Pedal to the Metals: There's More to Commodities Than Just Crude Oil Futures

Three reasons to consider commodities in today’s market

Last month, I outlined proposed crude oil production cuts tentatively agreed to by the members of the Organization of Petroleum Exporting Countries (OPEC). Since then, Iraq, Libya and Nigeria have requested an exemption, which has led some hedge funds to short crude in the belief that an OPEC agreement is doomed to fail.

But the market is neglecting to consider that none of these three countries is in a position to meaningfully increase crude oil exports in the near term. In fact, these three players have much to lose from lower crude oil prices. As such, I believe a formal agreement to limit production is more likely than not. Whether or not OPEC takes coordinated action, economic forces continue to rebalance the physical market – likely pushing crude oil prices slowly higher as demand trends outstrip supply over the coming months and years.

Of course, there is more to the current commodity story than just crude oil. Both precious metals and industrial metals are up over 20% so far in 2016.1 Metals and agriculture have often shown strength during volatile retracements in energy commodities this year, smoothing out the ride for commodity investors.

On balance, commodity performance is benefiting from a cyclical rebound that we forecast earlier this year. In fact, commodities, as defined by the DBIQ Optimum Yield Diversified Commodity Index Excess Return, are up over 18% since we published our outlook in that February blog post.1

A compelling entry point for commodity exposure

With industrial metals showing continued upside momentum and crude oil prices back down to the mid-$40 per barrel range, I believe now is a good time to consider adding diversified exposure to the commodity markets.2 In addition to a positive outlook for commodity prices, there are three foundational principles that support the inclusion of commodities in a diversified portfolio, in my view.

- Commodities as a portfolio diversifier – As illustrated in the graphic below, commodities have historically demonstrated low correlations to both equities and fixed income securities. This has important implications for diversification. While diversifying a portfolio does not guarantee a profit or eliminate the risk of loss, commodities can potentially smooth out the return profile of a portfolio made up primarily of stocks and bonds.

Historical correlation of commodities to equities & fixed income

- Commodities as a potential hedge against inflation – Given recent increases in average hourly earnings and the surprise election results in the US, inflation expectations have ratcheted sharply higher. Commodities have historically demonstrated the highest correlation to the consumer price index (CPI), which is used to gauge inflation in the United States. Over the past 15 years, commodities have experienced a 0.4 correlation to changes in the CPI. This compares to a 0.2 correlation with the CPI for Treasury Inflation-Protected Securities.1

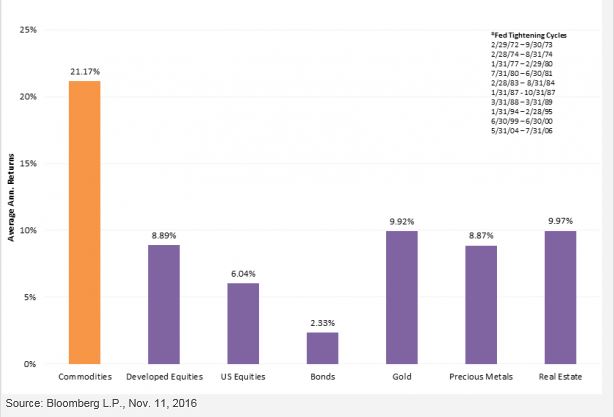

- Commodities as a top-performing asset class during Federal Reserve rate hikes – Short-term interest rates tied to Libor are on the rise, spurred in part by money market reforms that have driven some investors out of short-term paper issued by private institutions and into government debt instruments. Many market participants are also expecting the Federal Reserve to increase the targeted fed funds rate by at least 25 basis points within the next few months. Since 1972, commodities have been the top-performing asset class during Fed rate hike cycles, as depicted in the graphic below.

Investors looking for a convenient and cost-effective way to invest in the commodity markets may wish to consider PowerShares’ lineup of commodity ETFs. PowerShares ETFs feature a rules-based, optimized yield strategy that seeks to optimize futures roll yield.

1 Source: Bloomberg L.P., Nov. 11, 2016

2 Source: Bloomberg L.P., Nov. 14, 2016

Jason Bloom

Director of Commodities and Alternatives Product Strategy

Invesco PowerShares Capital Management LLC

Jason Bloom is the Director of Commodities and Alternatives Product Strategy for Invesco PowerShares. Mr. Bloom leads the Alternatives Product Strategy Team and is responsible for delivering the team’s macro views on commodities, alternatives and portfolio construction guidance. He joined Invesco PowerShares in 2015.

Prior to joining Invesco PowerShares, Mr. Bloom served as an ETF strategist for six years with Guggenheim Investments and later River Oak ETF Solutions. Previously, Mr. Bloom spent seven years as a professional commodities trader specializing in arbitrage strategies in both the energy and US Treasury markets.

Mr. Bloom earned a BA degree in economics from Gustavus Adolphus College in 1994, and a JD from the University of Iowa College of Law in 1999.

Important information

Commodities may subject an investor to greater volatility than traditional securities such as stocks and bonds and can fluctuate significantly based on weather, political, tax, and other regulatory and market developments.

Correlation is the degree to which two investments have historically moved in relation to each other.

The consumer price index measures change in consumer prices as determined by the US Bureau of Labor Statistics.

Libor (London Interbank Offered Rate) is a benchmark rate that some of the world’s leading banks charge each other for short-term loans.

Treasury Inflation-Protected Securities (TIPS) are US Treasury securities that are indexed to inflation.

The BofA Merrill Lynch Global Diversified Inflation-Linked Index is a broad, market-value weighted, capped total-return index designed to measure the performance of inflation-linked sovereign debt that is publicly issued and denominated in the issuer’s own domestic market and currency.

The BofA Merrill Lynch US Inflation-Linked Treasury Index is an unmanaged index comprised of US Treasury Inflation-Protected Securities with at least $1 billion in outstanding face value and a remaining term to final maturity of greater than one year.

The Bloomberg Barclays US Aggregate Bond Index is an unmanaged index considered representative of the US investment-grade, fixed-rate bond market.

The DBIQ Optimum Yield Diversified Commodity Index is a rules-based index composed of futures contracts on 14 of the most heavily-traded and important physical commodities in the world.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC, investment adviser. Invesco PowerShares Capital Management LLC (Invesco PowerShares) and Invesco Distributors, Inc., ETF distributor, are indirect, wholly owned subsidiaries of Invesco Ltd.

©2016 Invesco Ltd. All rights reserved.

Pedal to the metals: There’s more to commodities than just crude oil futures by Invesco