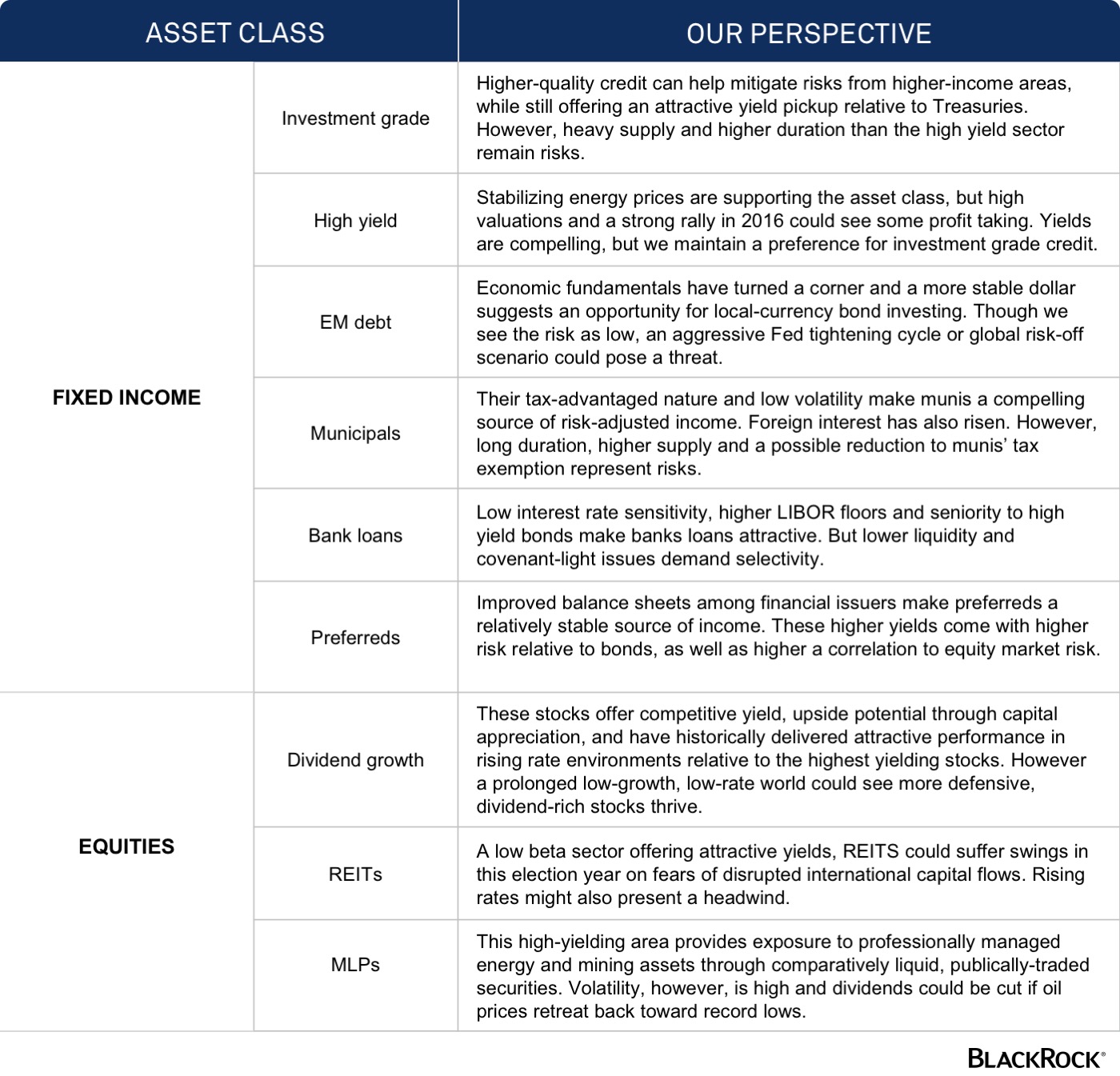

U.S. investment grade credit

Higher-quality credit can help mitigate risks from higher-income areas, while still offering an attractive yield pickup relative to Treasuries, we believe. However, heavy supply and higher duration than the high yield sector are risks, as is rising corporate leverage. High yield does represent a rare, income-producing bright spot and stabilizing energy prices are supporting the asset class. But high valuations and a strong rally in 2016 could see some profit taking in the high yield sector, so we generally prefer investment grade bonds.

International exposure via emerging market (EM) debt

This sector offers higher yield for a slight pickup in risk. Economic fundamentals have turned a corner and a more stable U.S. dollar suggests an opportunity for local-currency bond investing. But we have become more selective given rising valuations. We prefer the front end of local markets with room for EM central banks to cut rates further, such as in Brazil and emerging Asia. An aggressive Fed tightening cycle or global risk-off scenario could pose a threat to the asset class, though we see the risk as low.

Dividend growers

We think it is a good time for dividend-focused investors to divide stocks into dividend payers and dividend growers and balance out dividend portfolios. Dividend-paying stocks have performed strongly in a low-rate environment, but we believe they could suffer as rates rise.

In contrast, dividend growers have tended to outperform in a rising rate environment and typically have more stable payout ratios. These stocks generally offer competitive yield and upside potential through capital appreciation, and they have historically delivered attractive performance in rising rate environments relative to the highest yielding stocks. A prolonged low-growth, low-rate world could certainly see more defensive, divided-rich stocks thrive, but dividend growers do currently offer more attractive valuations.

Bottom line

It’s important to remember that all higher-yielding assets come with higher risks, but some of these risks appear more worth taking now. See the chart below for more on the opportunities and potential pitfalls we see for income investors today.

Terry Simpson, CFA, CAIA, is a multi-asset strategist for the BlackRock Investment Institute. He is a regular contributor to The Blog.

Investing involves risk, including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation and the possibility of substantial volatility due to adverse political, economic or other developments. These risks often are heightened for investments in emerging/developing markets, in concentrations of single countries or smaller capital markets.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of November 2016 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader.

©2016 BlackRock, Inc. All rights reserved. BLACKROCK are registered trademarks of BlackRock, Inc., or its subsidiaries. All other marks are the property of their respective owners.

USR-10828

© BlackRock

Read more commentaries by BlackRock