Rick Rieder talks about the improving wage growth and a tight jobs market having a possible impact on the Federal Reserve's rate hike decision in December.

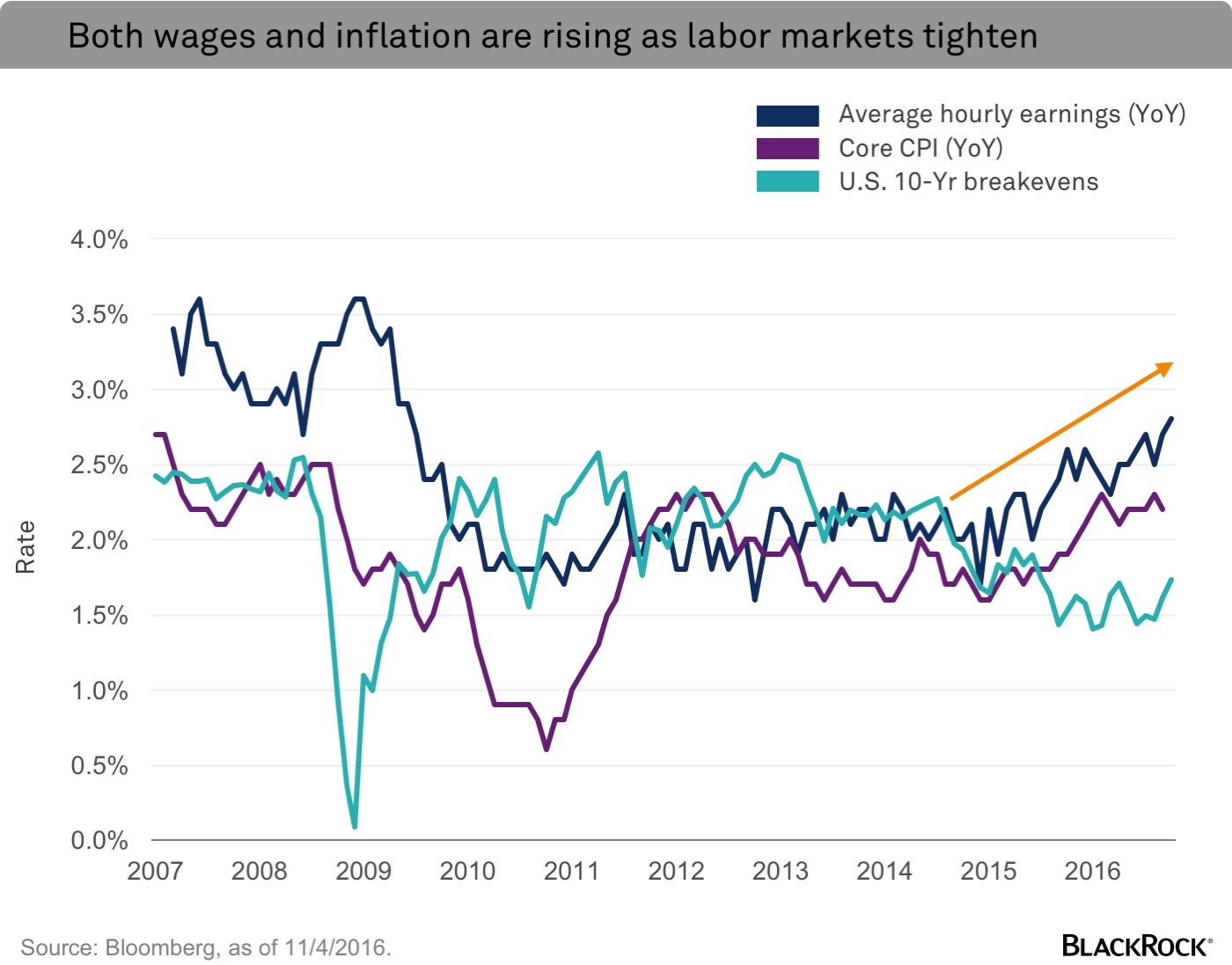

One of the most important indicators highlighting the tightness of the U.S. labor market today: recent improvement in wage growth. The October jobs report saw average hourly earnings rise by an impressive 0.4% on the month, above the consensus estimate of 0.3%. Average hourly earnings are now growing at 2.8% year-over-year, the most since June 2009, and rising wages are pushing up inflation. See the chart below.

The leisure and hospitality sectors are partly behind this wage growth. These “low wage” (in terms of dollar/hour pay) sectors have been regions of robust hiring in recent years as well as areas of the economy that have seen significant consumer spending. Industries such as utilities and information technology are also seeing growing wages.

I expect labor market tightness to continue to put upward pressure on wages through the remainder of the year. Of course, what happens with minimum wage policies is important to watch. When wage costs are increased through policy rather than via market mechanisms, revenues and profits (and hiring) can take a hit unless businesses can exhibit pricing power to correspondingly increase what they charge end customers to offset their own labor cost increases.

Where does this leave us from a monetary policy perspective?

The utility of extraordinarily low interest rate levels in effectively stimulating real economic growth has long since passed. It is extraordinary to think that the Federal Reserve (Fed) last cut its policy rate in December 2008, and in the 63 FOMC policy meetings since, it has only moved rates once (a 25 basis point hike last December), while the economic, employment and financial market landscape has changed markedly throughout this time.

Yet the Fed may hold off on a rate increase next month following Donald Trump’s surprise election win, as we write in our BlackRock Bulletin on the election outcome. But a lot can happen between now and then. If markets are stable and labor markets don’t dramatically falter in coming weeks, a quarter-point hike in December is still likely. In other words, if conditions allow it, I believe the Fed will move this year. In the meantime, as October’s payroll report underscored, the U.S. economy is running very close to full employment.

Rick Rieder, Managing Director, is BlackRock’s Chief Investment Officer of Global Fixed Income and is a regular contributor to The Blog.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of November 2016 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader.

©2016 BlackRock, Inc. All rights reserved. BLACKROCK is a registered trademark of BlackRock, Inc., or its subsidiaries. All other marks are the property of their respective owners.

© BlackRock

Read more commentaries by BlackRock