One topic noticeably absent from the recent presidential election was the U.S. government debt. In fact, the topic seems to have fallen from public consciousness: prior to the 2012 election 12% of survey respondents noted the country’s debt and deficit as their primary concern; in the most recent election that number fell to 4%. In the medium term we do not expect current debt levels to cause a shock, but the longer-term effects could drag on growth, especially with an aging population and sluggish economic growth.

Source: Bloomberg LP, US Treasury, Federal Reserve, Bureau of Economic Analysis

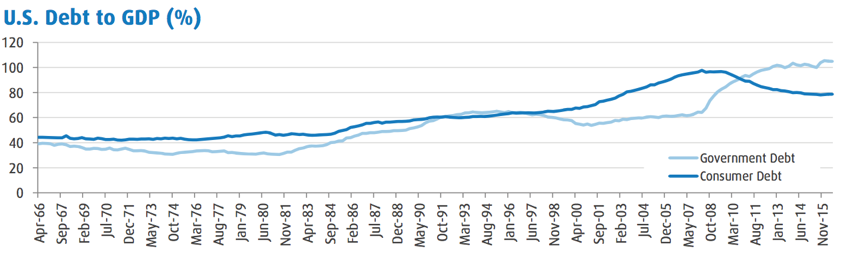

Beginning in the mid 1990s, the American consumer took on a significant amount of debt, mainly through low-down-payment mortgages, credit cards, auto loans and home equity lines of credit. Then, during the economic downturn of the late 2000s the U.S. consumer quickly delevered, causing ripple effects in the U.S. economy, which historically has relied heavily upon consumer spending. The U.S. government then picked up where the consumer left off, widening budget deficits and increasing debt in order to stimulate the economy and cushion the drop in consumer spending. While much of that stimulus has been rolled back and deficits have lately stabilized, this transfer of leverage has left the country with historically high government debt levels.

Source: Bloomberg LP, US Treasury

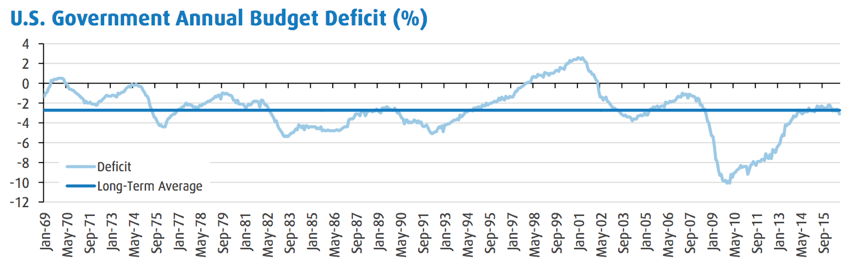

Note: Annual budget deficit is the difference between government revenues and expenditures as a percentage of nominal GDP

Yet despite high debt levels, the U.S. government continues to carry minimal explicit credit risk. Debt servicing costs are quite low; interest on the federal debt accounted for a meager 6% of government expenditures during the 2015 fiscal year. The U.S. benefits from its status as a reserve currency, so there has been ample demand for U.S. Treasurys, especially during times of crisis. U.S. debt is denominated in its own currency — unlike that of many peers in emerging markets — so in a crunch the Federal Reserve could just print more money to pay off outstanding debts. Inflation would likely rise in this scenario, but the government would at least avoid defaulting on its debt. The only plausible path to an explicit U.S. default would involve Congress refusing to raise the debt ceiling, as nearly occurred in 2011 and 2013. But given that Republican control of both the presidency and Congress makes a stalemate less probable, we do not view a repeat of this drama as likely.

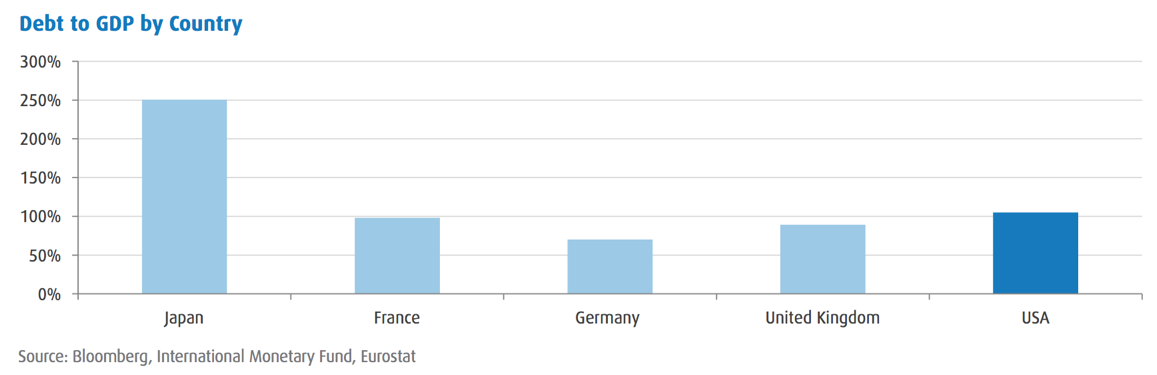

Taking a longer-term perspective, on the other hand, the U.S. debt could prove a drag on the economy as levels continue to rise. Consider Japan, an example (albeit extreme) of a country with poor demographics, extremely high debt levels and slow growth. High debt levels divert money toward unproductive debt servicing and away from productive uses such as infrastructure spending. Japan spends approximately 10% of its budget on debt interest, though ultra-low interest rates mask the true impact of its high debt levels. High debt levels also tend to weigh on economic activity, as businesses and consumers reduce consumption due to a high current tax burden and the potential for even higher taxes in the future.

We expect a renewed public conversation about the government debt over the next year. Budget deficits are widening on a year-over-year basis for the first time since 2010, leading to a slight climb in the closely watched debt-to-GDP ratio. Additionally, President-Elect Donald Trump’s combination of tax cuts and increased spending is forecast to add significantly to the federal debt, though some Republicans in Congress have indicated they prefer a more revenue-neutral approach. The recent increase in interest rates will also pose a problem as the cost of servicing the debt becomes a larger portion of the government’s budget.

Our overweight to U.S. equity meshes well with our analysis of the U.S. debt; over the medium term deficit spending will stimulate the economy without causing a debt crisis. Looking ahead, however, absent broader structural reforms, the high debt load of the U.S. could impede growth over the longer term.