We highlight which strategies could possibly benefit from policy changes, rising rates and more

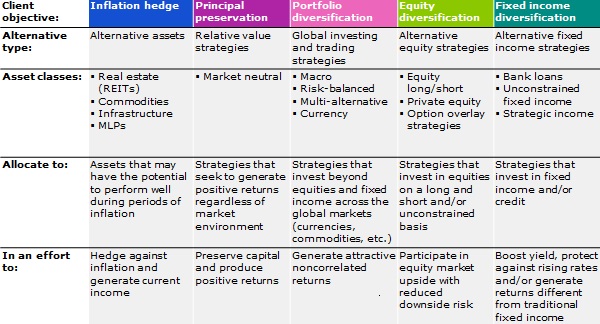

As we enter 2017, there is a long list of issues that could affect alternative investments: policy changes in the US, elections in Europe, rising rate expectations and more. Given this changing landscape, I would like to highlight some alternative investments that I believe have the potential to benefit investors in the new year. In doing so, I’ll be using Invesco’s Alternatives Framework (see below) to identify strategies for each of the five alternative buckets.

Invesco’s Alternatives Framework

Alternative investments to consider in 2017

- Alternative assets: Commodities, MLPs and infrastructure — With the incoming Trump administration focused on economic growth, deregulation, business-friendly energy policy and infrastructure investment, alternative assets such as commodities, master limited partnerships (MLPs) and infrastructure could be poised to benefit. Commodities could benefit from increased inflationary pressure resulting from economic growth, as well as from increased demand for industrial commodities used to build infrastructure, while MLPs and infrastructure investments could benefit from increased construction and a more business-friendly energy policy. Invesco Balanced-Risk Commodity Strategy Fund, Invesco Global Infrastructure Fund and Invesco MLP Fund are examples of alternative asset funds that invest in these opportunities.

- Relative value strategies: Market neutral — There will likely be a great deal of political uncertainty in 2017, given new leadership in the US as well as important elections in France and Germany. Given the likelihood of this uncertainty, investors may want to consider market neutral funds. These funds are designed to neutralize the effects of overall market movements and to generate returns based on the movements of individual stocks.1 Given their unique nature, market neutral funds may help insulate against market swings, have the potential to generate positive returns in all market environments, and may produce returns that have low correlation to stocks and bonds. Invesco Global Market Neutral Fund is an example of a typical market neutral fund, while Invesco All Cap Market Neutral Fund is an example of a more aggressive version of market neutral (i.e., it seeks higher returns in exchange for higher risk).

- Global investing and trading strategies: Global macro — Global macro funds invest opportunistically on a long and short basis across the global equity, fixed income, currency and commodity markets. These funds have the ability to select which markets they want, and don’t want, to invest in. And, because they can invest on both a long and short basis, they have the potential to achieve profits in both rising and falling market environments. I think 2017 could present global macro funds with numerous opportunities, especially given the potential for accommodative US fiscal and regulatory policy, and divergent monetary policy between the US and Europe. Investors looking for a strategy that can opportunistically trade across the global markets while offering potential diversification benefits should consider global macro funds, in my view. Invesco Global Targeted Returns Fund and Invesco Macro Allocation Strategy Fund are examples of global macro funds.

- Alternative equity: Long/short equity — Long/short equity funds combine long and short equity positions in a portfolio, while typically being net long to equities. As a result, these funds have a positive beta to equities, and performance tends to directionally follow the equity market. Two key differentiators across such funds are their inclusion of short positions in the portfolio and their typical net exposure to the market. I prefer long/short strategies that maintain a high net long exposure to equities and have demonstrated a proven ability to add value through their short positions during all parts of the market cycle (as opposed to only during periods of equity weakness). In my view, such strategies are well-positioned to provide equity-like exposure while offering the potential to outperform equities in both rising and falling equity markets (due to gains from their short positions). Investors looking for this type of opportunity might talk to their advisor about replacing some of their long-only equity exposure with exposure to a long/short equity fund. Invesco Long/Short Equity Fund is an example of such a fund.

- Alternative fixed income: Senior loans (also known as bank loans, senior secured loans and/or leveraged loans) — Investors looking to earn an attractive yield and benefit from rising interest rates should consider an investment in senior loans. Senior loans are loans made by banks to non-investment grade companies, often to fund leveraged buyouts, mergers and acquisitions. The loans are called “senior” because they are contractually senior to other debt and equity, and are typically secured by collateral. Given that the loans are made to non-investment grade companies, the yield associated with them tends to be higher than the yield for investment grade corporate bonds.2 Another key aspect of senior loans is that they pay a floating interest rate that resets every 30 to 90 days.3 This means that in a rising interest rate environment, as long as the rate rises above a predetermined minimum level, the investor will receive increased payments from the borrower. Invesco offers three different senior loan strategies for individual investors: Invesco Floating Rate Fund (which offers daily liquidity), Invesco Senior Loan Fund (which offers monthly liquidity) and PowerShares Senior Loan Portfolio (an exchange-traded fund).

For more information about alternatives

- To learn more about Invesco’s alternative strategies, please visit invesco.com/alternatives.

- You can also read previous blogs from Walter Davis, and ask Walter your questions about alternatives with our Ask the Expert feature.

- And, learn why it’s time to say goodbye 60/40 and to consider alternatives as more of your core.

Explore Invesco’s 2017 Investment Outlook Series.

1 Market neutral funds trade related equities on a long and short basis, such that the funds have close to a zero beta and close to zero net market exposure. In market neutral funds, the key to generating a positive return is security selection — determining which equities to go long and which to go short.

2 This is due to the increased credit risk associated with non-investment grade companies relative to investment grade companies.

3 Senior loans are usually priced relative to three-month Libor, with the lender receiving a fixed spread above the Libor rate. Therefore, as Libor rises, the amount paid by the borrower increases. Importantly, most loans have a provision that establishes a minimum, or floor, for Libor. Typically the floor rate is around 1%. As of Dec. 15, 2016, the three-month Libor rate was approximately 0.99%. Therefore, Libor would need to rise above the 1% floor before the investor would receive the benefit of rising interest rates.

Walter Davis

Alternatives Investment Strategist

As Alternatives Investment Strategist, Walter Davis serves as Invesco’s primary alternatives representative to retail, high net worth and institutional clients across the major broker dealers, wirehouses and RIAs. He is responsible for collaborating across Invesco’s alternative strategies to develop a cohesive alternatives education program for financial advisors and investors.

Prior to joining Invesco in 2014, Mr. Davis served as a managing director in Morgan Stanley’s Alternative Investments Department, and earlier as director of High Net Worth and Institutional Sales. Prior to Morgan Stanley, he worked at Chase Manhattan Bank in the Alternative Investments Department. He has worked in the industry since 1991.

Mr. Davis graduated cum laude with a BA in economics from the University of the South. He earned an MBA in finance and international business from Columbia Business School. He holds the Series 3, 7, 24 and 63 registrations.

Important information

Correlation is the degree to which two investments have historically moved in relation to each other.

Beta is a measure of risk representing how a security is expected to respond to general market movements.

Diversification does not guarantee a profit or eliminate the risk of loss.

Alternative products typically hold more nontraditional investments and employ more complex trading strategies, including hedging and leveraging through derivatives, short selling and opportunistic strategies that change with market conditions. Investors considering alternatives should be aware of their unique characteristics and additional risks from the strategies they use. Like all investments, performance will fluctuate. You can lose money.

Commodities may subject an investor to greater volatility than traditional securities such as stocks and bonds and can fluctuate significantly based on weather, political, tax, and other regulatory and market developments.

Most MLPs operate in the energy sector and are subject to the risks generally applicable to companies in that sector, including commodity pricing risk, supply and demand risk, depletion risk and exploration risk. MLPs are also subject to the risk that regulatory or legislative changes could eliminate the tax benefits enjoyed by MLPs, which could have a negative impact on the after-tax income available for distribution by the MLPs and/or the value of the portfolio’s investments.

Investment in infrastructure-related companies may be subject to high interest costs in connection with capital construction programs, costs associated with environmental and other regulations, the effects of economic slowdown and surplus capacity, the effects of energy conservation policies, governmental regulation and other factors.

Most senior loans are made to corporations with below-investment grade credit ratings and are subject to significant credit, valuation and liquidity risk. The value of the collateral securing a loan may not be sufficient to cover the amount owed, may be found invalid or may be used to pay other outstanding obligations of the borrower under applicable law. There is also the risk that the collateral may be difficult to liquidate, or that a majority of the collateral may be illiquid.

Short sales may cause an investor to repurchase a security at a higher price, causing a loss. As there is no limit on how much the price of the security can increase, exposure to potential loss is unlimited.

The risks of investing in securities of foreign issuers can include fluctuations in foreign currencies, political and economic instability, and foreign taxation issues.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

Before investing, investors should carefully read the prospectus and/or summary prospectus and carefully consider the investment objectives, risks, charges and expenses. For this and more complete information about the fund(s), investors should ask their advisors for a prospectus/summary prospectus or visit invesco.com/FundProspectus.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC, investment adviser. Invesco PowerShares Capital Management LLC (PowerShares) and Invesco Distributors, Inc., ETF distributor, are indirect, wholly owned subsidiaries of Invesco Ltd.

©2017 Invesco Ltd. All rights reserved.

What May Be in Store for Alternatives in 2017? by Invesco