The Trump Era Begins

We could conceivably write a Pyrspectives without referring to THE election and President-elect Trump and, to be frank, it is tempting to do so as there are so many unknowns that it is difficult to be cogent and value-additive. Nevertheless, we feel compelled to make some stumbling attempt at comment. We never fall into the trap of forecasting the outcome of elections, but if we are being totally honest we did believe it unlikely that we would end up discussing a Trump Presidency.

The first observation to make is that the stock market clearly likes the prospect of Mr. Trump at the helm. The “Trump-bounce” in the stock indices is very pronounced even on very longterm charts. The market likes the sound of a big-spending President, who has also promised a substantial reduction in the corporate tax rate. The jaw-boning about tariffs and protection seems not to disturb the traders one whit (it disturbs us!).

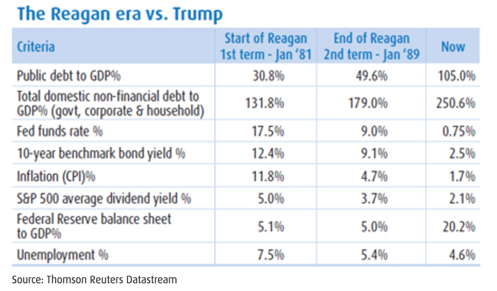

Janet Yellen, Chair of the Federal Reserve, has met the change of leader head-on by raising the Fed Funds rate by a quarter of one percent whilst forecasting as many as three increases in 2017. The exuberance shown by Wall Street to Trump’s election victory left her with little option but to make a move. The bond market, on the other hand, has not been appreciative of this turn of events. Yields across all maturities have risen sharply — and not just in the U.S. The U.S. 10-year benchmark treasury yield dipped to a low point of 1.36% on July 8th this year. At the time of writing it has risen to 2.5%. Ouch! (If you’re a holder). If you are a non-holder (and, in particular, a defined-benefit pension fund) you should be cheering. Finally, bond yields may begin to make some sense. We have read many times that Mr. Trump could be another President Reagan — that is, a President not afraid to turn the fiscal spigots at a rapid rate — spend the money now in the hope that growth eventually bails you out. At the risk of being accused of being out-of touch curmudgeons (again), we feel it necessary to point out some major differences between January 1981 and today. Take a look at the table below:

Mr. Reagan inherited a stagnant economy with high inflation and massive interest rates (they go hand-in-hand) but, importantly, very low levels of public and private debt. He was able to spend big and encourage others to do so, safe in the knowledge that the fiscal situation was more or less in control — at least during his two terms. Inflation and interest rates tumbled and the economy perked up (eventually). Mr. Trump, on the other hand, inherits an economy with tiny interest rates, record debt levels, an expensive stock market, modest growth, near-full employment, extremely low inflation and a central bank that has blown its balance sheet four-fold (relative to GDP) since the Reagan years. The money has poured into the system but the economic wheels have gained little traction — with the obvious exception of the stock and bond markets.

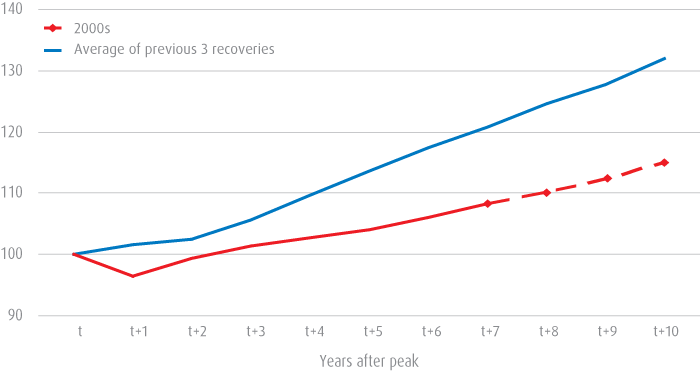

The Organization for Economic Co-operation and Development (OECD) has published some insightful work on just how poor the “recovery” from the 2008-9 recession has been, relative to the previous three recession recoveries. The data relates to all OECD member countries but the trend applies equally to the United States. The economic wheels have been skidding all over the world.

GDP Growth following recessions

The public debt situation in the U.S. gives the President-elect very little wiggle room. The OECD, in its latest forecast, suggests that nominal GDP may be able to outgrow the expansion in public expenditure mooted by Mr. Trump. Maybe, but the economic lessons from the last decade and a half give us justified cause for skepticism.

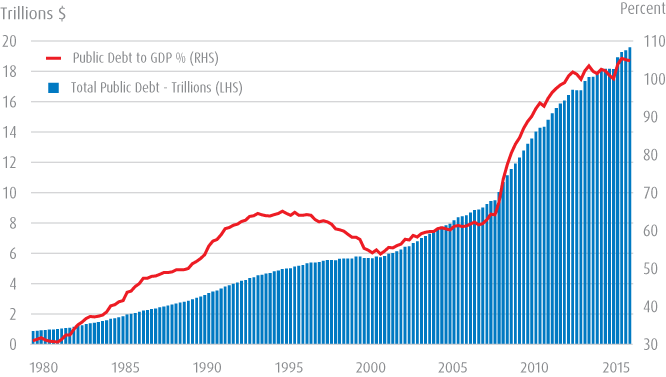

Public debt

Treasury securities outstanding

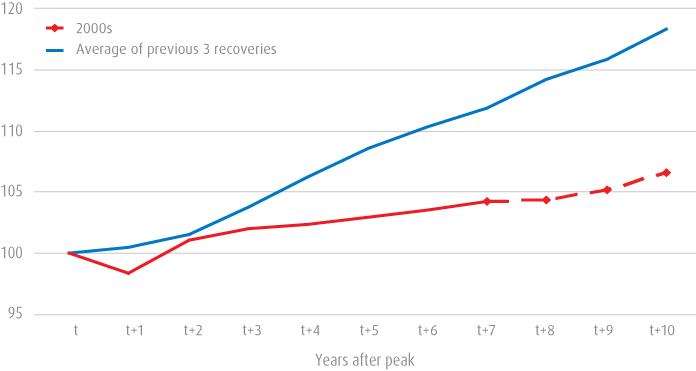

It seems that every politician, of whatever political persuasion, is tempted to spend money that is not theirs. The rewards of doing so flow to the few. It is a sad but true fact that the gap between the “haves” and the “never will have” continues to widen. We doubt that the policies of the President-elect will do anything to redress this imbalance. It is not just the headline GDP statistics that have been well below par during this “recovery”. The comment applies equally to employment, real wages, consumption, trade, labour productivity and capital investment. All of these factors are inextricably linked with cause and effect, always difficult to disentangle, but if one stands above the others as indicative of the economic malaise since the crisis it is the global phenomena of weak productivity growth (output per worker). Once again the OECD provides us with a stark illustration of the difference “this time around” relative to the past.

Labor productivity growth following recessions

Aggregate data for OECD economies (output per worker)

The view that we have expressed in past Pyrspectives is that loading an economy with debt is a palliative that works for a while but inevitably reaches a point of diminishing returns and then downright danger. The financial crisis of 2008-9 is an example of the “downright danger” stage. Since then, the ebb and flow of the global economy has been decidedly “odd” — it has been unlike any other post-recession recovery as the OECD has highlighted — and it doesn’t appear that it is about to change.

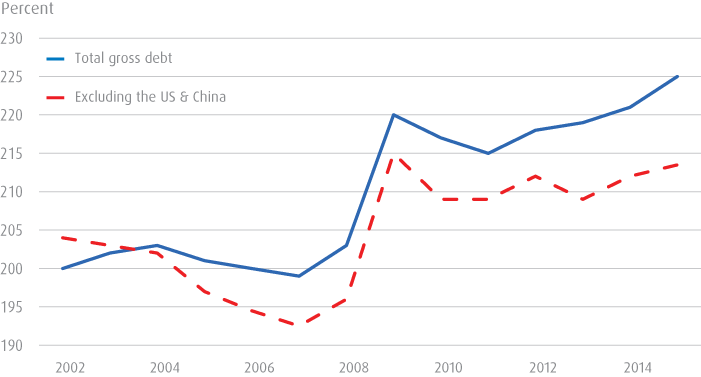

The household sector in the U.S. and a few other countries has moderated its debt load (relative to income) but governments, central banks and corporations have added vast sums to the pile so that the overall debt statistics are now at record levels (see graph below). Our “fear gauge” therefore remains elevated.

Can Mr. Trump perform miracles? How can we indulge in meaningful speculation about the unforecastable? The President-elect does have some relevant experience — running companies with mountains of debt. He is now about to take leadership of the world’s biggest economic (and military) entity and $20 trillion of public debt. He will probably relish the challenge and still sleep soundly at night, whereas the rest of us are likely to be tossing and turning for four years. It won’t be dull!

Gross global debt

As at % of GDP (weighted average)

Disclosures

All investments involve risk, including the possible loss of principal.

Foreign investing involves special risks due to factors such as increased volatility, currency fluctuation and political uncertainties. High yield bond funds may have higher yields and are subject to greater credit, market and interest rate risk than higher-rated fixed-income securities. Keep in mind that as interest rates rise, prices for bonds with fixed interest rates may fall. This may have an adverse effect on a Fund’s portfolio.

Investments cannot be made in an index.

This presentation may contain targeted returns and forward-looking statements. “Forward-looking statements,” can be identified by the use of forward-looking terminology such as “may,” “should,” “expect,” “anticipate,” “outlook,” “project,” “estimate,” “intend,” “continue” or “believe” or the negatives thereof, or variations thereon, or other comparable terminology. Investors are cautioned not to place undue reliance on such returns and statements, as actual returns and results could differ materially due to various risks and uncertainties. This material does not constitute investment advice. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. Investors should seek advice regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Investment involves risk. Market conditions and trends will fluctuate. The value of an investment as well as income associated with investments may rise or fall. Accordingly, investors may receive back less than originally invested.

Pyrford International Ltd. (Pyrford) is a registered investment adviser and a wholly owned subsidiary of BMO Financial Corp. BMO Global Asset Management is the brand name for various affiliated entities of BMO Financial Group that provide investment management and trust and custody services. Certain of the products and services offered under the brand name BMO Global Asset Management are designed specifically for various categories of investors in a number of different countries and regions and may not be available to all investors. Products and services are only offered to such investors in those countries and regions in accordance with applicable laws and regulations. BMO Financial Group is a service mark of Bank of Montreal (BMO).

BMO Asset Management Corp. is the investment adviser to the BMO Funds. BMO Investment Distributors, LLC is the distributor. Member FINRA/SIPC.

BMO Asset Management Corp., BMO Investment Distributors, LLC, BMO Private Bank, BMO Harris Bank N.A. and BMO Harris Financial Advisors, Inc. are affiliated companies. BMO Private Bank is a brand name used in the United States by BMO Harris Bank N.A. BMO Harris Financial Advisors, Inc. is a member FINRA/SIPC, an SEC registered investment adviser and offers advisory services and insurance products. Not all products and services are available in every state and/or location.

Investment products are: NOT FDIC INSURED — NOT BANK GUARANTEED — MAY LOSE VALUE.

© 2017 BMO Financial Corp. (5376876, 1/17)

© BMO Global Asset Management

Read more commentaries by BMO Global Asset Management