There is a normal dose of economic data this week, but we are entering a quiet, pre-holiday period. As the rally faltered a bit, the Dow 20K talk yielded to a discussion of what could go wrong. I expect this discussion to continue in the coming week, and perhaps the next one as well. The punditry will be asking:

What can derail the rally?

Last Week

In a reversal from the last month, most of the economic news was soft. There was little apparent market effect.

Theme Recap

In my last WTWA, I predicted a week-long fixation on the Dow 20K story. That was very accurate, with the closest call coming just as I arrived at Chicago’s NBC tower for a CNBC interview on my 2010 forecast. I think it represents a delay rather than a jinx. Some might attribute the selling to the Fed and Chair Yellen’s press conference, an “effect” that was reversed the next day. It must have been meJ I’ll stay at the office for the rest of the year!

The Story in One Chart

I always start my personal review of the week by looking at this great chart from Doug Short. He captures the continuing rally and the move to new highs.

Doug has a special knack for pulling together all the relevant information. His charts save more than a thousand words! Read his entire post where he adds analysis grounded in data and several more charts providing long-term perspective.

Personal

I will have several year-end posts planned for the next two weeks, but will probably skip WTWA next weekend. I am planning a Weighing the Year Ahead installment, probably in two weeks.

The News

Each week I break down events into good and bad. Often there is an “ugly” and on rare occasion something very positive. My working definition of “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

This week’s news was quite good—almost all positive. I make objective calls, which means not stretching to achieve a false balance. If I missed something for the “bad” list, please feel free to suggest it in the comments.

The Good

-

Framing lumber prices are higher, year-over-year. Calculated Risk sees this as an important leading indicator for housing, so we should, too.

-

Initial jobless claims edged lower, to 254K.

-

Hotels are close to an occupancy record. (Calculated Risk).

-

The Fed provided the expected increase in rates with almost no market reaction. (That is the good part). Tim Duy provides some insight. See also “Davidson” via Todd Sullivan.

-

The Philly Fed showed a big gain to 21.5 (7.6 prior) and trouncing expectations. I am not very interested in the Empire State survey, but it mirrored the Philly result. Business and consumer confidence have both strengthened since the election. Confidence is essential for spending, investment, and economic strength.

-

Inflation is still tame, even as it creeps toward the Fed’s target.

-

Household balance sheets are much stronger. Scott Grannis regularly produces this chart. It is far more valuable than material from those focusing exclusively on debt, and ignoring assets.

-

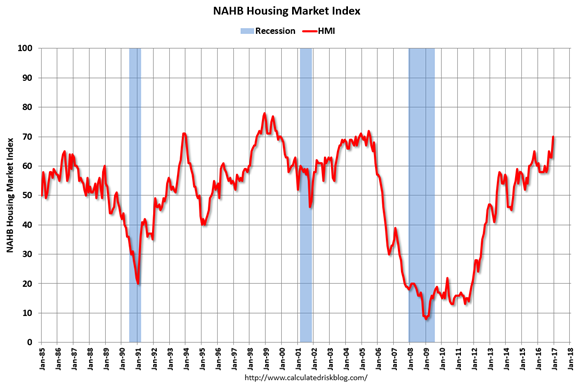

Homebuilder confidence hits the highest level since 2005. (Calculated Risk).

The Bad

-

Industrial production declined by 0.4% from October to November.

-

The rail contraction continues. Steven Hansen continues his coverage with multiple takes and time frames. Check it out!

-

China/drone incident. The drone seizure coincided with Friday selling, a hint of market reaction to sensitive international issues. China will return the drone and claims that the story was “hyped up.”

-

High frequency indicators edge lower. NDD’s useful weekly compilation shows continuing strength in short leading indicators, neutral in the coincident group, and some weakness in the long term. He is downplaying the effects due to seasonality, but it bears watching.

-

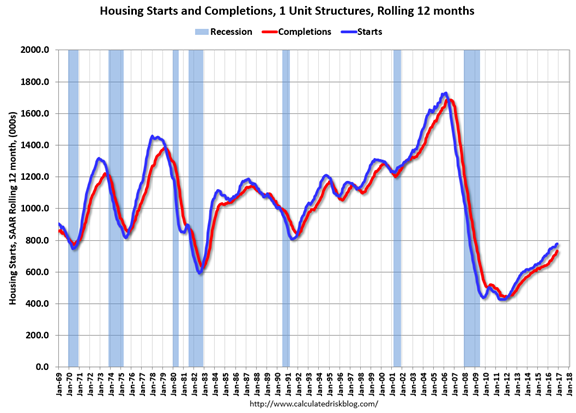

Housing starts dropped by 18.7%. This was a very bad headline number. Various sources suggest that it emphasizes multi-family while single-family is strong. This is a shift that is quite acceptable, so we should follow it closely. Calculated Risk, our go-to source on all things housing, has a great analysis and this chart.

The Ugly

The Young. Colleges are profiting from helping credit card companies. The choices are frequently worse than the student could find otherwise.

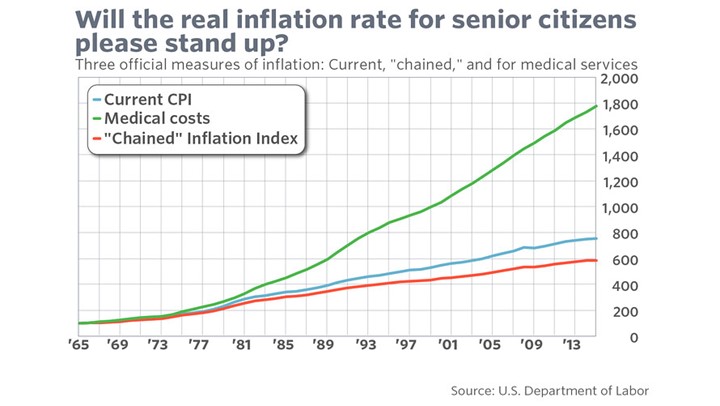

The Old. Brett Arends opines that cost-of-living adjustments may soon end. Already the inflation rate for seniors, mostly because of medical costs, exceeds the standard CPI calculation.

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. No award this week, but opportunities abound and nominations are welcome!

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead. You can make your own predictions in the comments.

The Calendar

We have a normal week for data, loaded into the latter part of the week. Things will get very quiet after Friday’s opening.

The “A” List

- Michigan sentiment (F). Confidence is important right now. Will the mid-month preliminary high hold up?

- New home sales (F). Not much change expected in this important sector.

- Leading indicators (Th). This widely followed measure is likely to be flat.

- Personal income and spending (Th). This important read on the economy is expected to show solid growth.

- Initial claims (Th). The best concurrent indicator for employment trends.

The “B” List

Despite the end of the FOMC quiet period, we have little FedSpeak. Chair Yellen makes an early-week appearance, and that is all I see.

Next Week’s Theme

Last week attention focused on Dow 20K. This was true even though it is a rather meaningless round number in a flawed index. It shows the power of symbolism to attract attention. When the rally fizzled out, the story swiftly turned. Everyone questions rapid, short-term moves, so it is a natural for the punditry.

I expect it to carry over into a quiet week, with plenty of focus on 2017. The popular question will be about what could stop the rally. What should we worry about? It is time to rebuild the wall or worry.

What could go wrong?

Pundits were already hard at work last week:

You should ignore the lists or 2017 winners.

Trump’s policies might not get enacted, disappointing markets. S&P businesses are in line for $87.1 billion.

Trump’s policies might be enacted, hurting the economy and markets. (Think trade matters).

Trump might make a bad decision in a crisis. An ill-timed tweet?

Valuations are still excessive. Stocks are too pricey to buy.

The Fed and a strong dollar might hurt earnings.

Stocks might get too expensive for dividend reinvestment. (You can’t make this up).

Bonds are sending a warning.

Or maybe we should look at the bright side?

A nice reversal from the negativity of last January, the worst start to a year ever. (Josh Brown).

The rally is real. Brian Wesbury’s valuation model showed stocks as 30% under-valued on election day.

20% upside for next year? Brian Gilmartin sticks to the facts. This is an earnings-based conclusion.

What should investors conclude from these sharply conflicting ideas? As usual, I’ll have a few ideas of my own in today’s “Final Thoughts”.

Quant Corner

We follow some regular great sources and the best insights from each week.

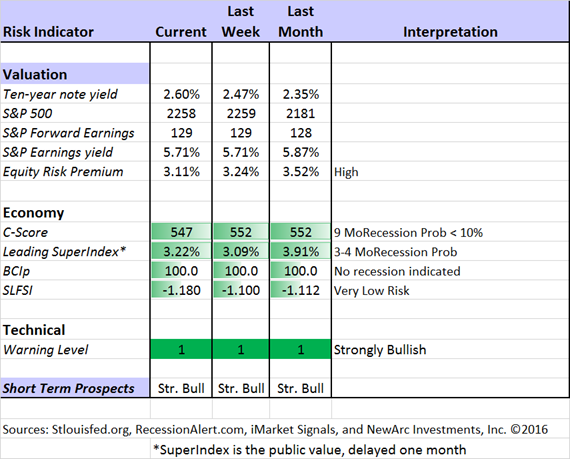

Risk Analysis

Whether you are a trader or an investor, you need to understand risk. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

The Indicator Snapshot

The increased yield on the ten-year note has lowered the risk premium a bit. I suspect much more to come. By this I mean that the relative attractiveness of stocks and bonds will continue to narrow.

The Featured Sources:

Bob Dieli: The “C Score” which is a weekly estimate of his Enhanced Aggregate Spread (the most accurate real-time recession forecasting method over the last few decades). His subscribers get Monthly reports including both an economic overview of the economy and employment.

Holmes: Our cautious and clever watchdog, who sniffs out opportunity like a great detective, but emphasizes guarding assets.

Brian Gilmartin: Analysis of expected earnings for the overall market as well as coverage of many individual companies.

RecessionAlert: Many strong quantitative indicators for both economic and market analysis. While we feature his recession analysis, Dwaine also has several interesting approaches to asset allocation. Try out his new public Twitter Feed. His most recent research update suggests some “mixed signals” from labor markets.

Georg Vrba: The Business Cycle Indicator and much more. Check out his site for an array of interesting methods. Georg regularly analyzesBob Dieli’s enhanced aggregate spread, considering when it might first give a recession signal. Georg thinks it is still a year away. It is interesting to watch this approach along with our weekly monitoring of the C-Score.

Doug Short: The World Markets Weekend Update (and much more). Jill Mislinski updates the ECRI coverage, noting that their public leading index is at the highest point since 2010. Surprisingly, the ECRI public statements remain bearish on the U.S. economy, the global economy, and stocks. It is as if they never recovered from the bad recession call in 2011. They have been out of step ever since.

James Picerno highlights an important, oft-ignored relationship. Many worry about higher interest rates. He notes the relationship between higher rates and stronger economic growth.

How to Use WTWA (especially important for new readers)

In this series, I share my preparation for the coming week. I write each post as if I were speaking directly to one of my clients. Most readers can just “listen in.” If you are unhappy with your current investment approach, we will be happy to talk with you. I start with a specific assessment of your personal situation. There is no rush. Each client is different, so I have six different programs ranging from very conservative bond ladders to very aggressive trading programs. A key question:

Are you preserving wealth, or like most of us, do you need to create more wealth?

My objective is to help all readers, so I provide several free resources. Just write to info at newarc dot com. We will send whatever you request. We never share your email address with others, and send only what you seek. (Like you, we hate spam!) Free reports include the following:

- Understanding Risk – what we all should know.

- Income investing – better yield than the standard dividend portfolio, and less risk.

- Holmes and friends – the top artificial intelligence techniques in action.

- Why it is a great time to own for Value Stocks – finding cheap stocks based on long-term earnings.

You can also check out my website for Tips for Individual Investors, and a discussion of the biggest market fears. (I welcome questions on this subject. What scares you now?)

Best Advice for the Week Ahead

The right move often depends on your time horizon. Are you a trader or an investor?

Insight for Traders

We consider both our models and the top sources we follow.

Felix and Holmes

We continue with a strongly bullish market forecast. Felix is fully invested. Oscar is fully invested in aggressive sectors. The more cautious Holmes also remains fully invested, but with continued profit-taking and position switching. The group meets weekly for a discussion they call the “Stock Exchange.” This week we had a great topic – whether the focus on Dow20K had an effect on technical analysis. The prior two segments were on limiting risk and maximizing returns. (We report exits from announced Holmes positions if you ask to be on that list. Write to holmes at newarc dot com).

Top Trading Advice

Brett Steenbarger continues to provide almost daily insights for traders. Sometimes the ideas draw upon his expertise in psychology. Sometimes they emphasize his skills in training traders. Sometimes there are specific trading themes. They all deserve reading. This week I especially liked the following:

- More benefits of keeping a trading journal – and a good idea from that noted trader, Bertrand Russell.

- A clever method for generating new trading ideas – reading in parallel.

Adam H. Grimes has an excellent piece on finding ideas. You must be experienced, but also avoid confirmation bias. Dr. Brett gives a HT and follows up.

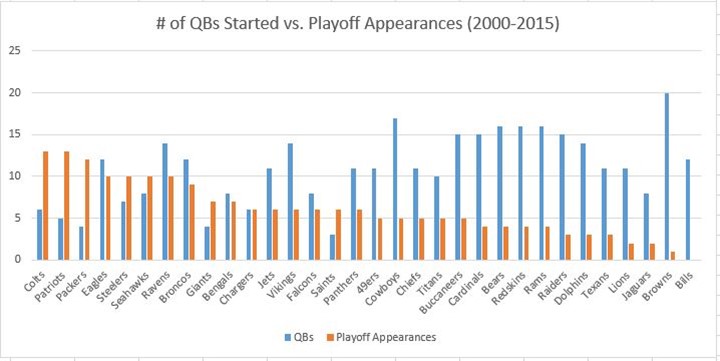

Brendan Mullooly takes one of my favorite approaches – drawing a lesson from outside trading, especially from sports. This approach helps rid us of confirmation bias, providing a fresh look. Check out the full post for data on the impact from overtrading. And the sports analogy? Teams that keep switching quarterbacks!

[This chart was approved by Mrs. OldProf, a native of Green Bay and a knowledgeable football fan.]

Insight for Investors

Investors have a longer time horizon. The best moves frequently involve taking advantage of trading volatility!

Best of the Week

If I had to pick a single most important source for investors to read this week it would be advice from legendary investor Peter Lynch. Instead of finding something from the last week, I wanted to find the best choice for current conditions. Ben Carlson did the Peter Lynch report about two years ago, starting with this very relevant quotation:

Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.

And also….

Now no one seems to know when they are gonna happen. At least if they know about ’em, they’re not telling anybody about ’em. I don’t remember anybody predicting the market right more than once, and they predict a lot. So they’re gonna happen. If you’re in the market, you have to know there’s going to be declines. And they’re going to cap and every couple of years you’re going to get a 10 percent correction. That’s a euphemism for losing a lot of money rapidly. That’s what a “correction” is called. And a bear market is 20-25-30 percent decline.

They’re gonna happen. When they’re gonna start, no one knows. If you’re not ready for that, you shouldn’t be in the stock market. I mean the stomach is the key organ here. It’s not the brain. Do you have the stomach for these kinds of declines? And what’s your timing like? Is your horizon one year? Is your horizon ten years or 20 years?

What the market’s going to do in one or two years, you don’t know. Time is on your side in the stock market.

Stock Ideas

Lee Jackson has an interesting screen that produced 5 Dividend Stocks that You Can Still Buy With Market at Record Highs. “We screened the Merrill Lynch research data base for stocks that are rated Buy, pay a dividend and haven’t gone parabolic this year. We found five that make good sense for investors”.

Wind energy stocks have been left behind in the “Trump rally.” Buying opportunity or victim of policy changes?

But keep in mind that solar is now cheaper than wind energy. Tom Randall (Bloomberg Technology) has a helpful analysis of how much and why.

Our trading model, Holmes, has joined our other models in a weekly market discussion. Each one has a different “personality” and I get to be the human doing fundamental analysis. We have an enjoyable discussion every week, including four or five specific ideas that we are buying. This week Holmes likes Amgen (AMGN). Check out the post for my own reaction, and more information about the trading models.

While we cannot verify the suitability of specific stocks for everyone who is a reader, the ideas have worked well so far. My hope is that it will be a good starting point for your own research. Holmes may exit a position at any time. If you want more information about the exits, just sign up via holmes at newarc dot com. You will get an email update whenever we sell an announced position.

Some Merrill Lynch top picks for 2017 (via 24/7 Wall Street).

Ben Levisohn (Barron’s) sees 23% upside for FedEx.

Interested in REITs? Try health care.

Get ready for Eddy Elfenbein’s new buy list. This annual event is a great source of ideas for investors who like to think in a time frame of at least a year. You can also join in the whole list via Eddy’s new ETF (CWS). It is both convenient and inexpensive.

Personal Finance

Professional investors and traders have been making Abnormal Returns a daily stop for over ten years. If you are a serious investor managing your own account, you should join us in adding this to your daily reading. Every investor should make time for a weekly trip on Wednesday. Tadas always has first-rate links for investors in his weekly special edition. There are always several great choices worth reading. My personal favorite this week is the important article by Jonathan Clements on your personal risk-free rate. It is not the T-Bill or T-Note from financial analysis, but your own most costly loan. This may seem obvious, but many people fail to consider it in their financial calculations.

Seeking Alpha Editor Gil Weinreich’s Financial Advisors’ Daily Digest is a must-read for financial professionals. The topics are frequently important for active individual investors, so the series is worth following regularly. This week I especially liked the discussion of financial literacy. Even active investors are unable to answer basic questions. WTWA readers would get them all right, so it may seem very surprising.

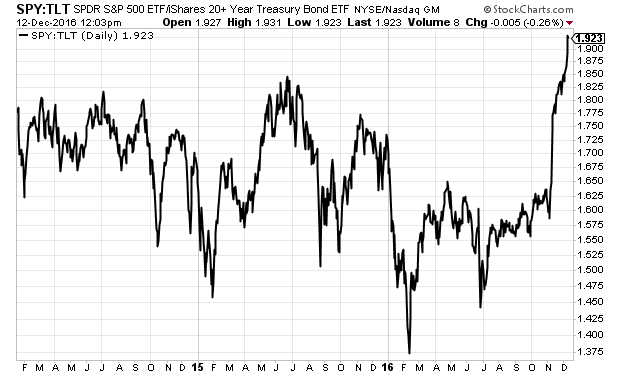

Watch out for…

Bonds cratering while stocks rally. Eddy Elfenbein presents a telling chart.

Final Thoughts

My biggest reason for the 2010 Dow20K post was to alert investors to the idea of “upside risk.” There is always – always – a list of plausible worries. These dominate the news and the financial discussions. The other side is difficult. It is boring to say repeatedly that things are normal and promising. Talking about some new development seems smart – attracting viewers, page views, more gigs to make you famous, and even investors who seek confirmation.

The natural process leads to a focus on problems. These are easy to see, while solutions are not. Therefore, most investors do not understand the ill-named concept of the wall of worry.

The new list of worries, all well-known and reflected in current market prices, is a replacement for those listed on my current “investor fears” page, which replaced those from the 2010 era. It seems smart to study world events and use that knowledge to guide your investment decisions. But it is not!

You cannot make these calls as well as the market does. You are almost certain to over-react.

The investor mistakes I highlighted in 2010 are still with us:

- Excessive attention to headline events;

- Reliance on poor forecasts of the economy, especially recessions; (James Picerno has a great list of typical forecasts)

- Too much reliance on backward-looking earnings, reflective of unusual events and times.

- Ignoring the long-term economic forces putting idle assets to work. (Mark Hulbert on 24K)

- Emphasizing politics instead of investing. In 2008 many investors hated the prospects and principles of the Obama administration. They sat out the start, and never found an entry point.

It is more profitable to accept a measure of uncertainty, rely upon the best recession and earnings indicators, and remain agnostic about politics.

This is a good time to ask yourself about how have you done? If you are wondering whether you might do better with a financial advisor, check out my latest paper, The Top Twelve Investor Pitfalls – and How to Avoid Them. If you regularly navigate these problems, you can fly solo! That is true for 99% of my readers, whom I am trying to help. Some readers might well benefit from our help. Readers of WTWA can get a free copy by sending an email to info at newarc dot com. We will not share your address with anyone.

© NewArc Investments, Inc.

Read more commentaries by NewArc Investments, Inc.