The political upheavals of 2016 caught many by surprise. That in itself is surprising, for the simple truth is that waves of populism are recurring features of economic history. Karl Marx predicted the first breakdown of globalization back in 1848, and Franklin Roosevelt was initially viewed as a very populist president. Today’s collapse of confidence in the political establishment became inevitable once the economic failure of the post- 2008 era was accepted as the “New Normal” and not just a transient phase.

In November, the U.S. electorate delivered a resounding message: Economic growth must be the preeminent priority. Monetarist dogmas are being abandoned in favor of fiscal, trade, regulatory and tax policies that will intervene directly in economic outcomes. While this regime may seem nebulous or precarious compared with its predecessors, the direction of things is clear. Populism has always been associated with reflationary impulses and reflation is good for equities.

For 2017, we expect:

» More upside than downside for equities, with the S&P 500 Index reaching 2400 by early 2018. Drawdowns of more than 5% or levels below 2150 are unlikely. Equities will be driven more by earnings growth than shifts in valuation. Consensus expectations for corporate profits (+11%) are realistic and assume modest recovery in nominal GDP. With tax reform and stronger economies overseas, earnings growth could surprise positively.

» President Trump will aggressively manage the U.S. economy, much like Jack Welch ran General Electric. Like the Chinese leadership, Trump is not afraid to intervene economically to create desired social outcomes. Fiscal stimulus, tax reform, a broad freeze in regulation and reparation of overseas cash will revive the “animal spirits” of which Keynes spoke so fondly. On the other hand, protectionism and immigration policy are risks to watch.

» Against this backdrop of sustained U.S. expansion, the upturn in the eurozone is gaining momentum. Coupled with brisk activity in Germany and Spain, the French economy appears to be emerging from its doldrums. Leading indicators across Europe are consistent with 2% GDP growth and imply this cyclical upswing will become self-sustaining. Politics are a wildcard, but European equities could comfortably outperform their U.S. counterparts in 2017.

» Fed policy is critical. Chair Yellen will remain patient in 2017 but the Fed is likely to over-hike and trigger a slowdown and bear market by mid-2018. Other concerns to monitor include whether U.S. bond yields overshoot on the upside, excessive U.S. dollar strength, and how well the Chinese manage their shift to slower growth.

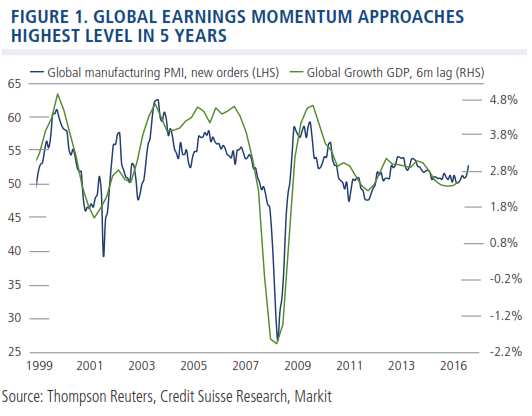

Global headwinds are giving way to flickers of reflation (Figure 1). Fiscal austerity is ending, bank deleveraging is complete, and the decline in oil and gas capital expenditures is over. The emerging economies are bouncing off their lows, supported by stronger PMIs for commodity exporters (Russia and Brazil). U.S. inventories, which were a drag for five quarters, are adding to growth again.

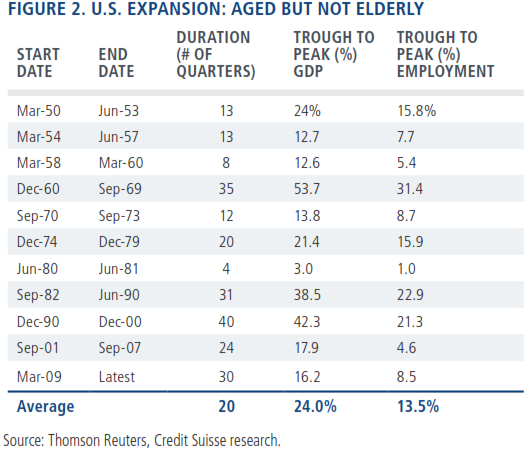

In the pole position, the U.S. economy is emerging from its midcycle slowdown. While the U.S. expansion is “old” in duration, it looks more middle aged in terms of actual fundamental progression (Figure 2). An easing of bank regulations encourages a more normal lending environment, while reflation of the U.S. middle class could transform the U.S. durable cycle. This will shape the remainder of the expansion, which will enjoy cyclical pushback against secular deflation pressures.

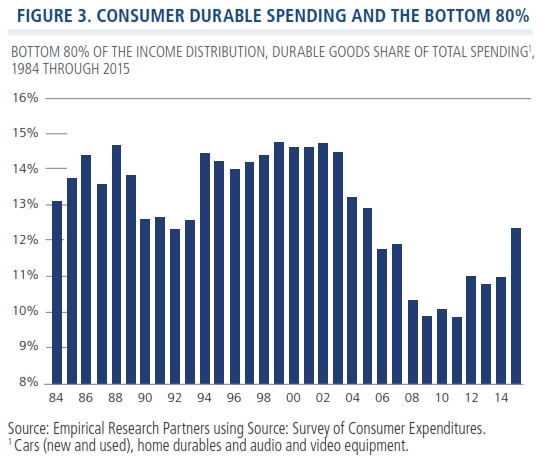

The U.S. consumer appears in lean health on a variety of measures, including free cash flows and home equity as a share of home value. Consumer incomes look healthy, boosted by weak oil prices and low inflation. This sets the stage for a more normal looking recovery in durable spending (Figure 3), which eluded the early years of the expansion.

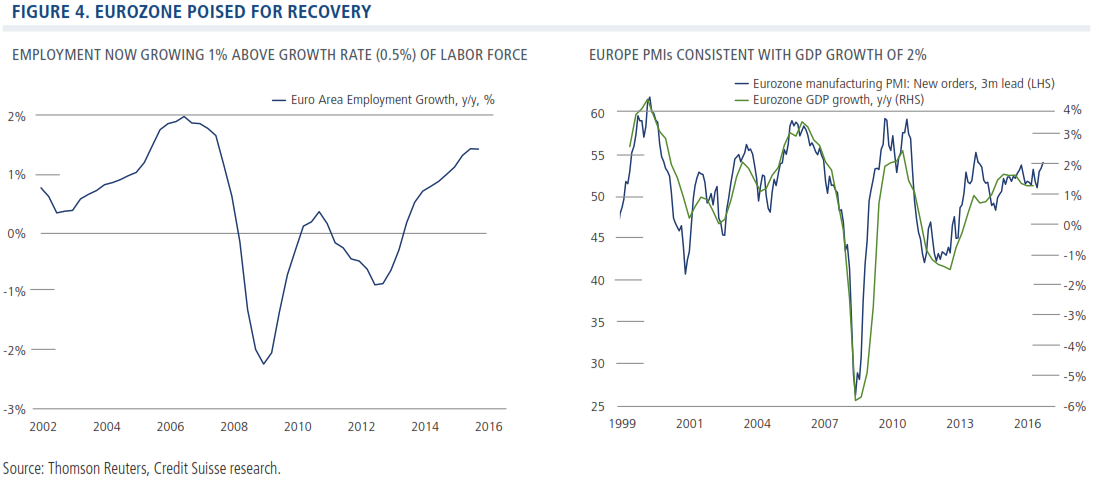

Across the pond, the eurozone is emerging from severe recession (Figure 4) and is poised for positive surprise. Political uncertainty has been the key driver of investor pessimism, but this reflects a rear view of political and economic conditions. Europe’s cyclical upturn is led by pent-up domestic demand, renewal of the bank lending system, export recovery to Russia and China, and a competitive euro. Operating leverage of European companies is high and earnings are particularly sensitive to the global cycle.

China is a source of concern as it transitions to slower secular growth. The politics of trade are more of an issue for 2018, but the post-Cold War “free pass” for China to develop its economy at the expense of the American middle classes is over. As President Trump reinvigorates the U.S. as a destination for investment, we believe China will struggle to adjust its growth model. For global industries that become overly reliant upon Chinese demand, such as commodities, heavy industries and oil, there are few silver linings.

Calamos Phineus Long/Short Fund: Consensus or Contrarian?

In our post-election blog, “Thoughts on the Market in Light of Election Results,” we noted that “populism has been associated historically with reflationary impulses and we believe that is the case today.” From this conclusion flowed the investment case for financials, domestic cyclicals, infrastructure and defense, and we touched upon our more cautious view for health care.

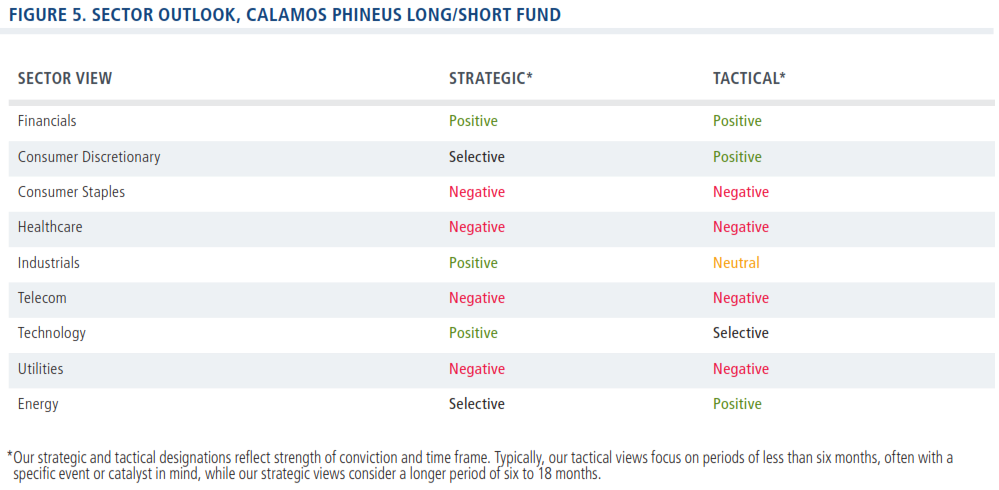

Our view today (Figure 5) is consistent with that framework. Since mid-2016, our positioning has anticipated a gradual reflation of the global economy and thus, we view the financial sector (banks, consumer finance and capital markets) as prime beneficiaries of easing deflation fears. Select consumer cyclicals and industrials that were mistakenly priced for “end of cycle” risk rather than sustained expansion are also compelling.

In energy, our tactical outlook is positive. Saudi leadership will do everything in its power to maintain stable oil prices as it prepares the IPO of Aramco, its national oil business. Longer term, periods of sustained excess return are less likely because U.S. shale has a shorter development cycle, allowing supply to adjust more quickly to higher prices. Also, alternative energy technologies have undermined the long-term value of oil resources, so production restrictions to boost prices are less likely.

We are selective with regard to technology. Market sentiment is near all-time highs and concentrated in a handful of names, which concerns us. We are also avoiding the “safety” stocks (consumer staples, telecoms and utilities) as well as the health care sector as it confronts less growth and more political risk.

Outlook

“There are decades where nothing happens; and there are weeks when decades happen.” —Vladimir Lenin

The reflation move since November has been aggressive but appears more right than wrong. The long cycle of global deleveraging, which hit the U.S. in 2008, swept through Europe in 2012, and washed along the shores of the emerging economies in recent years, has spent its force. Politics rather than economics carried the day in 2016, but this misses a crucial subtlety. The populist revolution emerged just as the global economy was on the mend, which implies President Trump is downright lucky. As Napoleon Bonaparte often noted of his generals, it can be as important to be lucky as to be smart. It is time to think more positively about the global economy.

--

The S&P 500 Index is considered generally representative of the U.S. stock market. Indexes are unmanaged, do not include fees or expenses and are not available for direct investment. Purchasing Managers Indexes (PMIs) measure the strength of the manufacturing sector. Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. The views and strategies described may not be suitable for all investors. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations. The Fund is actively managed and its portfolio is subject to change daily. Alternative investments may not be suitable for all investors, and the risks of alternative investments vary based on the underlying strategies used. Many alternative investments are highly illiquid, meaning that you may not be able to sell your investment when you wish to. An investment in the Fund is subject to risks, and you could lose money on your investment in the Fund There can be no assurance that the Fund(s) will achieve its investment objective. Your investment in the Fund is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. The risks associated with an investment in the Fund can increase during times of significant market volatility. The Fund also has specific principal risks, which are described below. More detailed information regarding these risks can be found in the Fund’s prospectus. The principal risks of investing in the Calamos Phineus Long/Short Fund include: equity securities risk consisting of market prices declining in general, short sale risk consisting of potential for unlimited losses, foreign securities risk, currency risk, geographic concentration risk, other investment companies (including ETFs) risk, derivatives risk, options risk, and leverage risk. Short Sale Risk — The Fund may incur a loss (without limit) as a result of a short sale if the market value of the borrowed security (i.e., the Fund’s short position) increases between the date of the short sale and the date the Fund replaces the security. The Fund may be unable to repurchase the borrowed security at a particular time or at an acceptable price. Leveraging Risk — Leverage is the potential for the Fund to participate in gains and losses on an amount that exceeds the Fund’s investment. Leveraging risk is the risk that certain transactions of the Fund may give rise to leverage, causing the Fund to be more volatile and experience greater losses than if it had not been leveraged. The Fund’s use of short sales and investments in derivatives subject the Fund to leveraging risk. Derivatives Risk — Derivatives are instruments, such as futures, options and forward foreign currency contracts, whose value is derived from that of other assets, rates or indices. The use of derivatives for non-hedging purposes may be considered more speculative than other types of investments. Derivatives can be used for hedging (attempting to reduce risk by offsetting one investment position with another) or non-hedging purposes. Hedging with derivatives may increase expenses, and there is no guarantee that a hedging strategy will work.

Before investing carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information or call 1-800-582-6959. Read it carefully before investing.

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE

This material is distributed for informational purposes only. The information contained herein is based on internal research derived from various sources and does not purport to be statements of all material facts relating to the information mentioned, and while not guaranteed as to the accuracy or completeness, has been obtained from sources we believe to be reliable.

Calamos Financial Services LLC, Distributor 2020 Calamos Court | Naperville, IL 60563-2787 800.582.6959 | www.calamos.com | [email protected] ©2017 Calamos Investments LLC. All Rights Reserved. Calamos® and Calamos Investments are registered trademarks of Calamos Investments LLC.

PLSGHCOM 18166 0117O C

© Calamos Investments

© Calamos Investments

Read more commentaries by Calamos Investments