KEY TAKEAWAYS

- Stocks and the 10-year Treasury yield have historically moved in the same direction when the yield has been below 5% as it is currently.

- Stocks have mostly interpreted rising interest rates as a signal of better economic growth, rather than harmful inflation, and have historically risen during periods of rising rates.

- We believe the bull market in stocks can coexist with the bear market in bonds.

Surging bond yields have not spooked stock market investors. The latest sharp move higher in bond yields has caused stock market investors to ask the question, At what point do higher interest rates potentially begin to hurt stock prices? It is logical to think higher interest rates will eventually slow the economy. Borrowing costs rise and higher inflation—which has accompanied higher interest rates in the past—erodes purchasing power. These are all reasonable points to make when evaluating the relationship between stocks and bond yields. Here we look at this relationship and make the case that, given the still low rate environment, rising interest rates do not put the aging bull market at risk.

IS 5% A MAGIC NUMBER?

The 10-year Treasury yield has risen about 110 basis points (1.10%) over the past five months to 2.46%. That move in rates has certainly not spooked the stock market, as the S&P 500 is up 130 points, or 6.1%, during that period and 4.2% during the fourth quarter alone.

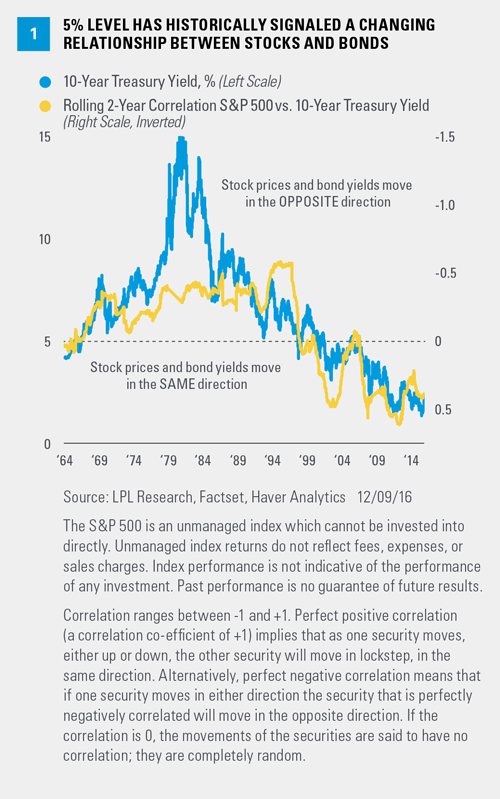

One of the reasons stocks have done well as bond yields rose is that the absolute level of yields is still low. We see in Figure 1 that, at a 10-year yield of 5%, the correlation between stocks and bond yields has historically changed. When the 10-year yield has been above 5%, as it was throughout the 1970s and 1980s, stocks tended to move in the opposite direction of bond yields (so when rates rose, stocks fell, i.e., negative correlation). Conversely, over much of the past two decades, the yield on the 10-year Treasury has been below 5%, and stocks and bond yields have exhibited positive correlation (stocks have tended to rise as bond yields have risen).

This relationship suggests that, with the 10-year yield currently near 2.5% and well below the 5% mark, rising bond yields may not disrupt the stock market’s ascent. So, while we would certainly not consider 5% a magic number, we do think yields have room to move before they become worrisome for the stock market.

We believe the change in the stock-bond yield relationship reflects the different growth and inflation signals reflected by the high and low levels of interest rates. Starting from low yield levels, rising interest rates tend to reflect rising economic growth expectations and ebbing deflation fears. And bond market losses may make investors sell bonds to buy stocks.

Conversely, at high interest rate levels, economic growth has been accompanied by high inflation, which can negatively impact economic growth and erode the present value of future earnings, a negative for stock prices such as was observed in the late 1970s.

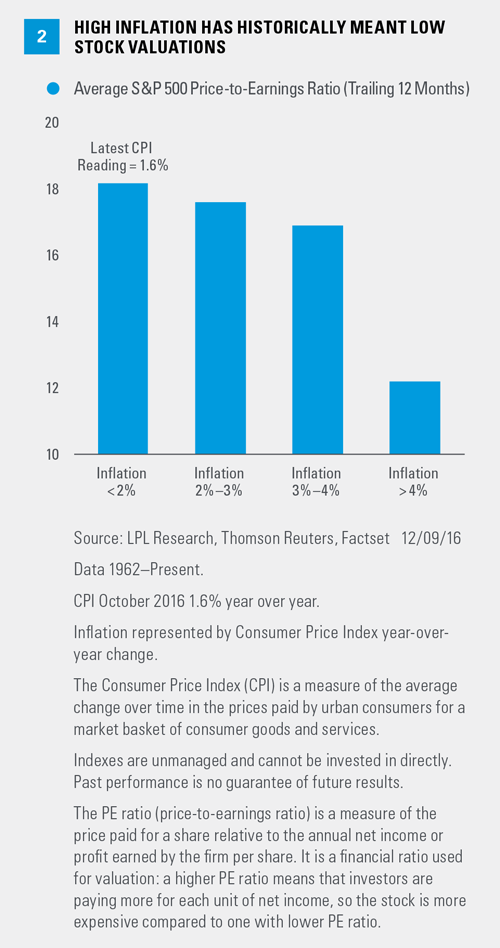

The negative impact of high inflation on stocks is evident in Figure 2, which shows the stock valuations have historically been lower at high levels of inflation, as measured by annual changes in the consumer price index (CPI). The latest reading on the CPI (October 2016) is below 2% (1.6% year over year), which has corresponded to average price-to-earnings (PE) ratio of just over 18, which happens to be where the S&P 500 PE is currently.

Similarly, high interest rate levels (above a 6% 10-year Treasury yield) have historically corresponded to lower stock valuations. Based on data back to 1962, above 6% the S&P 500 PE has averaged 13.7, compared with an average PE of 18 at 10-year Treasury yields below 6%. High interest rates can also put upward pressure on the U.S. dollar and, at least temporarily, negatively impact export growth and overseas corporate profits.

A LOOK AT HISTORY

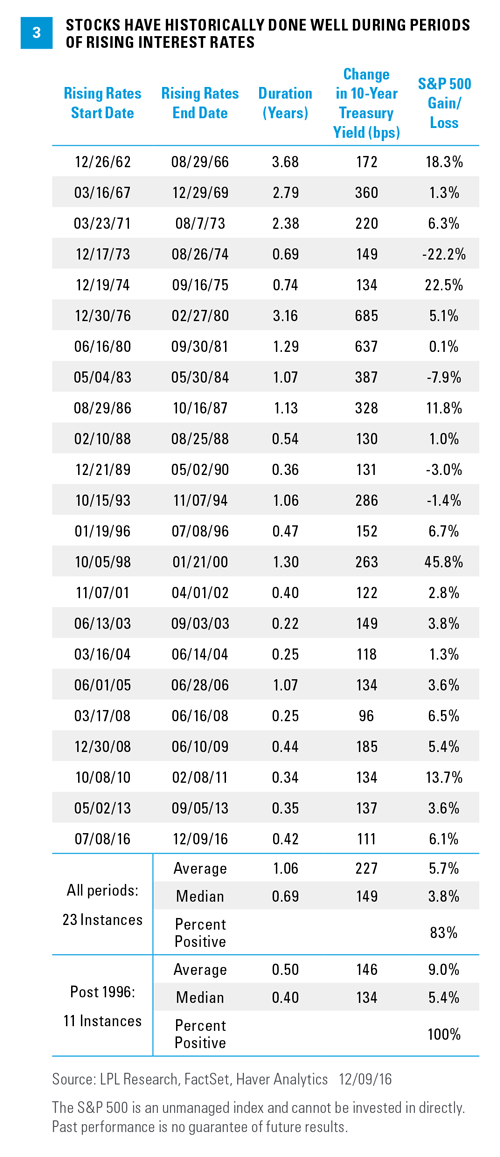

It is also instructive to look back at historical periods of rising interest rates to see how stocks reacted. Figure 3 shows all of the rising interest rate periods over the past 55 years (minimum of 100 basis point rise in the 10-year yield). The results offer generally good news, as stocks have mostly interpreted rising interest rates as a signal of better economic growth rather than harmful inflation. During the 23 periods analyzed, the average gain in the S&P 500, excluding dividends, has been 5.7% (median 3.8%). The average duration of the periods is 1.06 years and stocks rose in 83% of the periods.

Some of the circumstances surrounding markets during the rising rate periods when stocks fell most allow us to differentiate those periods from the current environment:

· Late 1973-early 1974.The U.S. was in the midst of an oil crisis from the Arab oil embargo and inflation fears were rampant. The S&P 500 fell 22% as interest rates rose from December 1973 through August 1974.

· Late 1983-early 1984. Soviet Union’s military buildup, along with terrorist bombings in Lebanon, and military conflicts in Libya and elsewhere, put geopolitical risk at the forefront. Inflation picked up and oil prices rose, prompting the Fed to raise rates aggressively. Stocks fell 7.9% from May 1983 through May 1984.

· December 1989-May 1990. The U.S. economy was on the verge of a recession, which began later that year in July of 1990. Inflation, based on the CPI, had steadily marched higher, averaging 4.1% in 1988, 4.8% in 1989, and 5.6% in 1990. Stocks fell 3% from December 1989 through May 1990.

· October 1993-November 1994. The Fed raised interest rates aggressively in 1994 after rates had been taken down substantially to combat the Savings and Loan crisis and the 1990-1991 recession. Stocks dipped 1.4% from October 1993 through November 1994.

Recent history has been better in general, as stocks have risen in all 11 rising rate periods since 1996, with an average gain of 9% (median 5.4%). These periods have been shorter in duration (average half a year) and seen slightly smaller rate moves, a reflection of the low inflation and low interest rate environment over the past 20 years.

While this analysis only goes back to the early 1960s, and going further back risks erroneous comparisons, the 1950s provide another example of stocks performing well in a rising interest rate environment. Bottom line, we believe the bull market in stocks can coexist with the bear market in bonds and we interpret the move in rates as an indication of improving economic growth prospects rather than of worrisome inflation.

CONCLUSION

The sharp move higher in bond yields has not spooked stock market investors. With the low level of interest rates and inflation, the market is interpreting higher interest rates as a signal of improving growth expectations. We think this is the right interpretation, while the stock market’s solid track record of performance in rising interest rate environments offers reassurance. Overall we do not expect higher interest rates to derail the ongoing bull market. Look for more from us on this topic in our Outlook 2017 publication due out on December 22, 2016.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

Government bonds and Treasury bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

All investing involves risk including loss of principal.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

© LPL Financial

Read more commentaries by LPL Financial