It's not unusual for a new year to bring changes. But 2017 may be particularly noteworthy. Topping the list is a new U.S. president and Republican-controlled Congress, bringing the prospect of a new direction for many policies, regulations and legislative priorities. Elections and leadership changes also are on the calendar in several major countries, including France, Germany and China. What may not change next year are the geopolitical tensions that continue to pressure several regions around the globe.

Many investors may be unsettled by the prospect that change will cause market volatility and general uncertainty. At Ivy, we believe it is important to stay focused on the fundamentals and merits of sectors, industries and companies when making investment decisions. Those fundamentals historically have tended to outweigh external factors such as government policies and regulations. While these can affect every business and investor, we think the innovation and skill of individual companies ultimately drives long-term success.

We’ve identified five themes in our outlook for investors in the coming year.

|

|

|

|

|

Leadership in key countries

The 2016 presidential election put Republican Donald Trump in the White House as the 45th president of the U.S. and gave his party control of both the Senate and House of Representatives.

Trump on Nov. 21 provided the initial details of his priorities as president by releasing plans for his first 100 days in office. He said he will seek to use executive orders to withdraw from negotiations on the Trans-Pacific Partnership (TPP) trade agreement; cancel environmental regulations related to energy production, including “shale energy and clean coal,” in order to generate jobs; reduce other business regulations; direct the Department of Defense and Joint Chiefs of Staff to create a plan to protect U.S. infrastructure from cyber and other forms of attack; investigate “abuses of visa programs that undercut the American worker”; and impose a five-year ban on executive officials becoming lobbyists after they leave the administration and a lifetime ban on executive officials lobbying on behalf of a foreign government.

While it was not discussed among his initial plans, Trump and Republican congressional leaders also have continued to promise that they will abolish the Affordable Care Act, or “Obamacare.” Trump has offered reassurance, however, that a replacement plan will keep key provisions such as ensuring health insurance coverage for existing conditions.

If enacted, all of these measures could have economic and market impact. While we believe there are short-term risks to the economy, in part from speculation that Trump’s policies could be potential obstacles to economic expansion, we do not anticipate a significant change to our long-term growth forecast.

Outside of the U.S., we think it will be important to watch developments in elections and leadership changes in several key countries, as all are likely to be factors in global economic and market activity.

The first round of the 2017 presidential election in France will be held in April, with a run-off election between the top two in early May if no candidate wins an outright majority. Incumbent president François Hollande of the Socialist Party announced on Dec. 1 that he will not run for re-election, raising further questions about the future leadership of this key European Union country. His party is scheduled to hold a primary election in January, although it is not clear now who the potential party candidates may be. Candidates from other parties include François Fillon of The Republicans and Marine Le Pen, leader of the National Front.

Chancellor Angela Merkel, the first female leader of Germany, will seek a fourth term in elections next year, which must take place between Aug. 23 and Oct. 22. Merkel will face opposition in part from the nationalist Alternative for Germany Party, which is represented in 10 state parliaments and has aggressively campaigned against her immigration decisions.

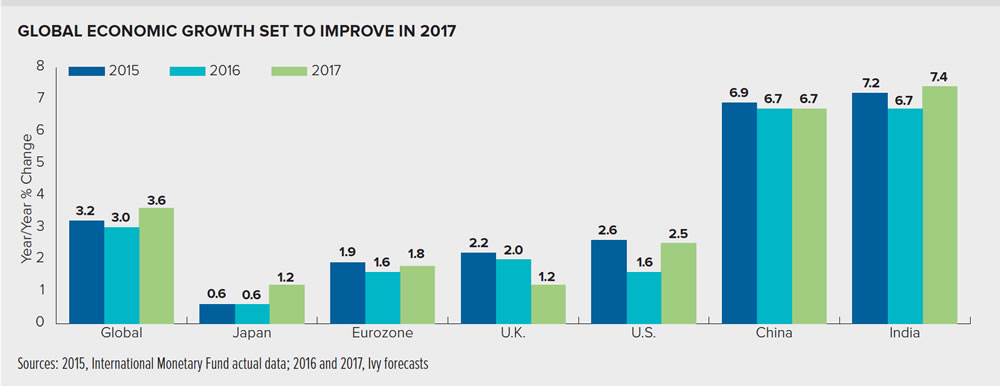

China – the second-largest economy in the world – will hold its 19th Communist Party National Congress during the second half of 2017. President Xi Jinping is expected to gain a second term as general secretary and remain in power. We think he is likely to continue policies that have included a widespread anti-corruption purge that has had effects within the party as well as on Chinese business and society. China boosted growth in 2016 through stimulus measures aimed at infrastructure and the property market, and again boosted demand for resources. We think China will continue stimulus programs in an attempt to keep economic growth at a similar level in 2017.

U.S. growth accelerates

We now forecast U.S. gross domestic product (GDP) growth will average 2.5% in 2017, up from 2016’s forecast growth of 1.6%. Inflation in the U.S. is running at an annual rate of 1.6%, which is within the Fed’s target of 2% inflation.1 We think inflation is likely to increase to that level or slightly higher in 2017.

Consumer spending is a key component of the U.S. economy and its recovery since the global financial crisis. We think that situation will continue next year. Retail sales have increased 4.3% since October 2015,2 reflecting consumer optimism and slow, steady economic growth. Consumers showed increased confidence in the economy late in the year, as shown by indexes that have returned to levels not seen since the Great Recession.3 We think that sentiment is an indication consumers will continue to spend, especially now that the uncertainty of the presidential election has been resolved.

While jobs and job growth were major issues in the election campaign, the U.S. unemployment rate has fallen to 4.6%, the lowest in nine years. The latest unemployment rate also reflects a drop in the number of people in the workforce, however.4 Employment overall continued to trend higher late in the year in health care, professional and business services, and financial activities. Employment in other major industries – including mining, construction, manufacturing, wholesale trade, retail trade, transportation and warehousing, information, leisure and hospitality, and government – has been little changed.

The popularity with voters of Trump’s pro-growth agenda may reflect the difference between employment data and the potential for individual upward mobility in a job or lifestyle. Phil Sanders, CEO of Waddell & Reed Financial, Inc. and CIO of Ivy Investment Management Co., notes that the U.S. economy is growing and overall wealth continues to improve, but "there isn’t a lot of dynamic activity in the economy." That may add impetus to policies to create or recover jobs in the U.S. “Austerity is not a recipe for growth," Sanders says. "Spending creates jobs, corporate earnings per share and ultimately tax revenues."

We believe a focus on infrastructure spending from the Trump administration could slightly boost that economic growth. He has highlighted his support for major improvements in bridges, highways and the nation’s energy infrastructure and electricity grid, and even promised upgrades in railroads, tunnels, airports, schools, hospitals, ports and waterways. While we think infrastructure spending in general is likely to have support in Congress, the extent still is unclear.

During his presidential campaign, Trump also promised a major overhaul of the tax code. "Corporate tax reform would be very positive for business sentiment," says Ivy Global Economist Derek Hamilton. "Trump has called for cutting individual taxes, he has supported infrastructure spending – all of these things could be positive for growth in the second half of 2017 and in 2018."

The impact of trade on the U.S. economy has come into question because of Trump’s comments during the presidential campaign and since his election. Although he has announced a planned withdrawal from the TPP, there have been few other details about trade policy. Hamilton says a token increase in tariffs on a specific item from a country such as Mexico or China or minor revisions to the North American Free Trade Agreement would not create worries about trade policy. "However, if we see across-the-board tariffs on many goods from many countries, that would be negative for growth in the U.S. and other countries as well," he says.

The Trump administration’s approach to trade could be important to emerging markets, where restrictive or protectionist trade policies would have a major impact. "Emerging markets are heavily geared toward trade," Hamilton says. If changes are modest and don’t impede growth, emerging market economies may continue to perform well, he says. Longer term, we think global growth overall and individual company performance will continue to be the key drivers for the emerging economies.

Return of rising rates

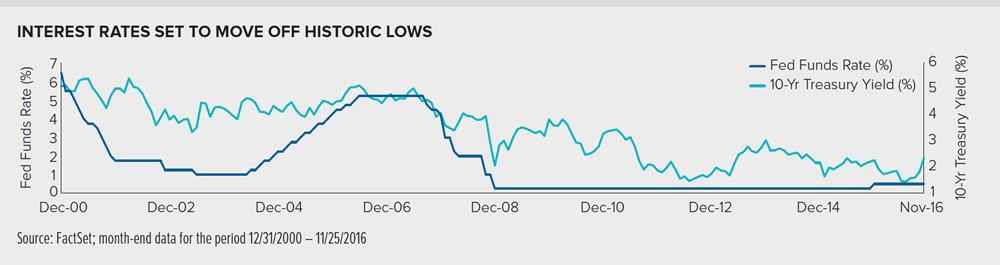

While the U.S. Federal Reserve (Fed) has indicated it will increase interest rates at its mid-December meeting, probably by 0.25 percentage point, we think further hikes are likely in 2017. Fed Chair Janet Yellen sent a strong signal of a December rate hike during testimony to Congress’ Joint Economic Committee on Nov. 17 when she said the economy is making solid progress and an increase could come "relatively soon."

Trump made several critical comments about current Fed policy and Yellen during his campaign. He has not called for her resignation, but has indicated he will not reappoint her when her term expires in early 2018. There also are two vacancies on the Fed’s Board of Governors and there could be other openings timed with, or leading up to, the expiration of Yellen’s term. We anticipate changes to Fed leadership in the future and think a more "hawkish" approach and higher interest rates are likely as a result.

The short end of the U.S. Treasury yield curve (five years and fewer) may be less volatile in the coming year because of the Fed’s commitment overall to low interest rates, says Mark Beischel, Ivy’s Global Director of Fixed Income. However, longer term Treasury rates may be more volatile in reaction to market uncertainty about fiscal and monetary policies, he says, especially given the change in the U.S. administration. He notes that the U.S. budget deficit is on the rise and the supply of U.S. Treasury securities will increase with it, but largely through Treasury bills in 2017.

Beischel also says high-yield credit is somewhat insulated from any concerns with the new administration and trade. "High-yield companies tend to go as the U.S. economy goes," he says. "Any concerns in the credit market at this point relate mainly to three areas: the Fed becoming more aggressive, with more interest rate hikes than are priced into the market; a substantial rise in Treasury yields; and political missteps that would have economic ramifications."

Beischel says he thinks central banks outside the U.S. will continue their current easy monetary policies. The recent strength in the U.S. dollar will allow them to pursue more aggressive actions in the near future, he says.

Oil finds supply/demand balance

The organization of Petroleum Exporting Countries (OPEC) agreed in late November to reduce production by 1.2 million barrels per day (bpd) to a total of 32.5 million, marking the first production cut in eight years. David Ginther, co-portfolio manager on Ivy Energy Fund, says the agreement is an important demonstration that OPEC countries again may be willing to act together when it comes to the oil market. The quota reduction itself is a meaningful reduction in supply, he says.

Ginther notes that the decision effectively puts a floor under crude oil prices at about $50 per barrel. He believes the oil market has reached a supply/demand balance and OPEC’s move will allow current high inventory levels to fall more quickly. Looking ahead, Ginther says, the price of crude oil could reach the mid to high $60s in 2017.

Global oil demand has continued to grow and may increase by 1.2 million bpd in 2017 on top of the current total of 95 million bpd, with the increase driven mostly by emerging markets. Ginther says energy companies will need to make new investments in order to meet supply requirements in the coming years, and higher oil prices are needed to attract any new investment.

He says oil producers need to get projects moving again to meet supply requirements as soon as 2018-2020. Capital spending was cut by 50% in the last two years and hundreds of thousands of workers have been laid off. Discoveries of new oil reserves totaled 2.8 billion barrels worldwide in 2015, the lowest annual volume since 1954.5 Ginther adds that it will require higher prices and time for the industry to get spending going and re-start or initiate new projects, and bring back jobs. These factors mean output will be slow to recover versus the stable demand growth worldwide, he says.

Sectors to watch in ’17

We think the financials, health care and defense sectors will remain in focus in 2017. In our view, a Fed rate hike will provide a positive scenario for the financials sector. Financials tend to benefit from rising rates because the interest margin expands, which in turn can create more profit, and improving economic activity typically points to more loan demand.

- Financials: A less-intense regulatory environment may provide an added benefit to the financial sector. For example, new Department of Labor regulations related to fiduciary standards for financial advisors — set to be implemented in April 2017 — may be delayed, revised or dropped if not enacted before President Barack Obama leaves office. The Trump administration also could repeal the Dodd-Frank Wall Street Reform and Consumer Protection Act, which put in place the most significant changes to financial regulation since the Great Depression. The Act affects all federal financial regulatory agencies and almost every part of the U.S. financial services industry.

-

Health care: Health care was hit this year by rhetoric about drug pricing and increased regulation. The Trump election victory prompted a rally in pharmaceutical sector stocks, since that industry was an area of scrutiny for Democrats and had absorbed pricing attacks. Similar factors have applied to biotechnology companies. But we think pharmaceutical companies can adapt to more scrutiny on their pricing.

Trump’s call to repeal Obamacare could pressure health care services stocks, such as hospitals and other providers, which have benefited from the law. Sanders suggests these stocks are likely to be volatile since policy or legislative changes – and any fundamental changes to the companies themselves – will take time to develop.

From an economic perspective, a key question is what any change in, or replacement of, Obamacare would mean to health care premiums. “The increases in premiums in the last couple of years have been a fairly significant drag on consumer purchasing power,” Hamilton says. Any changes that cause more modest increases in annual premiums could be positive for consumers and the economy, he says. - Defense We think defense stocks may perform well in the future because we believe Trump will take a hard stance on national security. We believe it is likely the defense budget will expand, which bodes well for companies dependent on governmentfunded defense contracts. That said, any new demand could prompt pressure for lower contract prices.

Other areas to watch

1Source: Consumer Price Index, U.S. Bureau of Labor Statistics, October 2016

2Source: Retail Sales report, U.S. Census Bureau, October 2016

3Source: Consumer Confidence Index, The Conference Board, November 2016

4Source: Employment Report, U.S. Bureau of Labor Statistics, December 2016

5Source: Financial Times, “Oil discoveries slump to 60-year low,” May 8, 2016

© Ivy Investment Management