Since its founding 35 years ago, The Leuthold Group has utilized a distinctive blend of quantitative, fundamental, and technical analysis to guide its investment activities. These disciplines are focused on value recognition, trend analysis, and leadership expectations, all of which influence our portfolio management and tactical-allocation decisions. While quantitative techniques have been around for decades, a recent incarnation of this investment style has taken the industry by storm. Factor investing (also known as smart beta or strategic beta, among other terms) has become the hottest portfolio management trend in the last five years. Morningstar estimates that 700 funds (primarily ETFs) now populate the smart beta space with assets under management exceeding $600 billion.

Smart beta is a generic version of quantitative investing, kith and kin to the disciplines used at firms such as ours. This article is the first in a series we plan to publish on the topics of smart beta and popular quantitative methods. Our motivation is threefold: 1) it’s essential for investors to have a solid grasp of this growing and important industry phenomenon; 2) examining these products may assist us in optimizing our own security selection and tactical tools; and 3) every active manager needs to understand how factors are influencing the structuring, risk positioning, and performance attribution of their portfolios, even if they do not use factors in their decision-making process.

Interest in factor investing has exploded in recent years as investors have searched for a “better way” after the market crash of 2008-09. This discipline traces its roots back to academia, where researchers have spent decades looking for market “anomalies.” Simply put, anomalies are characteristics or traits that appear to cause some assets to provide superior risk-adjusted returns beyond the level expected by the Capital Asset Pricing Model (which holds that excess return can only come from taking more systematic risk). Over the years, researchers have discovered many characteristics that seem to generate excess return without requiring excess risk or superior investment skill. The beginnings of factor investing are often traced back to Fama and French’s 1992 paper which proposed that Value stocks and Small Cap stocks earn unexpected excess returns. Academics have identified hundreds of possible factors since then but, as we shall enumerate later, the industry has latched on to fewer than ten as having true merit.

Factor Research

The academic research that has spawned the smart-beta movement is based on the notion that securities (primarily stocks) have common characteristics/attributes/traits that cause them to reliably produce excess returns. Studies are designed to define such attributes and identify the size and consistency of the excess return. Research generally assigns 1% to 4% per year of excess return to the factor in question, and attractive Sharpe ratios often signify the factor’s superior risk-adjusted return. Based on the notion that a basket of stocks with the positive attribute should be expected to outperform the market going forward, as it has in the past, practitioners build off this research to create a portfolio management process that captures the factor in a methodical and repeatable fashion.

In evaluating which of the scores of factors identified by academic research that are most likely to continue generating excess return, practitioners have zeroed in on a preferred set of criteria to determine the credibility of each candidate.

-

The factor return must be persistent; it should appear in a variety of market environments and recur over time.

- The factor should be present in multiple countries and sectors. A factor that works in just one market may be the result of an idiosyncrasy particular to that market rather than a true return driver.

- The factor should work across small changes in definition. A factor that only works using a specific narrow definition is less trustworthy than a factor that is robust across similar definitions of the characteristic.

- The factor should have an economic or behavioral reason to work.

One of the key analytical questions with any return anomaly is identifying the reason that the factor works. Data mining can uncover all sorts of positive-return correlations (remember the Super Bowl indicator?) but academics and practitioners insist that a factor have some basis for success, providing confidence that the results are not just random noise. One explanation centers on efficient-market theory, proposing that a return factor works because the investor has taken on increased risk to earn the excess return. The other explanation is behavioral in nature, and holds that a factor may deliver excess return because of persistent investor-behavioral errors which cause assets to be routinely over or under priced. Efficient market theory and behavioral errors are both plausible explanations for factor returns and each has the potential to remain viable into the future.

Having identified a believable return driver, one must next determine which stocks have a positive or negative exposure to that factor and o decide how to assemble them into a coherent portfolio. Neither of these is a simple task, and successfully resolving these difficulties reveals why factor investing is much closer to an active endeavor than a passive one.

Widely Accepted Factors

We have held you in suspense long enough! Here are the return factors widely accepted as meeting the criteria described and that have been incorporated into smart-beta ETFs which have attracted billions of dollars in assets under management.

-

Value: stocks selling at low valuation levels outperform those selling at high valuation levels.

-

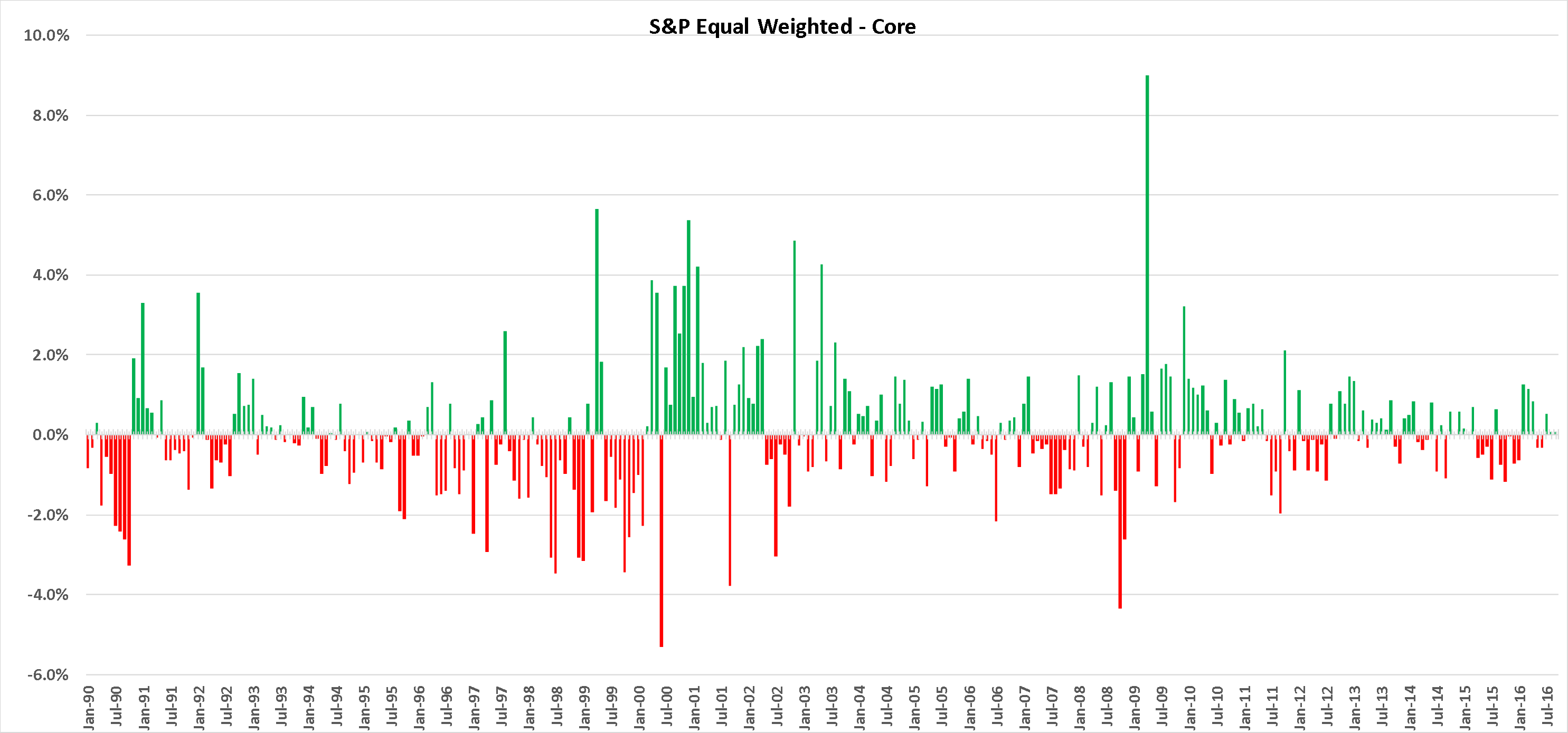

Size: small capitalization companies outperform larger cap companies.

-

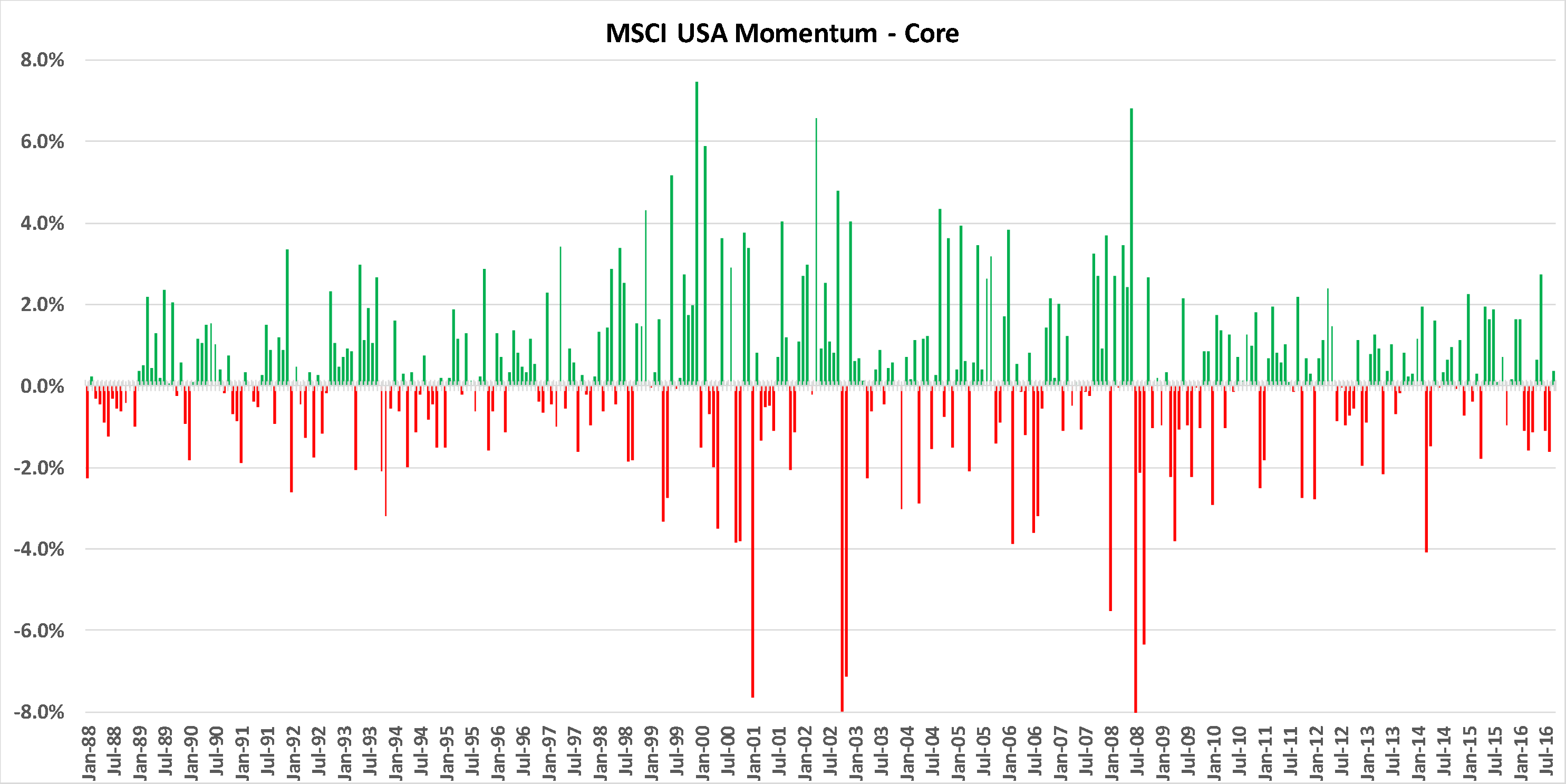

Momentum: stocks that have outperformed over the last year will continue to outperform.

-

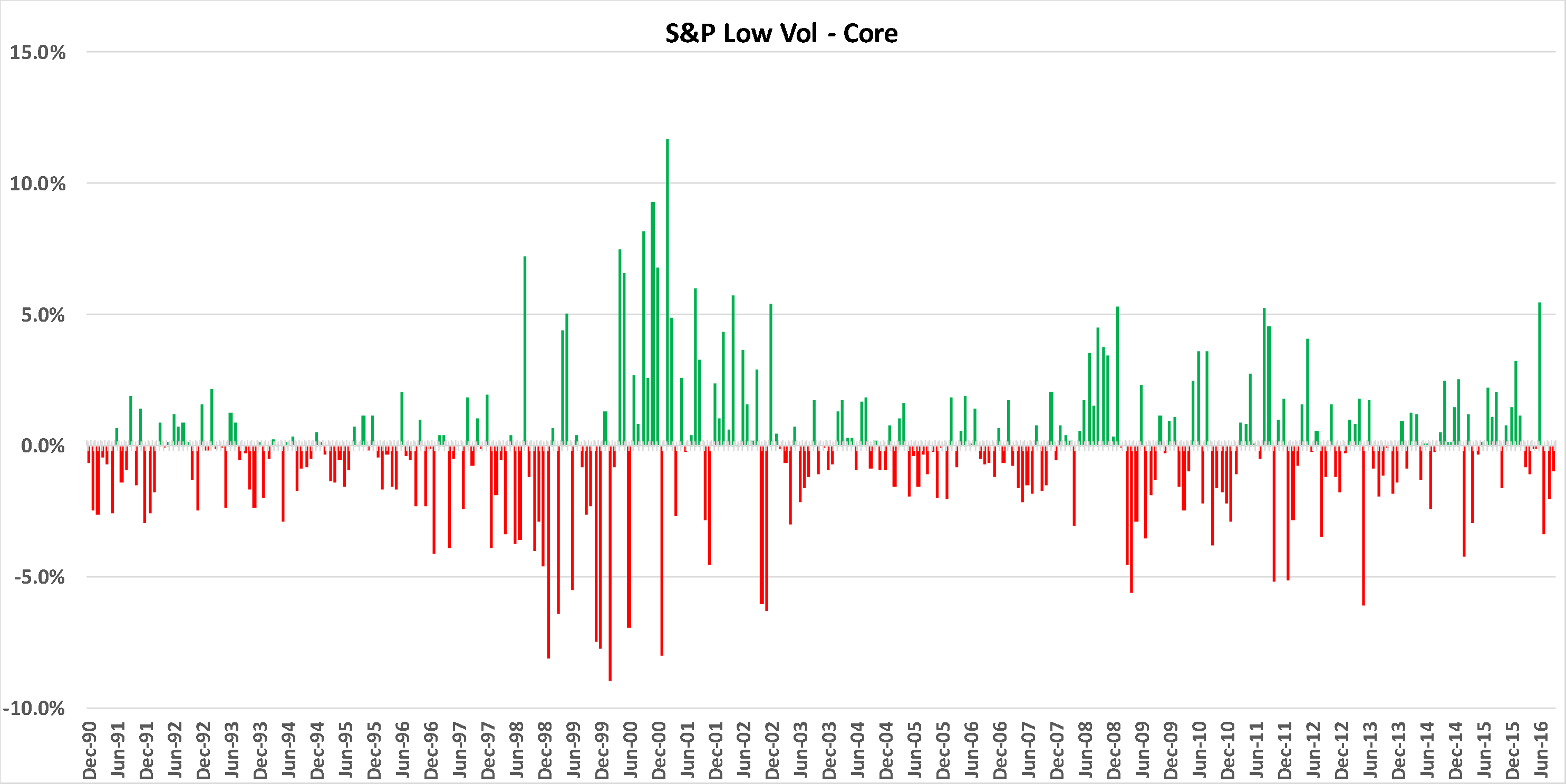

Low Volatility: less volatile stocks/portfolios will outperform higher volatility stocks/portfolios.

-

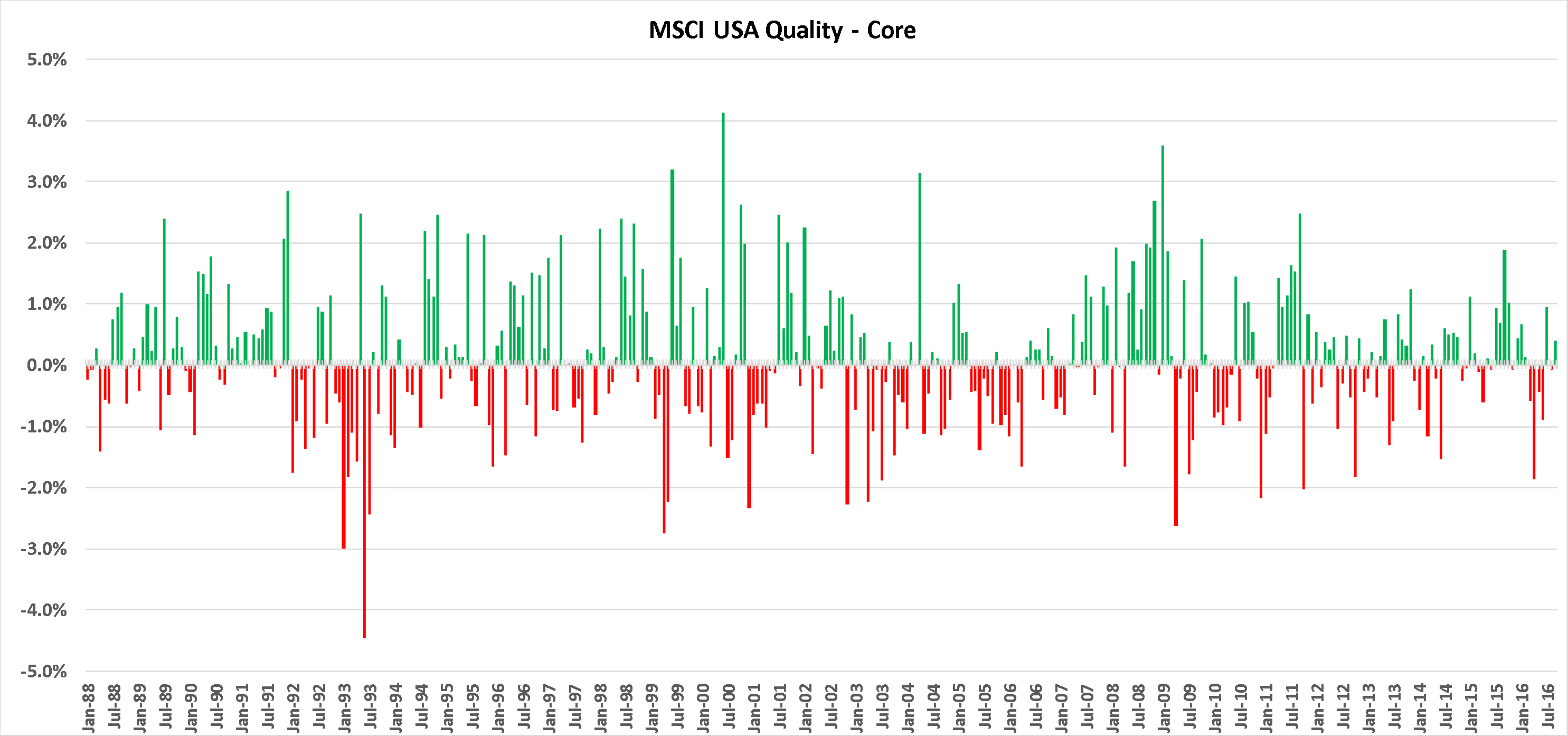

Quality: higher quality stocks will outperform lower quality stocks. (We include the “Profitability” factor in this general category.)

-

Dividends: higher yield stocks will outperform lower yield stocks.

A security’s positive or negative exposure to a certain factor is called its “beta” or “loading.” By selecting stocks with positive exposure to intelligently selected factors or attributes, we see the derivation of the popular terminology “smart beta.” Indexes and portfolios are designed to hold companies with high exposures to the factor, thereby harvesting the excess return associated with the anomaly.

Factor Returns

S&P and MSCI have each developed a set of indexes to track relative performance over time. We’ve selected the longer-running index series for each factor (S&P or MSCI) and plotted the rolling twelve-month excess return versus the U.S. market. If employing the S&P series we compare the factor index to the S&P 500; for an MSCI series we compare the factor index to the MSCI USA core index.

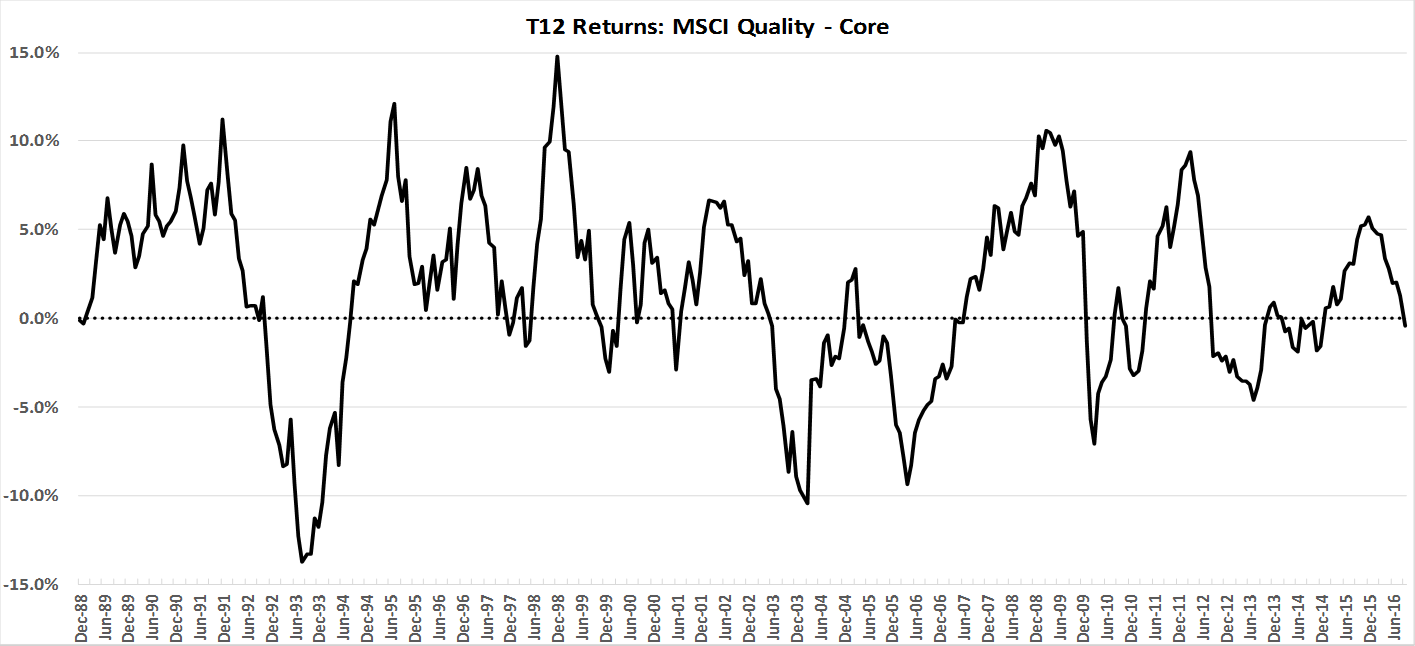

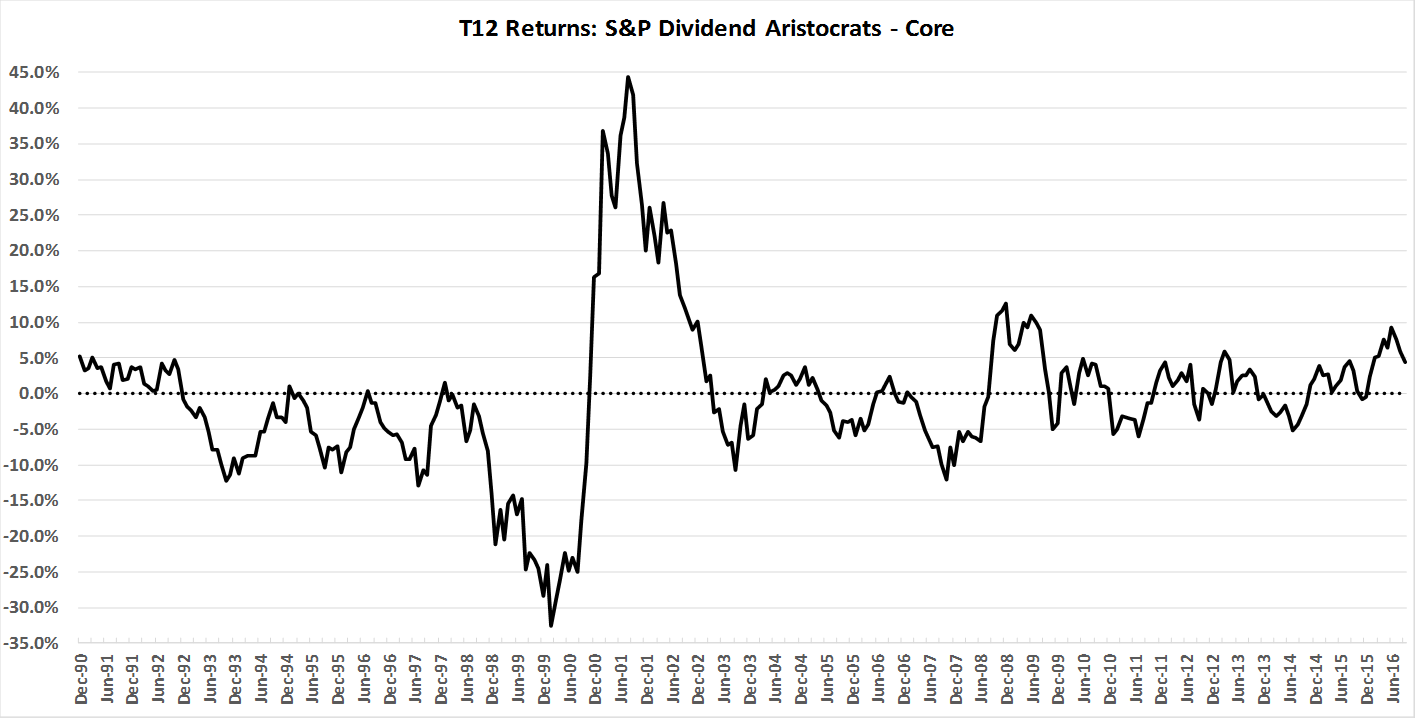

The purpose of Charts 1-6 is to illustrate the magnitude and duration of the relative-performance swings between each factor and the overall market. One of the most important things to understand about smart beta, as with any investment approach, is that it will experience periods of outperformance as well as underperformance. No factor or style works all the time and it’s critical for investors to have a sense of the cyclicality behind each strategy.

A common theme running through the charts is the incredible spreads that appeared during the Tech bubble and collapse of 1998-2001. This extreme period in market history has tainted every long-term data stream, and its impact on factor returns is multiples greater than any other period. This takes us back to the criteria of persistence; a factor that only works in extreme markets is not very useful. We want to see consistency across time and a generally positive bias in the factor before we commit real money going forward.

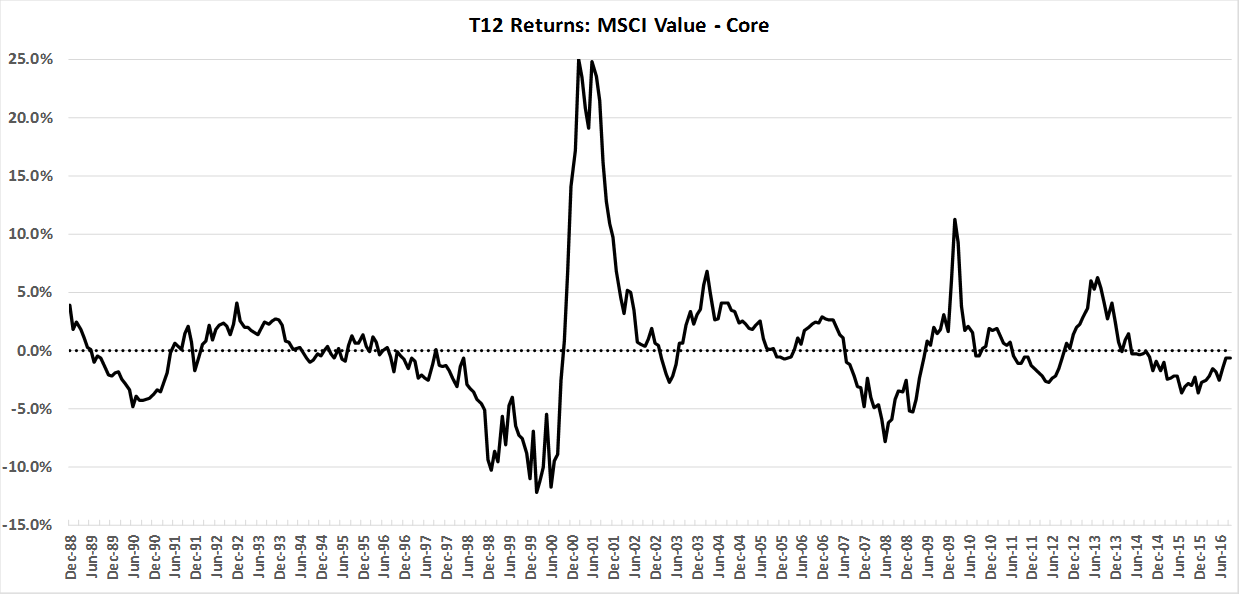

Chart 1

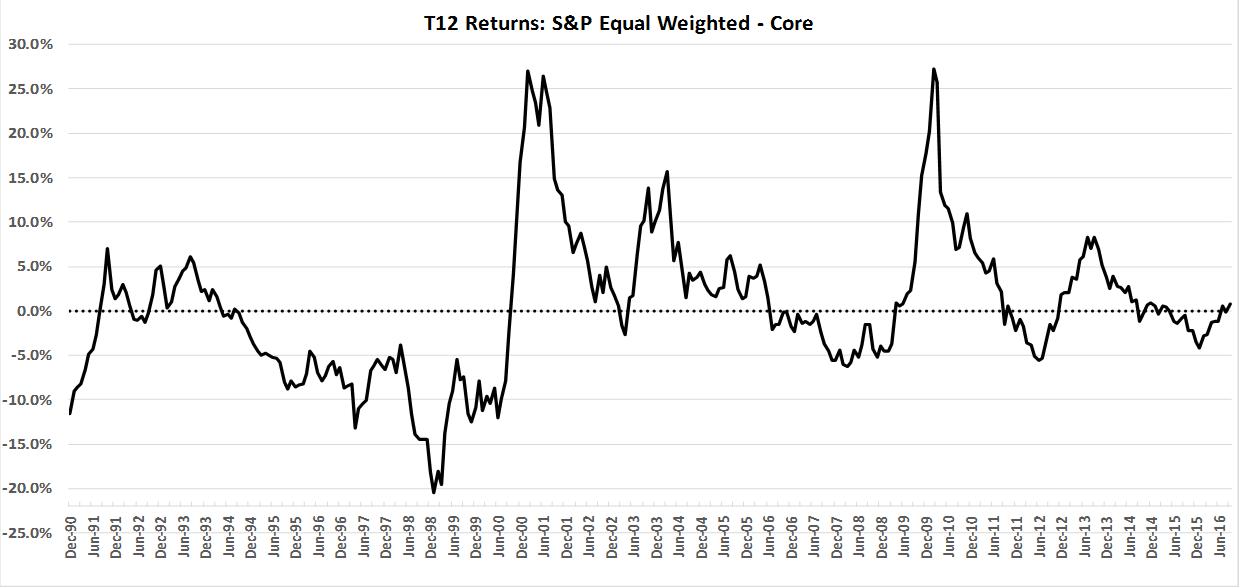

Chart 2

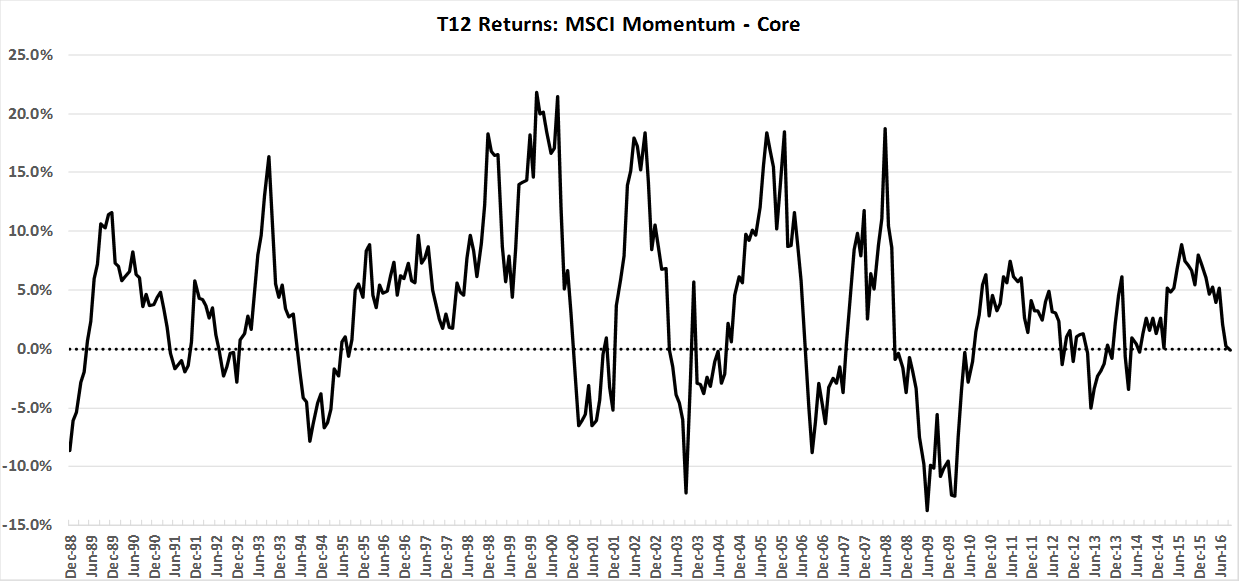

Chart 3

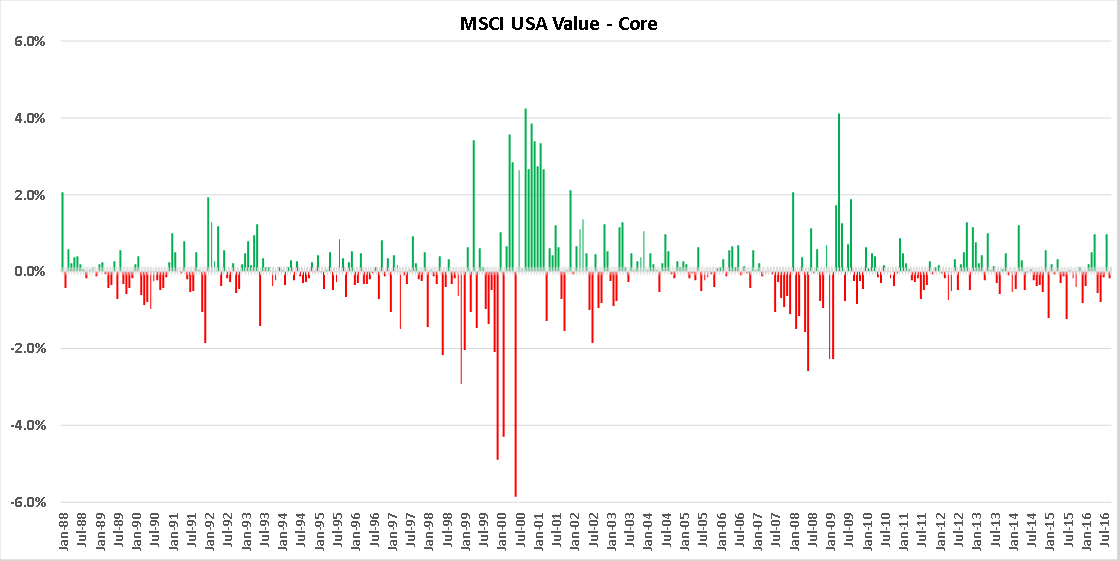

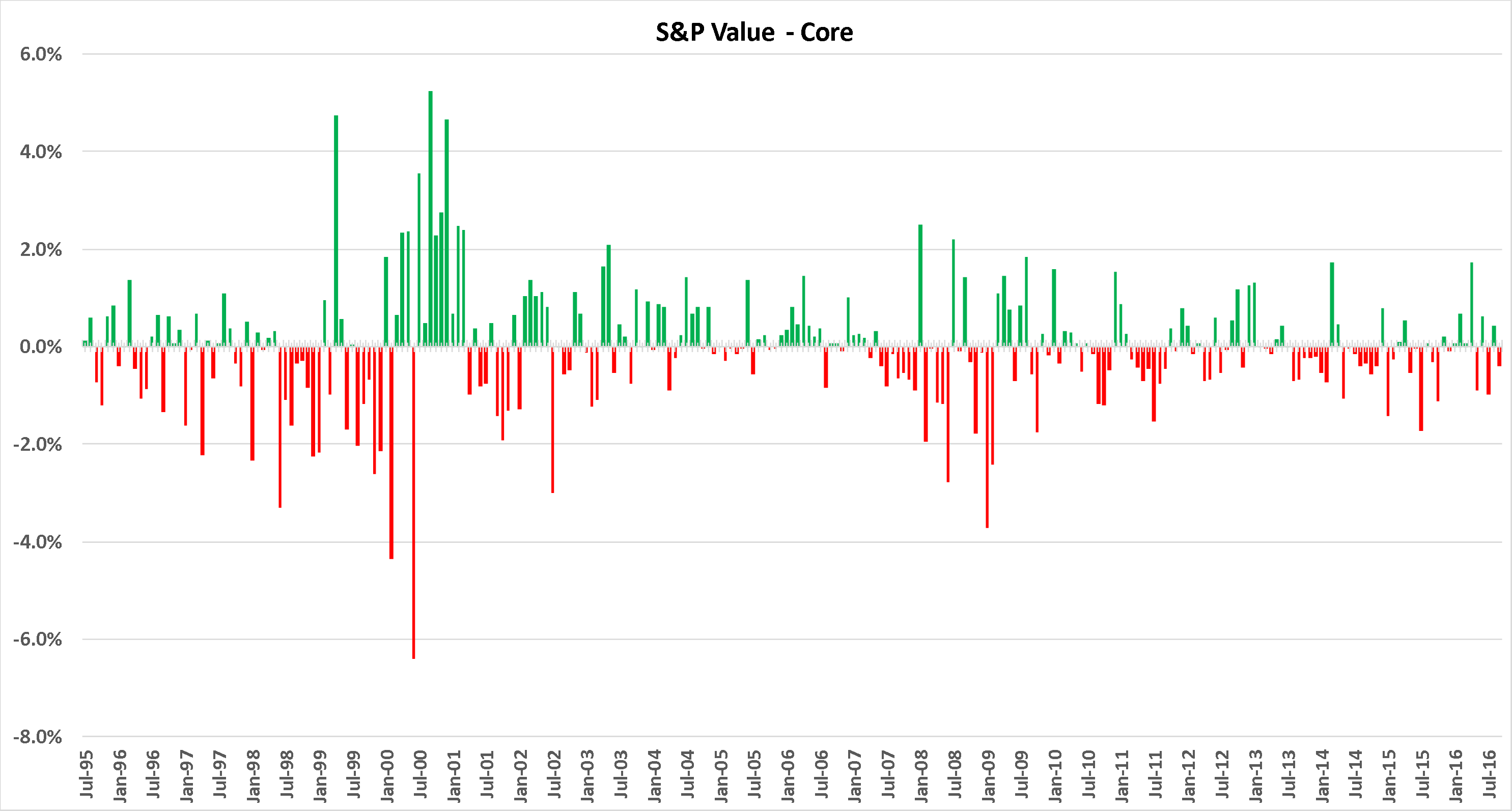

Value: MSCI defines Value based on a combination of Price/Earnings, Price/Book, and Yield. Chart 1 shows that lower valuation stocks tend to do poorly in a speculative bull market, such as 1999 and 2007, but come roaring back as the bubble deflates and sensibility returns to stock prices. The last few years have not been kind to Value, and it is the only anomaly currently on a multi-year losing streak.

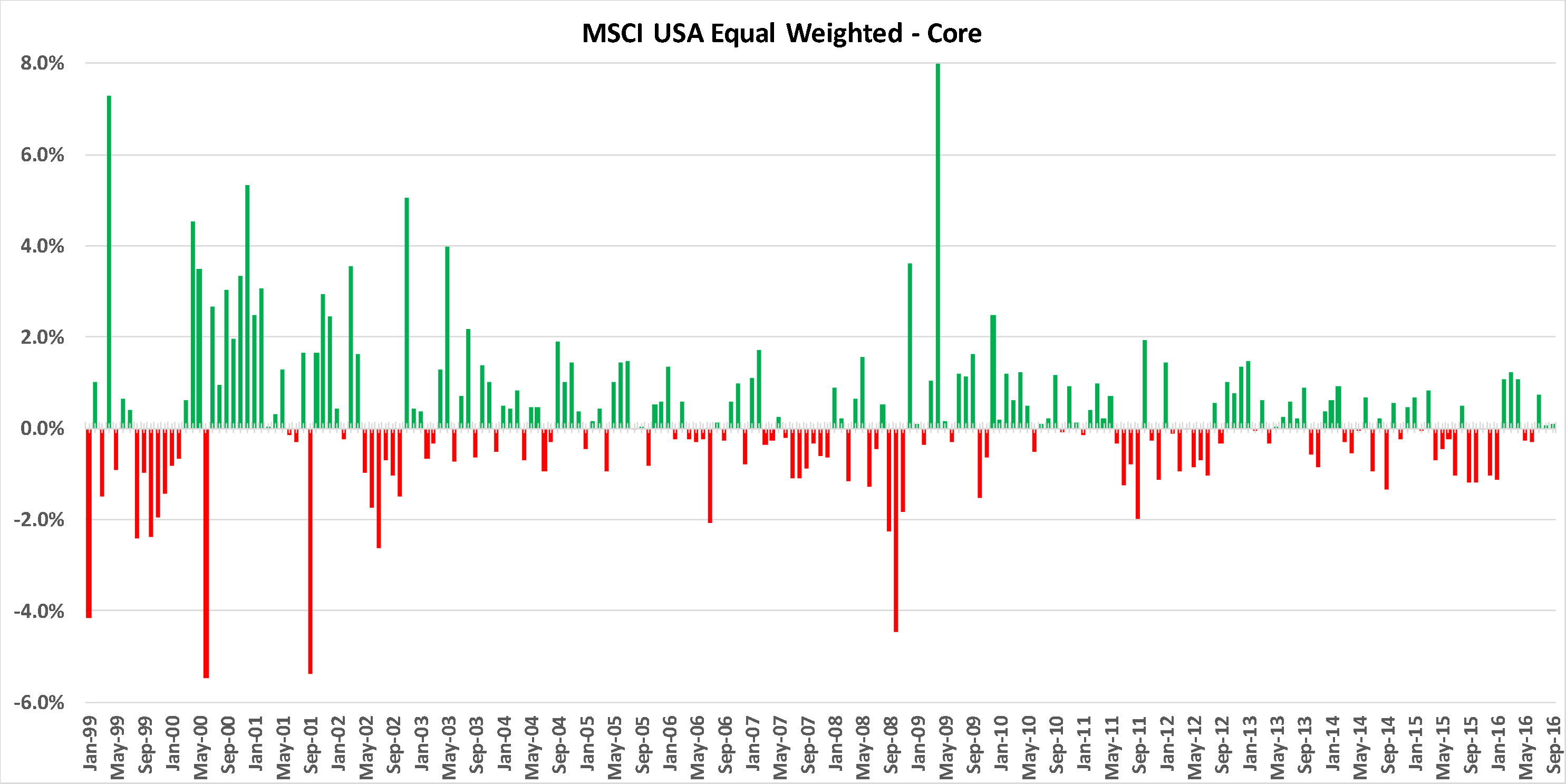

Size: Even though the constituents of equal-weighted and cap-weighted indexes are exactly the same, the importance of smaller companies is highlighted in the equal-weighting scheme. Equal weighting also has a counter-cyclical bias as seen in Chart 2, lagging in speculative up-markets driven by pricey mega caps, and winning as booms unwind.

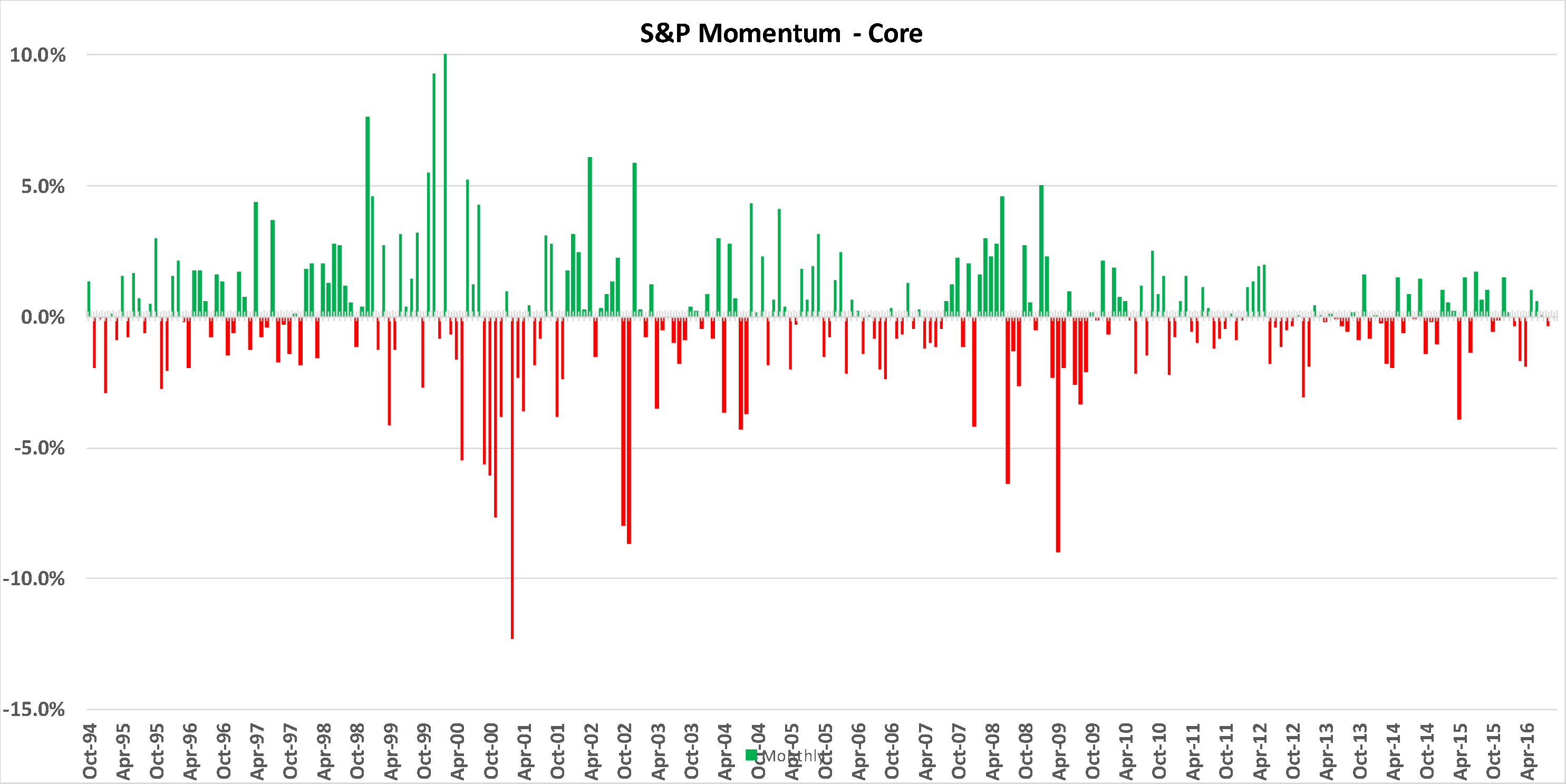

Momentum: Price momentum in Chart 3 is generally calculated as trailing twelve-month return excluding the most recent month, with higher returns being favored over laggards. As simplistic as it sounds to “buy recent winners,” momentum has one of the best hit rates of any return anomaly. Momentum most often falls short when the market reverses direction, leaving the strategy exposed to yesterday’s winners while the market has changed course.

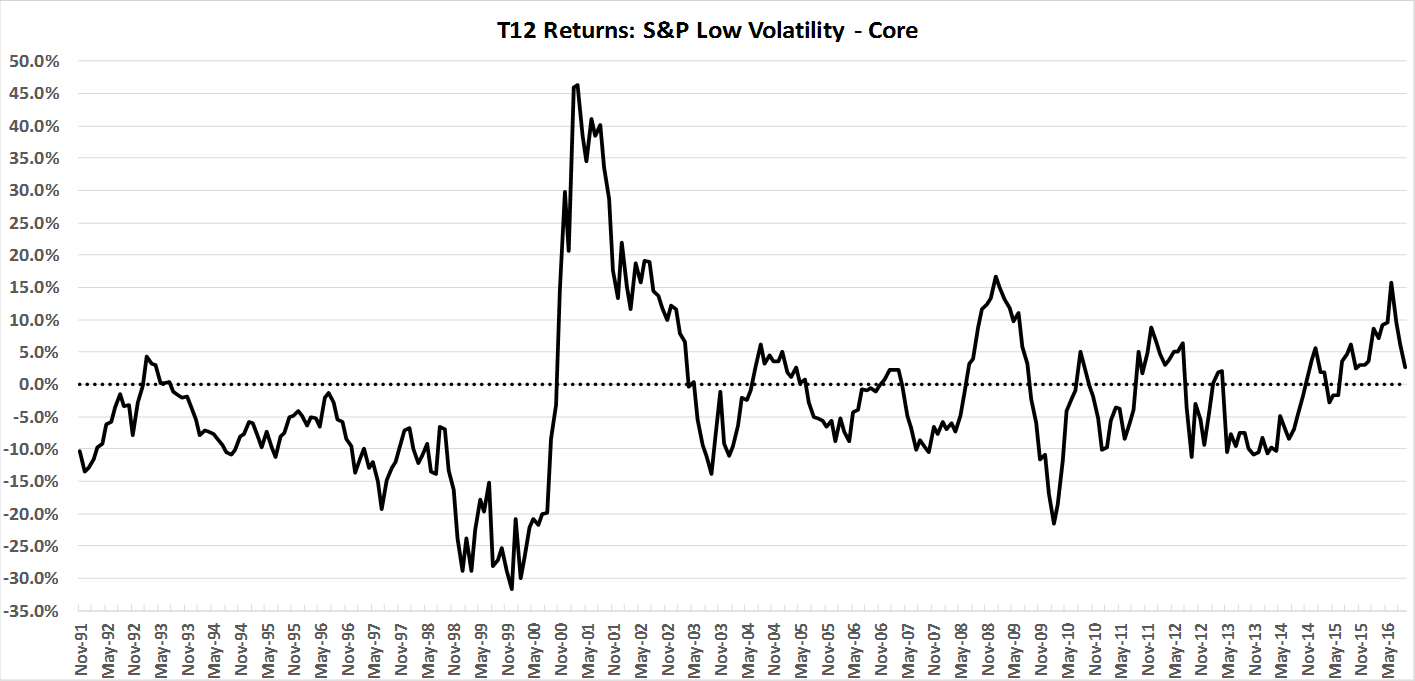

Chart 4

Chart 5

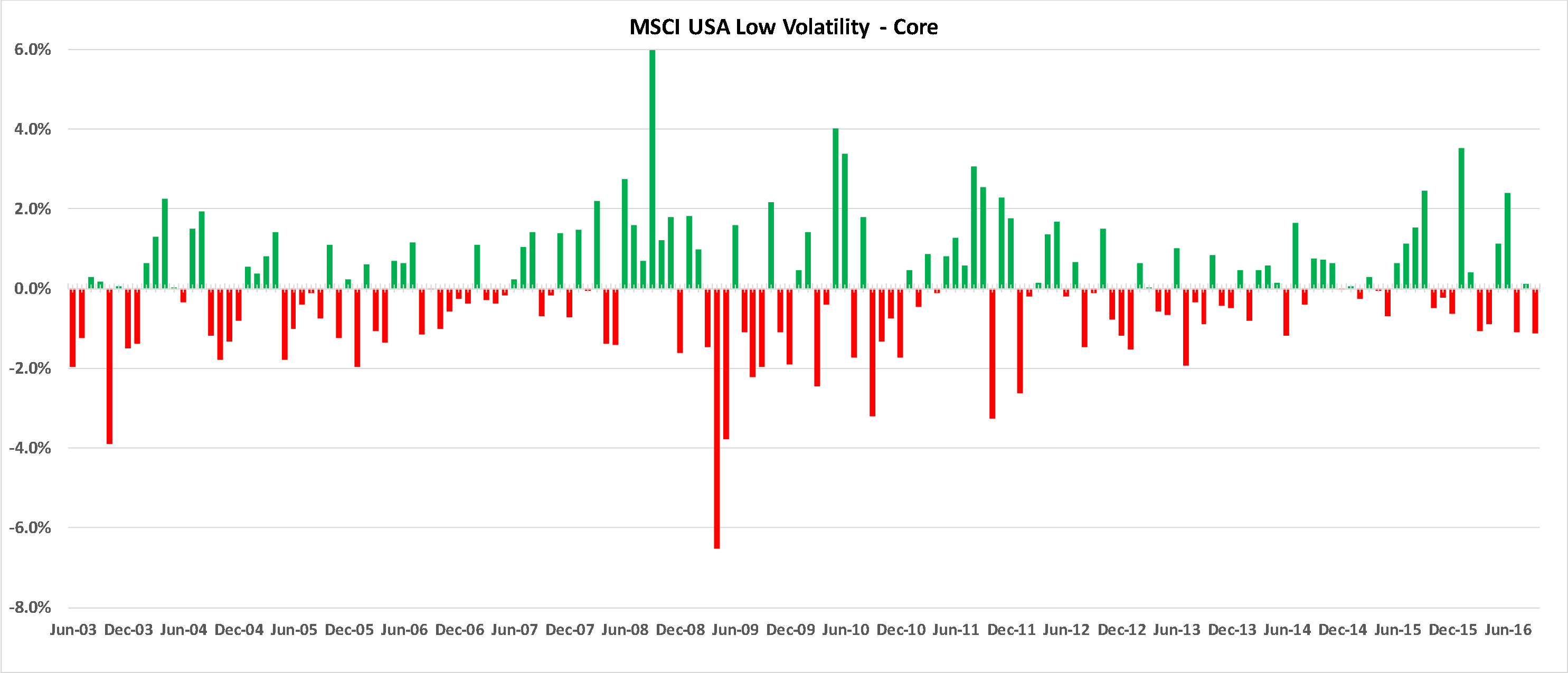

Chart 6

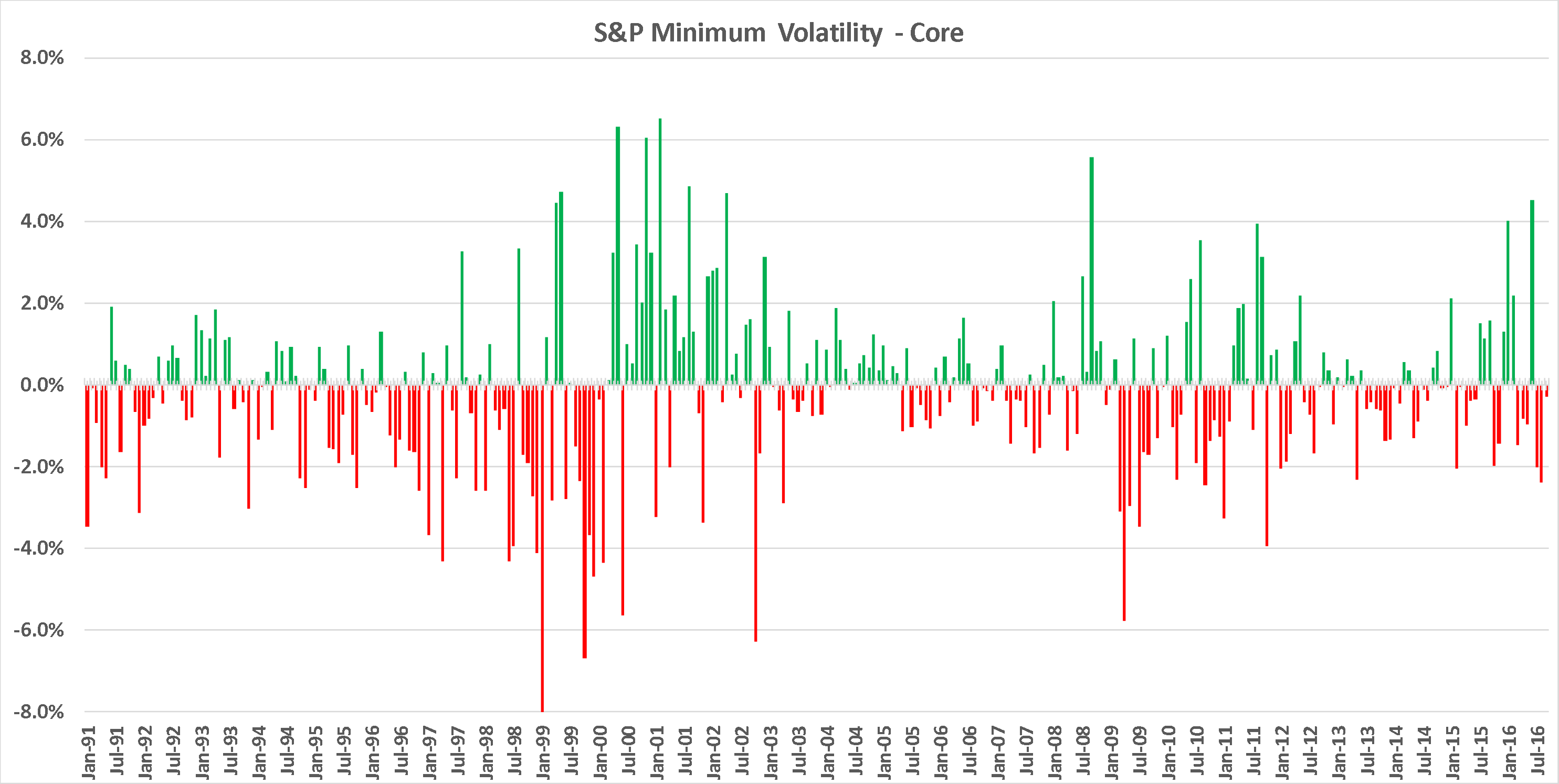

Volatility: “Low Volatility” (Chart 4) describes a portfolio made up of stocks that, individually, have low price volatility. “Minimum Volatility” strategies use correlations to select the portfolio that has the lowest overall volatility, even though not every component company is Low-Vol on its own. This is an “upside-down” factor in that we would intuitively expect investors to demand higher returns to hold high volatility stocks, but in fact it is low volatility that delivers an excess return. This has been the most popular and most successful strategy of late, as investors are worried about the market’s high valuation but are reluctant to move into low-yielding bonds. A happy medium is “safer” Low-Vol stocks that will hopefully provide some upside along with protection if the market does head south.

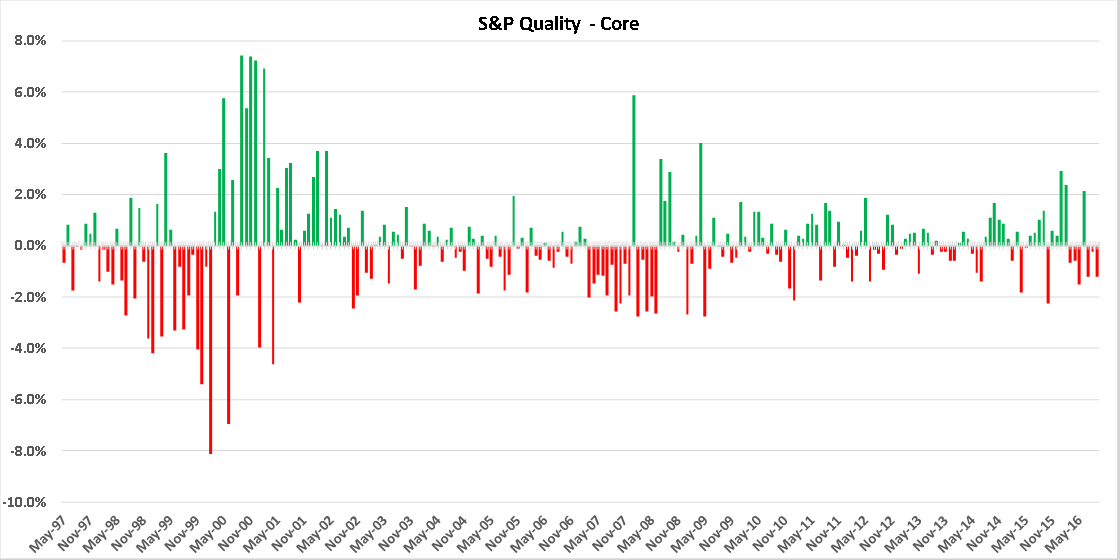

Quality: Defined in many ways, Quality typically includes profit margins, ROE, and leverage attributes. This is another “upside-down” factor in that it would seem investors should demand extra return to hold low-quality stocks, however, research shows that high-quality stocks generally outperform. Quality has been a reliable winner most of the last decade and has only recently begun to lag the core index (Chart 5).

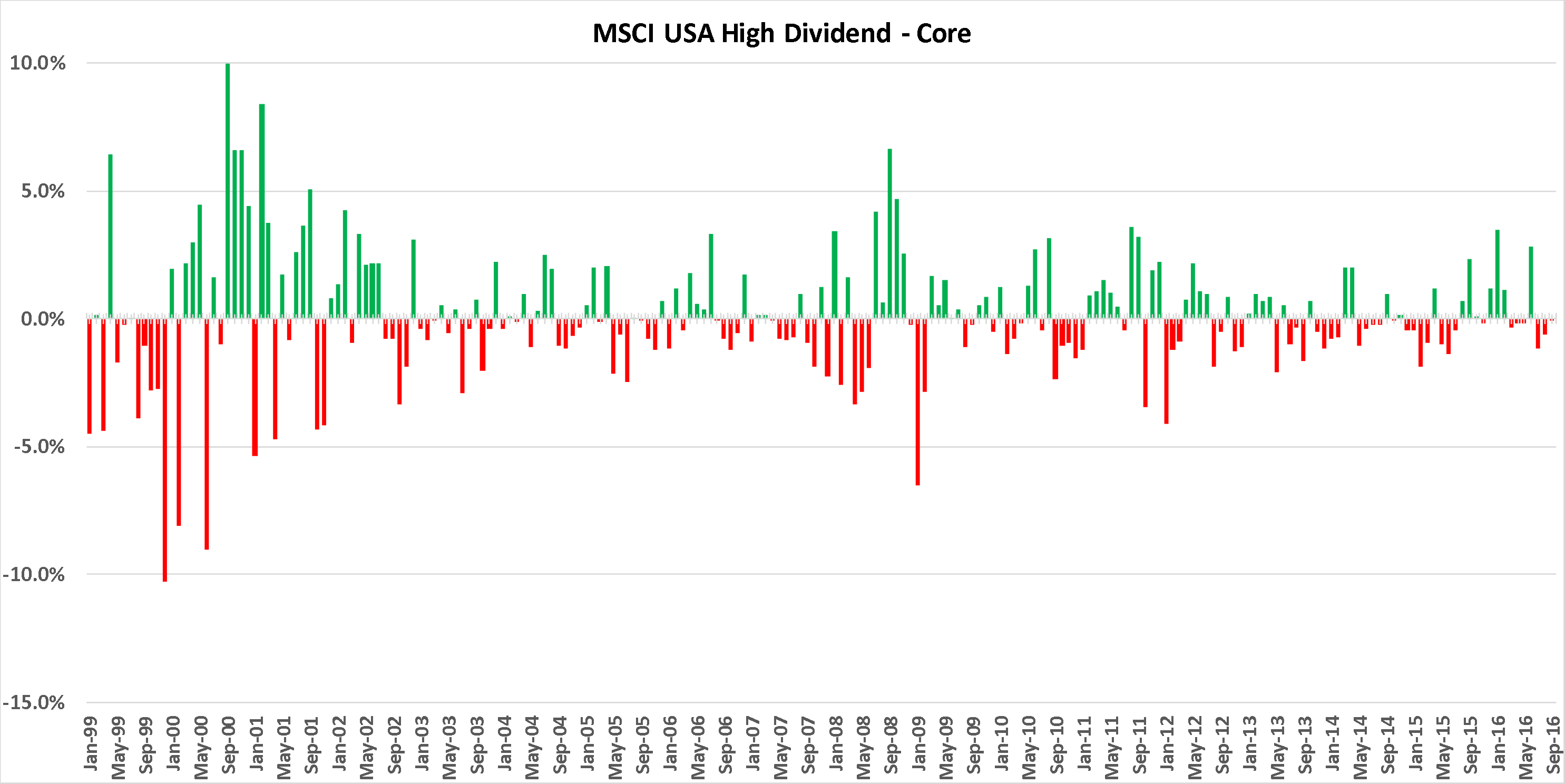

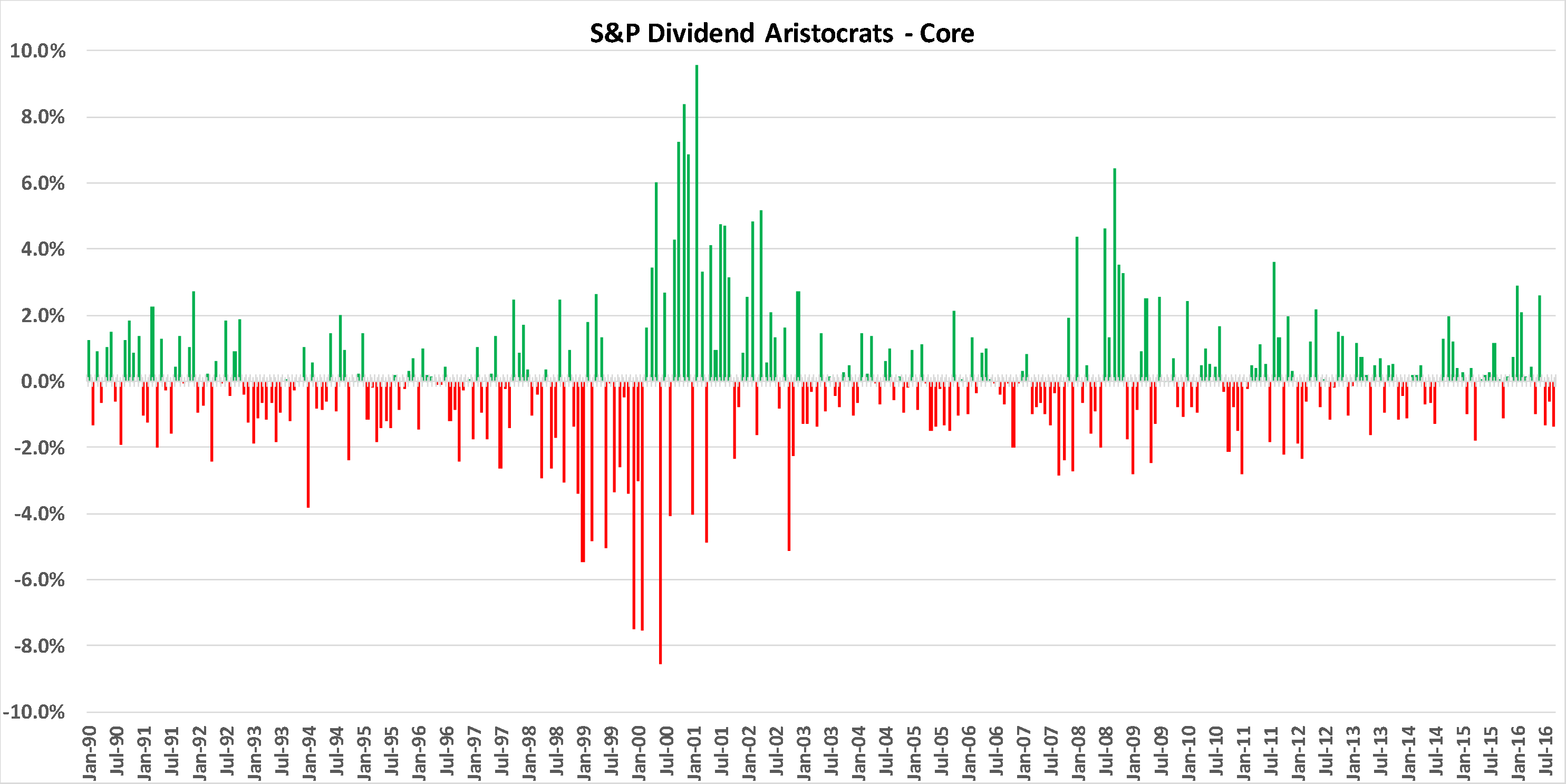

Dividends: Yield is yet a third “upside-down” factor in that dividends are generally seen as desirable, particularly by retail investors. However, research shows that high-yield stocks, not low yielders, provide an excess return over time. S&P’s dividend index focuses on dividend growth, while MSCI’s focuses on high current yield. Along with Low-Vol, dividend yield has recently attracted great interest from smart-beta investors looking for alternatives to low-yield bonds (Chart 6).

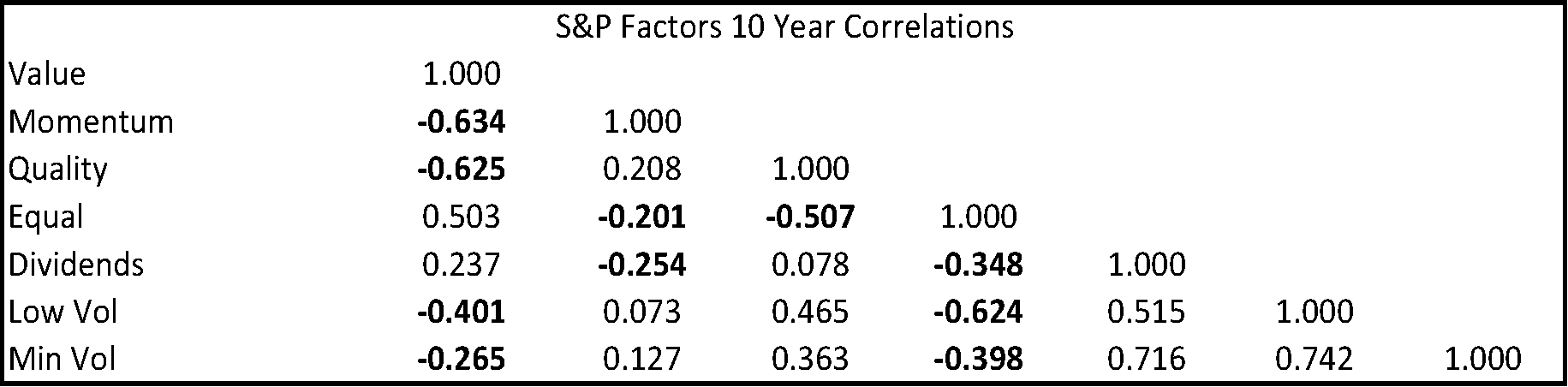

Building from the charts, we add Table 1, which shows the correlation of monthly return spreads across factors. One of the most attractive features of factor investing is that the factors generally have low or negative correlations with one another, increasing the value of diversification and greatly improving the risk-adjusted return profile of a multi-factor portfolio.

These generic factors are frequently similar to those incorporated in the proprietary models run at most quant firms. The main difference between firms such as The Leuthold Group and smart-beta funds is that traditional firms design, test, and build proprietary models that are considered confidential trade secrets. Smart-beta funds, on the other hand, are “open source” in that they rely on factors previously identified by academic research. These factors are available to anybody willing to study the literature on investment anomalies.

Simple To Explain, Difficult To Execute

Table 1

It all sounds so easy: identify a factor that has provided historical excess returns, design a simple quantitative metric to define the factor, build a portfolio full of stocks that have positive exposures to that factor, and wait for the returns to roll in. In theory, yes, but there is many a slip ‘twixt cup and lip. Our deep dive into factor investing, along with our decades of proprietary quant experience, help us to identify the subtleties and analytical challenges of factor investing that can make or break an investor’s success. We outline some of these difficulties in this concluding section, with the tease that we are actively researching each aspect and will pass along our findings in coming months.

Challenge #1: Defining the factor. Factors are defined differently by academic researchers and index providers. Which definition is the best? Which definition is most robust? Which definition is most likely to deliver the factor’s excess return going forward?

Challenge #2: Is diversification a good idea? If factors have low or negative correlation, is a basket of factors more attractive than a single factor? If so, how should that basket be designed and weighted? Should a stock be selected based on a high exposure to one of the factors, or does it need to reflect all the factors? Will one factor offset another, washing out the value of both?

Challenge #3: Factor returns are clearly cyclical. Is there a pattern? How extreme and long lasting are the cycles? Does factor success depend on a certain set of market conditions?

Challenge #4: If returns are cyclical, can they be timed? Since returns are cyclical, does tactical allocation work by selectively over and under underweighting factors? How should the tactical signal be constructed? This is the cutting edge of today’s smart-beta research and we look forward to adding our views to the discussion.

Challenge #5: Do fundamentals matter? Can a popular factor become overpriced and hence less likely to work in the future? Can an unpopular factor become more attractive because it is neglected and undervalued? Aside from the Value factor, do other factors outperform irrespective of their initial valuations?

Challenge #6: Long-Short. Academic research typically relies on building portfolios that are long stocks with high factor exposures, and short stocks that have low factor exposures. Most smart-beta funds use only the long side of the factor. How does the long-only versus long-short distinction impact the usefulness of a factor? Can factors be successful in a long-only portfolio, or does long-only cause a factor to lose its oomph?

The topic of factor-based investing, and the quantitative analysis of return drivers in general, is right in our wheelhouse. Greg Swenson has been producing factor-return analysis in the Green Book’s “Quantitative Strategies” section for some time now, and we will be augmenting that with a deeper look at returns, portfolio composition, and factor fundamentals as we move forward.

The success or failure of proprietary, quantitative disciplines and academic “open source” factor investing depends on properly analyzing and evaluating the design challenges we have identified. As a firm that employs quantitative processes, we are delighted to see investors becoming more confident in and supportive of this management style. We are eager to bring our perspectives and analytical skills to the world of factor investing and the smart-beta phenomenon. We hope to enlighten clients and to improve our own disciplines and models, always with the goal of developing original and profitable insights.

Monthly Returns of Each Factor: