Donald Trump has been elected the 45th president of the United States, and both houses of Congress are now in Republican hands. Just as with Brexit, markets underestimated the strength of the populist movement. Trump struck a deep chord among lower and middle-class Americans reeling from manufacturing job losses over the past few decades, the slow economic recovery since the 2008 financial crisis and Washington’s lack of response in addressing these problems.

We believe that in the medium and longer term, the impact of Trump’s victory, although uncertain, may be positive for the US economy. Trump’s policies of lower regulation and lower taxes could be highly stimulative for US GDP growth. The wild card that could partly offset these pro-growth policies is his threat to be “tough-ontrade.” However, many in the all-Republican congress are generally supportive of free trade, so the political process may lead Trump to compromise, mitigating the more negative aspects of his trade platform.

Economy: Potential for Higher Economic Growth and a Wider Deficit

With a Republican House and Senate, Trump does not face Obama’s gridlock challenge. Many of his policies could be at least partially adopted. Areas in which Trump’s goals are consonant with those of the Republican party lower regulation, corporate tax reform and income tax cuts, as well as higher infrastructure and defense spending-could significantly boost economic growth. Corporate tax cuts could incentivize corporations to bring jobs back to the US and encourage increased business investment. In addition, Trump’s focus on reducing restrictions in the oil and gas sector, and reforming Obamacare, may be positive for the economy. Rising premiums for unsubsidized participants and penalties for non-participation related to Obamacare are creating headwinds for lower middle-income consumers. Addressing rising health care costs is essential to continued strong consumption, a major driver of US GDP growth.

The biggest uncertainty for future economic growth relates to trade policy. Trump has proposed imposing tariffs and rejecting trade agreements. He carried the election in part based on his promise to protect US jobs. We believe the Republican Congress could mitigate the more extreme aspects of his trade policies. It is important to note that Trump’s proposals to increase tariffs would involve a year-long administrative process, and any proposed repeal or revision of the North American Free Trade Agreement (NAFTA) would require Congressional approval.

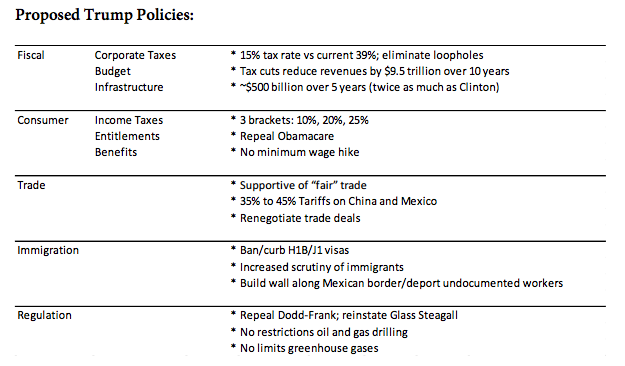

The following table summarizes key policies and programs proposed by Trump. If all his policies were fully adopted, the Committee for a Responsible Federal Budget estimates a $5.3 trillion increase in the federal debt over 10 years.

Market Impact: Potentially Positive in the Intermediate and Longer Term, with Rising Inflation

US and European markets have already recovered today from the sell-off following Trump’s victory. While the longer-term market impact of Trump’s victory is uncertain, corporate earnings may benefit from lower taxes, less regulation, and faster growth, helping boost both the US credit and equity markets. On the other hand, higher real yields caused by increased GDP growth, and rising inflation would be negative for the US Treasury markets.

Trump’s impact on the Federal Reserve will not be immediate. While Trump has been critical of Yellen, he cannot remove her as Chairman of the Federal Reserve until the end of her term in February 2018. However, he can appoint governors to fill the three vacancies coming up in 2017.

Fixed Income and Currency Markets

The Trump presidency may see rising US Treasury yields and inflation expectations, in response to the following factors:

-

The anticipated rate increase in December. We believe that the Federal Reserve may raise rates in December based on continued steady economic and inflation data. Should growth and inflation pick up from pro-growth policies, we might see a more aggressive Federal Reserve response in 2017.

-

Potential increases in deficit spending to fund tax cuts and increased infrastructure and defense spending.

-

Stable or improving US growth and improving global growth, as reflected in recent increase in global Purchasing Manager Indices. Higher growth may be accompanied by higher real yields or higher inflation.

-

Lower investment in Treasuries by foreign investors, most notably China.

-

Higher market and central bank uncertainty regarding the effectiveness of negative yields and extreme quantitative easing.

We see Treasury inflation-protected securities (TIPS) as a particularly attractive opportunity under Trump, as inflation may continue to rise, reflecting higher spending, accompanied by higher US debt levels. Credit sectors may benefit from Trump’s progrowth policies, in which US GDP growth and inflation increase. Given his success as a businessman, we would anticipate a corporate-friendly environment under a Trump administration.

The path of the US dollar is uncertain. It may benefit from an improving growth outlook, and relatively higher interest rates. Were Trump to move more aggressively on protectionist trade policies, the dollar could depreciate as foreign investment flows slow and inflation expectations rise. Emerging markets may face a mixed response.

Improving global growth and rising commodity prices may support these markets, although Trump’s protectionist trade policies may have a dampening effect on certain emerging markets.

Equities

While equities may suffer from volatility in the short term, it is possible with stronger global and US growth, equity markets may benefit in the longer term. Sectors that may benefit under a Trump administration include drug makers, financials, infrastructure, defense, coal and energy. Multinational companies that are heavily dependent on overseas sourcing may experience pricing pressure, given the possibility of more protectionist trade policies. In addition, hospital firms dependent on health care spending may be hurt with significant reform of Obamacare.

Market Outlook

Our market views remain broadly intact:

Fixed Income

- Developed markets sovereigns, including most US government debt, look unattractive.

- Investors are being poorly compensated for duration risk as a result of negative nominal yields and negative real yields. With yields so low and the yield curve flatter, shorter duration positions have become less costly.

- Corporate credit is generally more desirable than Treasuries. However, with the continuing rally in corporate credit over the past few months, we favor agency mortgage-backed securities (MBS) and other structured credit based on relative value. Within corporate credit, we continue to favor financials and, to a lesser extent, the energy midstream sector.

- Floating rate securities, including structured securities and event-linked (catastrophe) bonds, continue to be attractive to hedge interest rate risk, particularly in light of elevated LIBOR rates. LIBOR (London Interbank Offer Rate) is a key rate used by banks to price variable rate loans.

- With higher yields and stabilized commodity prices, select emerging market debt is attractive.

Equities

- We are more constructive on international equities than US equities given more attractive valuations abroad.

- We favor large-cap stocks over small-cap stocks, given their more attractive relative value.

- We also see opportunities in mid-cap stocks, many of which are reasonably valued given their growth prospects.

- Within the cyclical area of the economy, we believe the technology sector may benefit due to earnings growth, driven by the shift to mobile and cloud computing. We also believe financials stocks are attractively valued and can do well in a rising interest rate environment.

- Health care, is likely to be volatile due to political rhetoric related to pricing, but should perform well overall due to continued innovation and consolidation. Conversely, telecommunications and utilities may underperform as interest rates rise.

Important Information

Unless otherwise stated, all information contained in this document is from Pioneer Investments and is as of November 9, 2016. The views expressed regarding market and economic trends are those of the author and not necessarily Pioneer Investments, and are subject to change at any time based on market and other conditions and there can be no assurances that countries, markets or sectors will perform as expected. These views should not be relied upon as investment advice, as securities recommendations, or as an indication of trading on behalf of any Pioneer Investments product. There is no guarantee that market forecasts discussed will be realized or that these trends will continue.

Investments involve certain risks, including political and currency risks. Investment return and principal value may go down as well as up and could result in the loss of all capital invested. This material does not constitute an offer to buy or a solicitation to sell any units of any investment fund or any services.

Pioneer Investments is a trading name of the Pioneer Global Asset Management S.p.A. group of companies.

Date of First Use: November 9, 2016.

www.pioneerinvestments.com

Read more commentaries by Pioneer Investments