Executive Summary:

- The chase for dividend yield has created bloated valuations in some sectors.

- Free cash flow yield can provide insight into a company’s strength.

- Paying out too high a dividend can limit a company’s path forward.

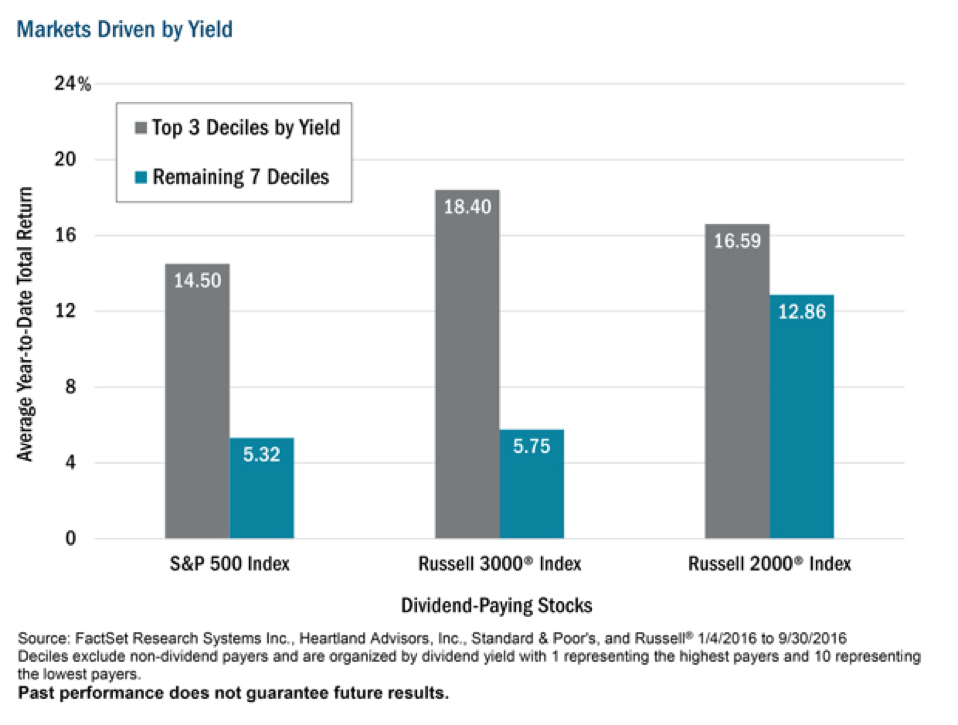

The hunt for dividends has shown little sign of slowing. Through the first nine months of the year, the top 30% of names based on yield in the S&P 500 outperformed the remaining stocks by more than 900 basis points on average. Other major indices have seen similar results as the struggle to replace income formerly generated by bonds continues.

The upward climb coincides with nearly eight years of historically low yields for fixed income. Adding to the effect is the heightened importance placed on low-volatility/high-momentum stocks. The combination creates a feedback loop where stocks are bid up for their yield and then additional buyers enter because shares have performed well and price movements are stable.

A Widespread Issue

Utilities and Real Estate Investment Trusts (REITs) top the list of sectors where the pursuit of income has produced frothy valuations. Despite a third-quarter pullback in power companies, the sector in the S&P 500 still trades at 17.1x estimated 2017 earnings—well above its 20-year average of 13.6. Real estate is at similar levels. While the two areas are the most obvious, the phenomenon is widespread.

Yielding to Reason

Many of our portfolios have a dividend focus, including our Mid Cap Value Strategy, however, we believe a process that focuses solely on the ratio of payments to share price is shortsighted and could be costly over the long term. Instead, we look at current dividend rates as a single piece of a bigger picture including free cash flow yield and payout ratio. Using these two measures is consistent with our long-term value focus.

Even the most attractive dividend rates will lose their appeal if they become unsustainable. To that end, we look at how much income a business generates after paying its expenses as an indicator of whether cash distributions will endure. If a company’s cash flow is shrinking, it likely won’t be able to continue to pay investors at current levels. However, a business that generates increasing profits is better positioned to maintain or expand dividends.

Too Much of a Good Thing?

While dividends can be a welcomed aspect of total return, as long-term investors we want management to be prudent about the amount of income it returns to shareholders. We look to payout ratios to help gauge whether a business is being too aggressive in distributing cash. Put simply, businesses that are paying out a relatively small portion to shareholders have greater flexibility to increase dividends in the future or could use retained cash to invest in expansion or pay down debt.

A Closer Look Exposes Big Differences

The following example of two dividend-paying names illustrates how looking beyond dividend yield is integral to comparing potential investments. We’ve chosen these businesses to show how free cash flow yield and payout ratio can help uncover the more compelling opportunity when looking for high yielding equities.

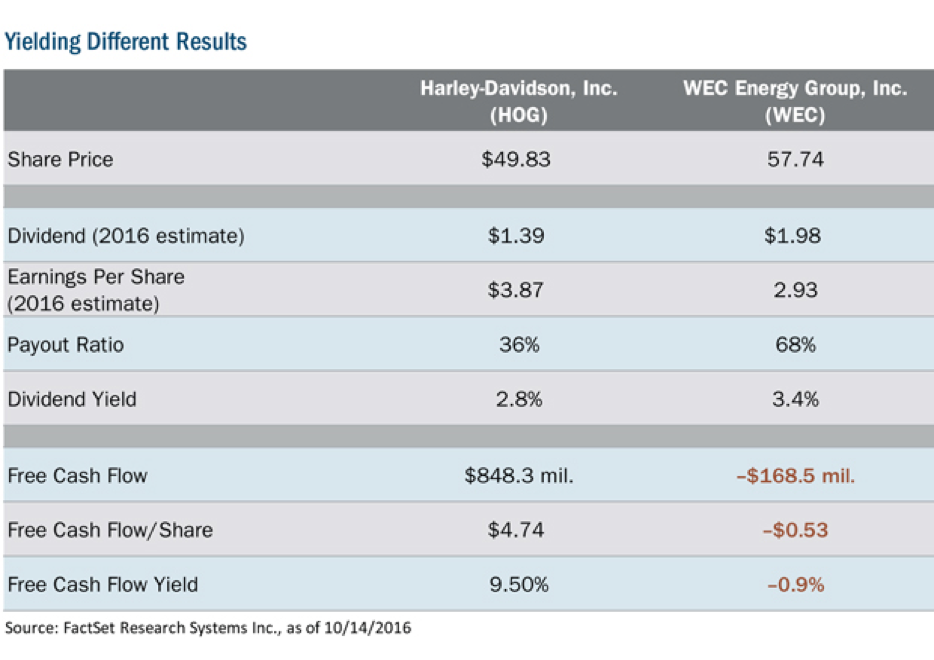

Motorcycle manufacturer Harley-Davidson, Inc. (HOG)—a holding in our mid-cap portfolio—controls more than 50% of the domestic new market and has a strong following in Japan, Canada, and Europe. WEC Energy Group, Inc. (WEC) is a utility operating primarily in Wisconsin and Illinois.

Harley Davidson’s forward dividend rate is $1.39 per share. At a share price of $49.83 on October 14, its forward yield was approximately 2.8%. WEC’s forward dividend rate is $1.98 per share and it was trading at $57.74 on October 14. Therefore, its forward dividend yield was 3.4%. For income hungry investors the dividend rate of the companies may make WEC appear to be the more attractive stock.

However, a look at free cash flow yield makes the case for WEC less clear. During its latest fiscal year, the utility generated a negative $0.53 per share in free cash flow, which translates to a yield of -0.9%. By contrast, the motorcycle manufacturer generated $4.74 per share in cash during its most recent fiscal year, resulting in a yield of 9.5%. The upshot is that Harley is generating cash per share, unlike WEC, and the income can be used to either increase future dividends or used to pay for growth or to reduce debt.

Some may still be tempted to hold the utility due to its recent performance and the sector’s history of relatively stable stock prices.

The ability of both companies to fund growth opportunities and/or increase dividends, we believe, will have an impact on future returns and stability. Harley has a payout ratio of approximately 33%, meaning that 67 cents of each dollar in profit is available for paying down debt, sustaining a dividend during a sales slump or reinvesting to grow the business. By contrast, WEC pays 68% of its net income out in dividends, meaning it has far less room to raise distributions, pay down debt or fund growth.

By digging deeper into the numbers that affect dividend yield, we are able to add an additional layer of evaluation when determining whether a company offers a compelling opportunity. We use this analysis alongside our 10 Principles of Value Investing™ as an attempt to ensure we don’t overpay for businesses that offer attractive dividend yields.

Disclosure:

Past performance does not guarantee future results.

Investing involves risk, including the potential loss of principal. There is no guarantee that a particular investment strategy will be successful.

Dividend-paying stocks cannot eliminate the risk of investment losses. Dividends are not guaranteed and a company’s future ability to pay dividends may be limited. A company currently paying dividends may cease paying dividends at any time.

Value investments are subject to the risk that their intrinsic values may not be recognized by the broader market.

The Mid Cap Value Strategy seeks long-term capital appreciation by investing in mid-size companies as defined by the market capitalization range of the Russell Midcap® Index. This focused portfolio seeks companies with strong underlying business franchises priced at a discount to their intrinsic worth that have temporarily fallen out of favor.

As of 9/30/2016, Heartland Advisors on behalf of its clients held approximately <0.01% and 0.00% of the total shares outstanding of Harley-Davidson, Inc. and WEC Energy Group, Inc., respectively. Statements regarding securities are not recommendations to buy or sell. Portfolio holdings are subject to change. Current and future holdings are subject to risk.

The statements and opinions expressed in this article are those of the presenter(s). Any discussion of investments and investment strategies represents the presenter’s views as of the date created and are subject to change without notice. The opinions expressed are for general information only and are not intended to provide specific advice or recommendations for any individual. The specific securities discussed above, which are intended to illustrate the advisor’s investment style, do not represent all of the securities purchased, sold, or recommended by the advisor for client accounts, and the reader should not assume that an investment in these securities was or would be profitable in the future. Certain security valuations are based on Heartland Advisors’ estimates. Any forecasts may not prove to be true. Economic predictions are based on estimates and are subject to change.

Sector and Industry classifications as determined by Heartland Advisors may reference data from sources such as FactSet Research Systems, Inc. or the Global Industry Classification Codes (GICS) developed by Standard & Poor’s and Morgan Stanley Capital International.

Definitions: 10 Principles of Value Investing™ consist of the following criteria for selecting securities: (1) catalyst for recognition; (2) low price in relation to earnings; (3) low price in relation to cash flow; (4) low price in relation to book value; (5) financial soundness; (6) positive earnings dynamics; (7) sound business strategy; (8) capable management and insider ownership; (9) value of company; and (10) positive technical analysis. Basis Point (bps): is a unit that is equal to 1/100th of 1% and is used to denote the change in a financial instrument. Dividend Yield: is a ratio that shows how much a company pays out in dividends each year relative to its share price. Earnings Per Share: is the portion of a company’s profit allocated to each outstanding share of common stock. Free Cash Flow: is the amount of cash a company has after expenses, debt service, capital expenditures, and dividends. The higher the free cash flow, the stronger the company’s balance sheet. Free Cash Flow Yield: is calculated as the free cash flow a company has divided by either its current market price per share or enterprise value. Momentum: is the rate of acceleration of a security's price or trade volume. Payout Ratio: is the percentage of dividend earnings paid to shareholders. It is calculated by dividing yearly dividend per share by earnings per share. Price/Earnings Ratio: of a stock is calculated by dividing the current price of the stock by its trailing or its forward 12 months’ earnings per share. Real Estate Investment Trust (REIT) is a security that sells like a stock on the major exchanges and invests in real estate directly, either through properties or mortgages. Volatility: is a statistical measure of the dispersion of returns for a given security or market index which can either be measured by using the standard deviation or variance between returns from that same security or market index. Commonly, the higher the volatility, the riskier the security. Russell 3000® Index: is a market capitalization weighted equity index maintained by the Russell Investment Group that seeks to be a benchmark of the entire U.S. stock market and encompasses the 3,000 largest U.S.-traded stocks, in which the underlying companies are all incorporated in the U.S. Russell 2000® Index: includes the 2000 firms from the Russell 3000® Index with the smallest market capitalizations. S&P 500 Index: is an index of 500 U.S. stocks chosen for market size, liquidity and industry group representation and is a widely used U.S. equity benchmark. All indices are unmanaged. It is not possible to invest directly in an index.

Russell Investment Group is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group.

Data sourced from FactSet: Copyright 2016 FactSet Research Systems, Inc., FactSet Fundamentals. All rights reserved.

CFA® is a registered trademark owned by the CFA Institute.

©2016 Heartland Advisors

heartlandadvisors.com

2016448

© Heartland Advisors

Read more commentaries by Heartland Advisors