The Fed raises rates. Finally.

It’s been a long wait, but the U.S. Federal Reserve (Fed) finally raised interest rates by 25 basis points today, bringing the current rate to 0.5 – 0. 75%.

The market took a small step back today, with the S&P 500® falling by 0.5%, according to Bloomberg at 12:45 p.m.Pacific Standard Time. We believe the rate increase has been priced into the markets for some months now, due to a great deal of communication, stronger economic data, and a market-implied probability of a rate increase of more than 90%.

The surprise was that the Fed’s projections were upgraded to now show a forecasted pace of two to three rate hikes next year. In our view, however, the distribution of Fed forecasts indicates that Fed Chair Janet Yellen still likely favors a two-hike pace. And that’s important given her leadership role on the committee.

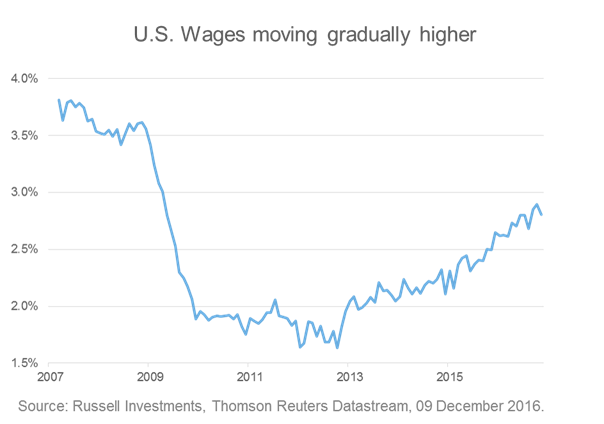

The last Fed interest rate increase happened in December of 2015. There were a number of market and economic setbacks in 2016 that caused Yellen to take a more cautious approach, including market volatility early in the year, sluggish Chinese growth, a weak U.S. employment report in May, and the surprise Brexit vote. But under the surface, the U.S. economy this year has been incredibly resilient. As of this writing, the U.S. unemployment rate hovers around 4.6%—the lowest rate since 20071. And positive inflationary pressures—particularly wage inflation (as shown in the figure below)—are continuing to build in the country.

The expected impact: Not much

We expect the rate increase to have very little lasting impact on equity markets and don’t foresee meaningful volatility from this announcement. Higher interest rates can be a positive catalyst for the financial sector to outperform its more defensive counterparts, including utilities and other low volatility stocks.

We believe even emerging markets (EM)—which can be more sensitive to U.S. Fed rate increases—will likely see little in the way of additional headwinds going forward. Conceptually, as U.S. interest rates rise, capital is often attracted away from the emerging economies, but we believe most of that damage to EM is behind us at this point, as noted in our 2017 Global Market Outlook. Bigger EM risk likely still lies ahead, depending on the continued pace of rate hikes in 2017 and beyond.

On the fixed income side of the scale, there is an outlier possibility this rate increase could further encourage selloffs in the bond market. But Russell Investments’ strategists believe that also registers as a low probability.

We are paying special attention to currency markets, which are typically very much impacted by yield moves. While there has been a lot of volatility in the U.S. dollar over the last few years, we expect to see it appreciate modestly throughout 2017. Still, we are keeping a watchful eye on the relationship between the Fed and other central banks around the world.

More Fed movement in 2017

Looking ahead, we still expect the Fed to raise rates twice more in 2017. When? It’s too soon to say. As the new year begins, it will be interesting to see if the Fed changes their communication style going forward.

Under Janet Yellen, the Fed has been much more transparent than it was under previous chairs, with its members regularly speaking publicly about their different views. While that approach has allowed for this rate increase to be priced into the market ahead of an announcement, that communicative style also seemed to create a significant amount of market noise earlier in 2016.

Under a Trump administration, what might happen when Yellen’s term ends in early 2018?

It’s too early to tell, but we’ll keep a close watch on who he nominates for the two currently vacant Fed governor positions.

Trump’s economic platform of tax cuts and infrastructure spending could provide a tailwind to the U.S. economy towards the end of 2017. The Fed will be in a “wait and see” mode around the size and specifics of the final fiscal package before altering course, but this increases the risk of a faster hiking process as we move into 2018.

See our 2017 Global Market Outlook – Annual Report for more information about what we expect next year.

1 Source: U.S. Bureau of Labor Statistics. December 9, 2016.

Disclosures:

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

Investing involves risk and principal loss is possible.

Forecasting is inherently uncertain and may be incorrect. It is not representative of a projection of the stock market, or of any specific investment.

Investments in non-U.S. markets can involve risks of currency fluctuation, political and economic instability, different accounting standards and foreign taxation.

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional.

The S&P 500, or the Standard & Poor's 500, is a stock market index based on the market capitalizations of 500 large companies having common stock listed on the NYSE or NASDAQ.

Russell Investments' ownership is composed of a majority stake held by funds managed by TA Associates with minority stakes held by funds managed by Reverence Capital Partners and Russell Investments' management.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

Copyright © Russell Investments 2016. All rights reserved.This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.

UNI – 10974