MLPs: Back on Track After Last Year's Slump?

What yield-seeking investors need to know about this expanding asset class

This year, I’ve written several blogs highlighting the strong performance of alternative assets, including real estate, commodities and infrastructure. In this installment, I want to give particular focus to an area that many investors may not be familiar with, but that offers the potential for attractive returns, income, inflation hedging and portfolio diversification — master limited partnerships (MLPs).

Introduction to MLPs

Before delving into the performance of MLPs, and the factors behind the numbers, I want to first offer some background about their history and potential benefits.

MLPs are publicly traded limited partnerships that are focused on energy infrastructure in the US. Pipelines, storage facilities and processing plants are all examples of assets that MLPs own, operate and build. As of the end of 2015, there were approximately 180 MLPs, with a market capitalization of more than $300 billion.1

MLPs are typically classified into three categories:

- Upstream, which are involved in the exploration, recovery, development and production of crude oil and natural gas

- Midstream, which are involved in the gathering, processing, storage and transportation of oil and gas

- Downstream, which are involved in the distribution of fuels to end customers, such as homes, businesses and factories.

Given that MLPs are limited partnerships, they do not pay federal income tax. Rather, MLPs pass their income on to the limited partners, who are then subject to income tax. Also, unlike many limited partnerships that are privately placed and offer limited liquidity, MLPs are publicly traded and provide investors with the same liquidity as a publicly traded stock.

MLPs are expected to fuel energy infrastructure expansion

Energy production in the US has evolved over the past decade. While crude oil and natural gas production declined by about 20% from 1980 to 2006,2 that trend has reversed over the past 10 years thanks to new technologies, especially fracturing technology, which have allowed the extraction of hydrocarbons from previously uneconomical locations. As a result, the US Energy Information Administration estimates that energy production in the US could grow by 77% from 2006 levels by 2030.2

The increasingly diverse geography of US energy production, combined with the increase in US energy production overall, has created a strong need for additional energy infrastructure. To this end, the American Petroleum Institute estimates that it will take $890 billion in total direct investment of oil and gas transportation and storage infrastructure through 2025 to support US energy production levels.3 MLPs are expected to play an important role in providing the capital to build this needed infrastructure.

As energy production in the US has evolved, so too have MLPs. Today, most MLPs primarily focus on midstream energy infrastructure and natural gas, as it provides the plumbing that transports and stores oil and gas. Furthermore, revenue from midstream infrastructure is based on the volume of oil and gas processed, which tends to be insulated from fluctuations in the price of oil and gas.

MLPs have posted solid performance thus far in 2016

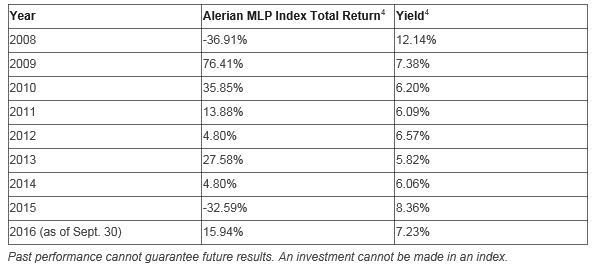

As you can see from the chart below, MLPs have provided an attractive level of yield over the past several years. From a return perspective, it’s clear that while MLPs have the potential to generate attractive returns, they can also experience sharp losses and returns can be quite volatile. For example, after posting a negative total return in 2015, as represented by the Alerian MLP Index, MLPs rebounded this year to post a positive total return as of Sept. 30, 2016.

Annual performance and yield of MLPs since the financial crisis

While many investors may assume that oil prices are the biggest determinant of MLP performance, especially since MLPs and oil both fell in 2015, correlations between oil prices and MLP performance are relatively low over the longer term.5 MLP performance has historically been tied more closely to the level of energy production in the US. Additionally, natural gas, not oil, is the primary focus of most MLPs.

However, last year the correlation between MLPs and oil prices were higher than usual,5 as investors may have been concerned about whether the US could sustain its record output of oil production in the face of low prices. As a result, we believe last year’s MLP market was overbuilt from an oil production standpoint, leading to volatility in the MLP market that hasn’t been seen since the global financial crisis.

Today, we believe the MLP market presents a better risk/reward opportunity, as evidenced by the positive performance so far this year. We also believe US oil production is sustainable, particularly in West Texas, which helps make the case for long-term exposure to MLPs.

It’s important that investors understand the correlation between oil and gas prices and MLP performance, as it’s clear, from a return perspective, that while MLPs have the potential to generate attractive returns, they can also experience sharp losses.

Ways to invest in MLPs

There can be distinct advantages and disadvantages to the various investment vehicles that investors choose for their MLP exposure – whether it’s investing directly in MLPs, or through open-end mutual funds and exchange-traded funds (ETFs). Each individual’s situation is unique, so selecting the right vehicle is important.

For example, some investors might not want to deal with the paperwork involved with a direct MLP investment, namely the Schedule K-1 process and the requirement to file state income taxes in each state where the MLP operates.

Other investors may not be aware that open-end mutual funds and ETFs pay corporate-level taxes, which can potentially eat into the performance of the underlying MLPs, but also alleviate the tax filing burdens because the funds handle the K-1 process by providing shareholders with 1099s instead.

What’s more, potential investors need to be aware that open-end mutual funds and ETFs tend to offer more diversification than buying MLPs directly.

Learn more about MLPs

Talk to your advisor about MLPs if you’re seeking an investment that has the potential to generate attractive returns, provide attractive levels of current income, serve as a hedge against inflation and/or provide portfolio diversification.

Learn more about Invesco MLP Fund.

Learn more about the MLP & Income Portfolio.

Learn more about alternative investing.

Walter Davis

Alternatives Investment Strategist

As Alternatives Investment Strategist, Walter Davis serves as Invesco’s primary alternatives representative to retail, high net worth and institutional clients across the major broker dealers, wirehouses and RIAs. He is responsible for collaborating across Invesco’s alternative strategies to develop a cohesive alternatives education program for financial advisors and investors.

Prior to joining Invesco in 2014, Mr. Davis served as a managing director in Morgan Stanley’s Alternative Investments Department, and earlier as director of High Net Worth and Institutional Sales. Prior to Morgan Stanley, he worked at Chase Manhattan Bank in the Alternative Investments Department. He has worked in the industry since 1991.

Mr. Davis graduated cum laude with a BA in economics from the University of the South. He earned an MBA in finance and international business from Columbia Business School. He holds the Series 3, 7, 24 and 63 registrations.

Important information

Blog header image: wang song/Shutterstock.com

1. Source: Alerian, as of Dec. 31, 2015

2. Source: US Energy Information Administration, Dec. 4, 2014

3. Source: “Oil & Natural Gas Transportation & Storage Infrastructure: Status, Trends, & Economic Benefits,” IHG Global Inc., December 2013

4. Source: Alerian. The Alerian MLP Index is a composite of the 50 most prominent energy master limited partnerships calculated by Standard & Poor’s using a float-adjusted market capitalization methodology.

5. Sources: Bloomberg L.P., StyleADVISOR. Based on 10-year correlation of 0.48 and 2015 correlation of 0.55 between the Alerian MLP Index and West Texas Intermediate oil prices, as of Dec. 31, 2015

Correlation is the degree to which two investments have historically moved in relation to each other.

Most MLPs operate in the energy sector and are subject to the risks generally applicable to companies in that sector, including commodity-pricing risk, supply-and-demand risk, depletion risk and exploration risk. MLPs are also subject the risk that regulatory or legislative changes could eliminate the tax benefits enjoyed by MLPs which could have a negative impact on the after-tax income available for distribution by the MLPs and/or the value of the portfolio’s investments.

Diversification does not guarantee a profit or eliminate the risk of loss.

Before investing, investors should carefully read the prospectus and/or summary prospectus and carefully consider the investment objectives, risks, charges and expenses. For this and more complete information about the fund(s), investors should ask their advisors for a prospectus/summary prospectus or visit invesco.com/FundProspectus.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC, investment adviser. Invesco PowerShares Capital Management LLC (Invesco PowerShares) and Invesco Distributors, Inc., ETF distributor, are indirect, wholly owned subsidiaries of Invesco Ltd.All data provided by Invesco unless otherwise noted.

©2016 Invesco Ltd. All rights reserved.

MLPs: Back on track after last year’s slump? by Invesco