“Forecasts usually tell us more of the forecaster than of the future.”

Warren Buffett

Each week during American football season the New York Post proudly presents the Bettor’s Guide to its readers. The Post’s 11 (so-called) experts advise the newspaper’s readers as to which teams to bet on. The Post introduced the service in 2015, and the results of the first full season covering 256 games were as follows:

- The best picker was right 55.1% of the time.

- The worst picker was right 48.8% of the time.

- On average, the pickers were right 51.6% of the time.

Flattering? Not really. One could argue that a coin toss would deliver a more profitable outcome after costs so, in that respect, it is not that different from our industry.

Crucified by Howard Marks

The example above is – almost word for word – taken from Howard Marks’[1] most recent client memo, aptly named Expert Opinion (see here). It came through my letterbox a few weeks ago, and I began to read it almost immediately, as I almost always do when receiving his commentary. Howard is one heck of a smart guy. He is also very nice and very approachable – a true gentleman as I learned, when I ran into him in Munich a few years ago.

The gist of Howard’s recent letter is Who really knows? As he points out, we all spend so much time trying to figure out what is going to happen; yet little do we know how it will all pan out. Do I need to say more than Brexit or Trump?

When I put his letter away, my first reaction was to retire from writing. Then I started to think. What is it we actually do at Absolute Return Partners? Are we wasting everybody’s time by focusing on things that are, almost by definition, unpredictable?

If you have followed my writing for a while, you will know that I spend only a limited amount of time on cyclical trends. Why is that? Because I happen to agree with Howard that trying to predict currencies, interest rates or equity prices over the short term is largely a mug’s game (my words, not Howard’s).

However, there is another way, and that is what we do at Absolute Return Partners. We largely ignore shorter term cyclical and behavioural trends (we call those trends tactical trends) and instead tune into structural trends. Almost all of them are longer term in nature, so don’t plan to turn yourself into a day trader armed with the knowledge and information I am about to share with you.

Let me give you some examples but, before I do so, I should stress that the three examples below are only a subset of all the structural trends we have identified. I should also point out that we distinguish between what we call structural mega-trends and structural sub-trends.

The examples below are all mega-trends, and we have identified a total of six of those. In addition to them, we have also identified eight structural sub-trends. Think of the mega-trends as the trends that provide the big picture and the sub-trends as the trends that drive the investment strategies we end up investing in (or stay clear of).

I have written about all these trends over the years so, if you have been reading the Absolute Return Letter regularly for years, none of this will be new to you. The following trends are the three most important mega-trends that we have identified in recent years – at least as far as financial markets are concerned - and they are all likely to have a significant impact on financial asset prices in the years to come. They are as follows:

- The retirement of the baby boomers.

- The declining spending power of the middle classes.

- The end of the debt super-cycle.

Howard is not correct when he says – or at least insinuates – that no one really knows. We certainly know that certain things will happen, given the mega-trends just referred to. On the other hand, I would totally agree that none of these trends are of much use, if it is about guesstimating what is likely to happen to the dollar (or any other financial asset class) over the next few weeks.

The six mega-trends that we have identified again drive a number of sub-trends. I will give you an example of such a sub-trend, so you can see how these trends interact. Take the declining spending power of the middle classes, which continues to suppress economic growth. Governments will, as a result, be forced to put more emphasis on fiscal policy as opposed to monetary policy; i.e. that becomes one of our eight sub-trends.

That again has wide-ranging investment implications, the most obvious one of which is an emphasis on infrastructure via increased public spending. The beauty of this entire set-up is that ‘our’ structural mega-trends are certain to happen (most of them are actually unfolding as we speak), whereas the structural sub-trends that we have identified are exceedingly likely to happen so, in that respect, Howard is wrong. It is actually possible to make fairly accurate predictions about the future, as long as you approach the subject appropriately.

Can the US economy really grow as fast as Trump has promised?

Because of the shrinking spending power of the middle classes, because demographics are increasingly adverse, and because more and more capital that really should be employed productively is instead used to service existing debt, we know that economic growth will, with 99.9% likelihood, be quite soft for years to come.

That doesn’t mean we cannot enjoy a phenomenally good year every now and then, but it does mean that Trump’s promise to the American populace that he can deliver 3.5-4.5% annual GDP growth consistently is a pie in the sky.

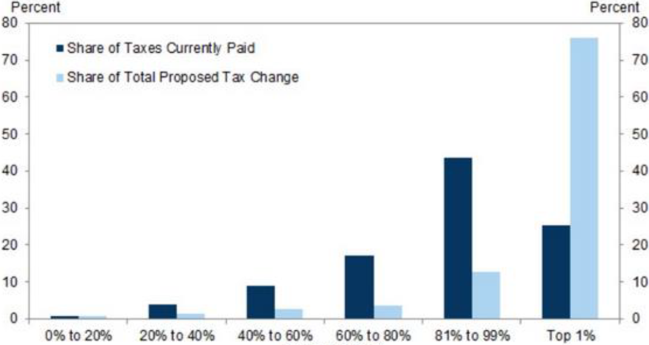

Trump has already promised that he will reduce the tax burden; he has in fact declared that he will make tax cuts across the board – to individuals and to corporates. The Congressional Budget Office has done some interesting work around the current proposal, and they have found that – if implemented – the tax cuts will benefit the top 1% of income earners the most. No less than 75% of the proposed tax change will fall into the pockets of the top 1%, whereas the bottom 80% - many of whom voted for Trump – will hardly benefit at all (exhibit 1).

Exhibit 1: Impact on proposed US income tax cuts by income bracket

Source: Tax Policy Center, Congressional Budget Office, January 2017

However, if you read the December Absolute Return Letter (see here), you will know that it is the spending power of the global middle classes – which would include the vast majority of US income earners – that needs to be boosted, if we want the economy to get going again, and Trump’s tax plans do absolutely nothing to fix that problem.

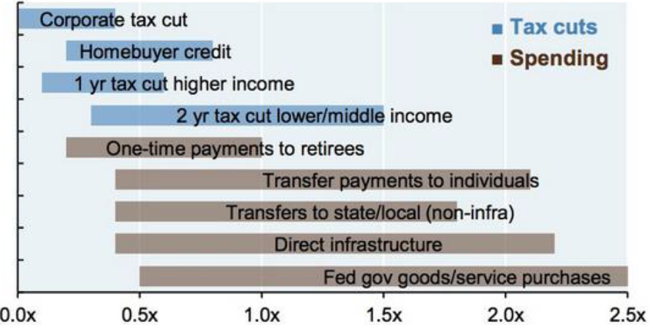

Adding to that, Trump also wants to reduce the corporate tax rate, but that is about the least effective policy tool he could come up with, if the intention is to accelerate economic growth. Where infrastructure spending leads to a significant increase in national income, a reduction of the corporate tax rate does little to that effect (exhibit 2).

As you can also see from exhibit 2, tax cuts in general are not nearly as effective as other policy tools, but they are more popular! That said, with the man on the street likely to be left behind yet again, it won’t take long before he realises that Trump is not the man he had hoped for.

In the January Absolute Return Letter (see here) I argued for potential problems in US equities in 2017. Since election day in early November we have enjoyed numerous new highs in US equities, and there seems to be no end to the optimism that Trump has brought in.

If my assessment of his tax plans is correct, the end result could be quite different from what markets expect today. Economic growth should remain muted, and companies could struggle to deliver the results many take for granted now. If that won’t increase the accident prone nature of US equity markets, I am not sure I know what will.

Exhibit 2: Estimated fiscal multiplier range

Source: Congressional Budget Office, February 2015

Beta, alpha, gamma and credit risk

At Absolute Return Partners we distinguish between four types of risk – beta, alpha, gamma and credit risk. Beta risk is market risk – plain and simple. Credit risk is precisely what is says on the tin. Gamma risk is a mixed bag of various types of risk away from market and credit risk.

Alpha risk is the contentious one. The way the vast majority of investors think of it – and admittedly also the way we defined it until the Blu Family Office (see here) became part of the ‘Absolute family’ – alpha risk is the risk of underperforming the markets, i.e. doing worse than you would do through sheer beta exposure.

Then Blu turned up on our doorstep, and they convinced us that there is more than one way to think of alpha risk. According to Blu, alpha risk is the risk of mis-pricings, and that would include inefficiencies. In Blu’s terminology, you can only generate alpha if you can extract the mispricing through the opening and closing of opposing trading positions.

A major source of returns in recent years has been the so-called illiquidity premium. Tie up your capital for five years, and suddenly (expected) returns spike, but there are obviously risks associated with such a strategy. We often come across investment managers, who proudly tell us they generate plenty of alpha but, quite often, what those managers actually do has nothing whatsoever to do with alpha, whether you define alpha one or the other way.

They generate solid returns because they have identified a way to benefit from taking other risks (in this example liquidity risk). From our experience, those managers who cannot articulate precisely which sorts of risk they take, and why they generate the high returns they do, often revert back to the mean (or worse) in terms of performance.

The reason I bring this up now is that I believe there will be little to gain from taking beta risk in 2017 – in the US or elsewhere. If you wonder why that is, I suggest you read the January Absolute Return Letter again. A decent performance in 2017 is more likely to come from taking other types of risk.

One challenge you will quickly run into is that the vast majority of investment managers with a decent track record take a considerable amount of beta risk along the way. It is certainly the case in the equity long-only space, where all managers take substantial beta risk, but the majority of equity long/short managers are guilty of the same.

This is not a significant issue at Absolute Return Partners, because we almost never invest in plain vanilla equities or bonds, but it certainly is, as far as Blu is concerned. They have built up a lot of experience when it comes to articulating and disseminating the different types of risk for their investment process.

Alpha is by definition a zero sum game before fees. For every underperformer you come across, there will by definition also be somebody who outperforms. When people say that “nobody outperforms anymore”, it is sheer nonsense. If somebody underperforms, somebody else must outperform.

In the early days of the alternative investment industry – back in the 1980s and 1990s – it was possible to pick up a considerable amount of alpha by merely buying and selling the same security on different exchanges. Back in those days many investment bank proprietary desks and hedge funds delivered stellar performance. That has all changed. The amount of alpha generated by alternative investment managers in recent years has been very disappointing, and I think there are at least a couple of reasons for that.

Firstly, there is far more capital chasing the same mis-pricings today, making margins harder to come by and secondly, technology has changed dramatically. Algo-based trading now accounts for a large percentage of total volume on all major exchanges, and inefficiencies are harvested in nanoseconds rather than days or weeks, as we saw back in the golden years. However, alpha will not disappear entirely, so long as markets don’t go up and down in straight lines.

The perception that nobody outperforms these days is probably a combination of two factors – high fees (frequently 2+20 or even worse) combined with the fact that the absolute level of outperformance today is lower than it was years ago. This has caused many to underperform after fees.

And that brings me to the final point on risk factors – how to benefit from gamma risk. Being exposed to gamma risk is about exposing yourself to convex return profiles[2] and not relying on the markets (i.e. beta) to generate returns. Here you have to look for the more qualitative input factors employed.

Gamma risk is present in both liquid and illiquid investment strategies. I mentioned illiquidity earlier as an important gamma factor, but gamma factors can also be employed in the liquid space - volatility being one example. The beauty of gamma risk is that you can turn that risk up or down as you see fit without it affecting your beta exposure.

The biggest opportunities in 2017

Although I don’t plan to say much about the beta opportunity set, I will say one thing. If the Fed is forced to raise the Fed Funds rate more aggressively this year as I suspect it may have to, the best performing stocks in the US will most likely be very different from the winners of the last several years. Most importantly, value stocks would almost certainly outperform growth stocks, but that is likely to be on a relative basis only. On an absolute basis, I am not convinced the US equity market is where you should park most of your money in 2017.

In the alpha space, where we have done a great deal of work in 2016, we are inclined to favour commodities over equities, partly because of the inefficiencies in that market and partly because commodities should react more to a spike in inflationary pressures than equities.

Within the commodity space, there are several opportunities worth mentioning. Oil and gas offer interesting opportunities, and coal should also be an exciting area in 2017, given Trump’s plans to revive the US coal industry. Another growing area within the energy space is electricity trading. It is still relatively under-developed, offering great opportunities to those who have taken the time to fully understand the opportunity set.

In other areas of commodity trading, my long-term favourite is probably agriculture. It caught our attention years ago, as rising living standards across emerging markets continue to drive animal protein consumption to new highs. Our antennas are certainly out for this opportunity.

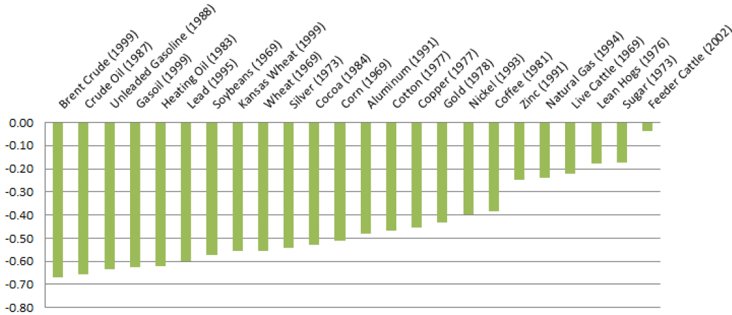

The two biggest risk factors in most commodity markets are probably (a) a global or near-global recession, and (b) a strong US dollar. Most commodity prices are negatively correlated to the US dollar index, and a strong US dollar could therefore hold back commodity prices (exhibit 3).

Exhibit 3: S&P GSCI Commodity Index correlation to US dollar index, 2016-15

Source: Daily Insider, S&P Dow Jones, January 2015

In other words, you don’t want the US economy to do either too well or too poorly. A very strong US economy will most likely result in rising US interest rates, which will drive the US dollar higher, whereas a (near) global recession will lower overall demand for the commodity in question.

That said, weak commodity prices can actually be an advantage, if the investment strategy in question is long/short in nature, which is how we typically approach the asset class. The worst environment for long/short commodity managers is low volatility, and that is not exactly what we expect in 2017.

The gamma space is full of opportunities, and here smaller investors have a huge advantage over the larger ones, but they don’t always take advantage (which is a mystery to me). Because many gamma opportunities are seriously capacity constrained, they are often no-go for the world’s largest investors.

Take the third structural mega-trend I mentioned earlier - the end of the debt super-cycle. That leads to one of our eight structural sub-trends – regulatory arbitrage[3]. One of the investment strategies benefitting from regulatory arbitrage is trade finance. Before the financial crisis, commercial banks were queuing up to provide export finance to EM exporters but not anymore. Export finance is increasingly provided by alternative providers such as trade finance funds, but the market is not (yet) big enough to take capital from the world’s largest investors. It is simply not big enough.

The biggest gamma opportunity of them all is the illiquidity premium. If (near) instant access to your capital is not a must, you can expect significantly higher returns. Even in today’s low return environment, generating double-digit returns is not unheard of, as long as the investment manager has access to your capital for a reasonable amount of time. In order to generate mid-teens annual returns, in our experience, you need to tie up your capital for 5-7 years.

Final remarks

First things first – allow me to make three important points.

Firstly, rules and regulations prevent me from being very product-specific in this forum; hence the Absolute Return Letter you have just read is quite general in nature with no mention of any particular investment products. I know – you would like a bit more ‘juice’, but I have to follow the rules.

Secondly, if your interest has indeed been stirred by what you have just read, you are more than welcome to email us on [email protected], or simply give us a call on +44 20 8939 2900. At Absolute Return Partners we spend a great deal of time looking into how best to pursue investment opportunities that have come up through the macro work I do, much of which has been shared with you over the years in this letter.

Thirdly - and this is really my 30-second slot of commercial time – our Managing Partner Nick Rees will be in Switzerland (mostly Zurich) the week of 13th February and in Brazil, Argentina, Chile and Uruguay between 8th and 16th March. I will be in Denmark myself just before Easter in mid-April, and in the Cologne area in Germany in the first week of May. If you are a family office, pension fund or other financial institution and would like to meet, drop Nick a note on [email protected] or me a note on [email protected].

On that note, there is not much else to say. Some years are obvious ‘beta years’, whereas others are not, and I suspect 2017 may fall into the latter category. Adding to that, you rarely want to take excessive amounts of credit risk when the beta outlook is dim, so that is not the way to go either. 2017 is much more likely to be remembered as a solid alpha and gamma year.

Niels C. Jensen

1 February 2017

©Absolute Return Partners LLP 2017. Registered in England No. OC303480. Authorised and Regulated by the Financial Conduct Authority. Registered Office: 16 Water Lane, Richmond, Surrey, TW9 1TJ, UK.

Important Notice

This material has been prepared by Absolute Return Partners LLP (ARP). ARP is authorised and regulated by the Financial Conduct Authority in the United Kingdom. It is provided for information purposes, is intended for your use only and does not constitute an invitation or offer to subscribe for or purchase any of the products or services mentioned. The information provided is not intended to provide a sufficient basis on which to make an investment decision. Information and opinions presented in this material have been obtained or derived from sources believed by ARP to be reliable, but ARP makes no representation as to their accuracy or completeness. ARP accepts no liability for any loss arising from the use of this material. The results referred to in this document are not a guide to the future performance of ARP. The value of investments can go down as well as up and the implementation of the approach described does not guarantee positive performance. Any reference to potential asset allocation and potential returns do not represent and should not be interpreted as projections.

Absolute Return Partners

Absolute Return Partners LLP is a London based client-driven, alternative investment boutique. We provide independent asset management and investment advisory services globally to institutional investors.

We are a company with a simple mission – delivering superior risk-adjusted returns to our clients. We believe that we can achieve this through a disciplined risk management approach and an investment process based on our open architecture platform.

Our focus is strictly on absolute returns and our thinking, product development, asset allocation and portfolio construction are all driven by a series of long-term macro themes, some of which we express in the Absolute Return Letter.

We have eliminated all conflicts of interest with our transparent business model and we offer flexible solutions, tailored to match specific needs.

We are authorised and regulated by the Financial Conduct Authority in the UK.

[1] For those of you who don’t know who Howard Marks is, he is the co-Chairman of Oaktree Capital Management and a leading light of the investment management industry – a man I respect and admire.

[3] The debt super-cycle, which started in earnest in the first few years after World War II, has led to a dramatic increase in leverage in banks. As the banking regulator forces banks to reduce financial leverage, a rising amount of borrowing takes place away from commercial banks, hence the term regulatory arbitrage.

© Absolute Return Partners LLP 2017