A stock market wild card in 2017 is the potential for a significant reduction in the corporate tax rate. President-elect Trump’s desire to lower corporate taxes, if implemented, would have multifaceted impacts on businesses. Lowering the corporate tax rate from 35% to as little as the proposed 15% rate would be a historical cut, not only due to the size of reduction, but also because it will be the first corporate tax rate cut since 1988. The ultimate shape and size of corporate tax relief can only be surmised at this point, but we can begin to gauge the impact on corporate earnings using a few simplified assumptions.

Corporate earnings drive stock prices, and a meaningful lowering of tax expense could have a significant impact on EPS growth over the next couple of years. This analysis examines corporate tax expense as represented by the 500 largest U.S. companies, and discusses how—and to what degree—the lower statutory corporate tax rate could impact reported earnings. (In our next report we’ll look at another important piece of Trump’s tax plan: tax on cash repatriated from overseas.)

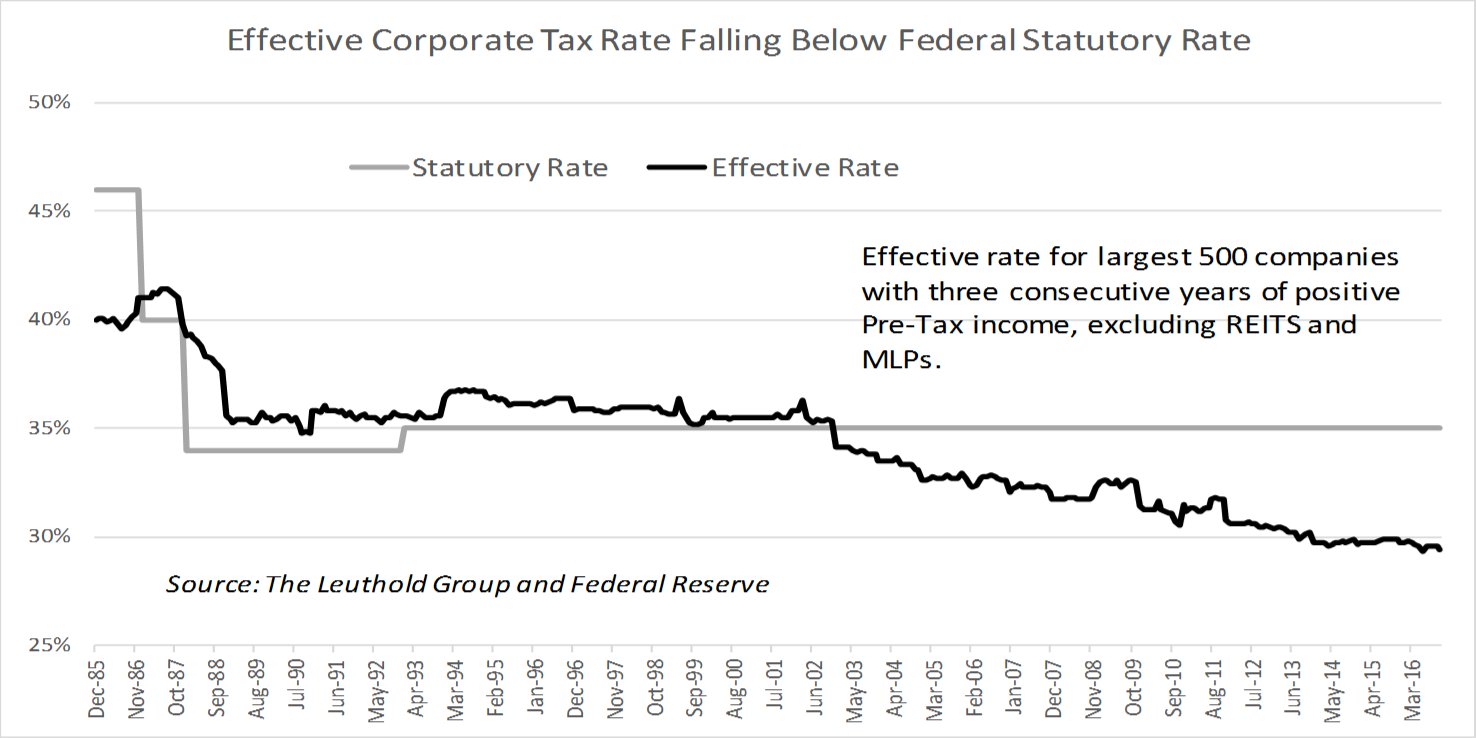

Declining Effective Corporate Tax Rate Is Still Well Above 15%

Chart 1

The U.S. has one of the highest statutory corporate tax rates in the world, yet we find that companies are increasingly using sophisticated tax management schemes to reduce their effective rate (defined as income statement tax expense divided by pre-tax income). A tally of the largest 500 companies with three consecutive years of positive taxable income (excluding REITS and MLPs) finds that indeed the average effective tax rate (including federal and state tax payments) has declined from above 35% in 2002 to 29% currently.

While companies have undercut the statutory rate by six percentage points, tax payments are still well above Trump’s proposed 15% federal tax rate. Assuming an average state tax around 4%, the tax rate including federal and state could be capped at around 19% based on Trump’s most aggressive plan. On average, this reduces companies’ tax rates by one-third. Actual savings, however, will vary.

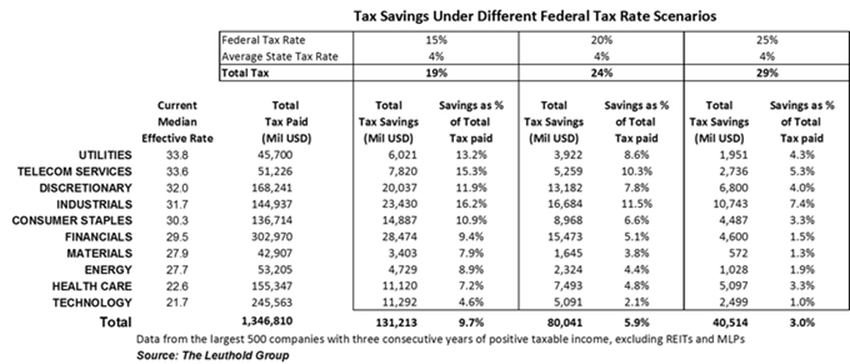

Tax Savings Varies Among Sectors

Companies with high effective tax rates would generally reap the most benefit of Trump’s tax plan. We quantified the difference in tax savings at the company level under three scenarios: assuming a federal rate at 15%, 20%, and 25%, with a flat state tax rate at 4% (the 4% state tax rate is an average; applying it to all companies can give us only a rough calculation). The 500 companies that make up our sample universe experience noticeably different tax savings depending on their sector membership.

Table 1

A dramatic cut in the statutory rate should benefit sectors currently paying the highest effective rate. Table 1 measures this impact by calculating: (1) the total tax paid by sector; (2) the total reduction in tax expense under the three scenarios; and, (3) the scale of this tax reduction as a percent of tax expense. Among the ten sectors, Utilities, Telecom Services, and Consumer Discretionary currently have the highest median effective tax rate. Technology, Health Care, and Energy post the lowest rates.

If the federal rate is lowered to 15%, five sectors including Utilities, Telecom Services, Consumer Discretionary, Industrials, and Consumer Staples will see tax bills lowered by more than 10%. Among them, companies within the Industrials sector lead the way with a 16.2% tax cut on an aggregate level. Across all sectors, a 15% federal tax rate means roughly $130 billion in tax expense savings for these 500 companies.

On the other hand, assuming a 15% federal rate, Technology companies in total can only save 4.6% on tax expenses. Health Care, Energy, and Materials sectors will also have relatively smaller savings. Finding tax-cut winners will clearly require a sector level perspective.

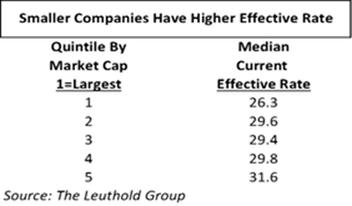

Smaller Companies Benefit More From Lower Tax Rate

Table 2

Table 2 uncovers a size effect, as we find that the largest 100 among these 500 companies have the lowest median effective rate at 26.3%, and the smallest 100 companies have the highest rate at 31.6%.

Among the other three market cap quintiles, the current effective rates are essentially the same. Smaller companies may have less diversified revenue streams in terms of geographic location, and may employ less sophisticated tax shelter strategies than most mega caps do, hence a rate cut should have a more favorable impact on these smaller companies.

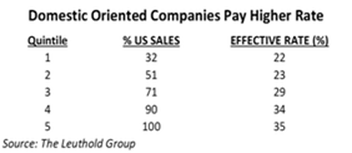

Companies With Domestic-Market Focus Also Benefit More

Table 3

The largest companies are often multi-nationals that have more opportunity to shelter income abroad. (As we know, getting it back home is another question entirely.) We explore this idea by stratifying our 500 companies based on the percent of sales coming from the U.S. as opposed to overseas, then matching that against effective tax rates.

In Table 3, companies are quintiled based on U.S. sales as a percentage of total sales. Those generating all of their sales in the U.S. pay the highest effective tax rate (35% on average), while companies generating the bulk of their sales overseas pay a significantly lower effective rate of 22%. This relationship appears clear and consistent from top to bottom. A rate cut should have an outsized benefit for companies selling primarily to U.S. customers.

Benefit Of Lower Tax Rate Varies Based On Net Deferred Tax Assets/Liabilities

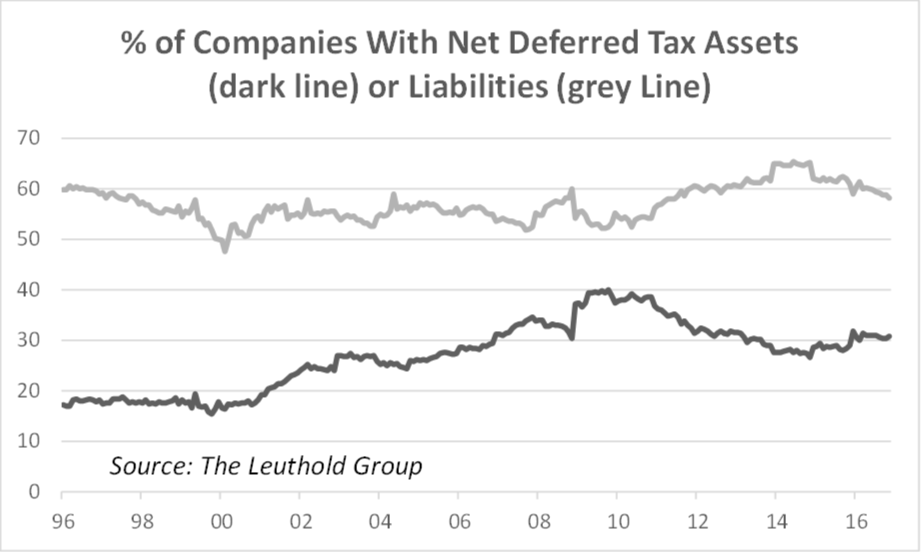

Chart 2

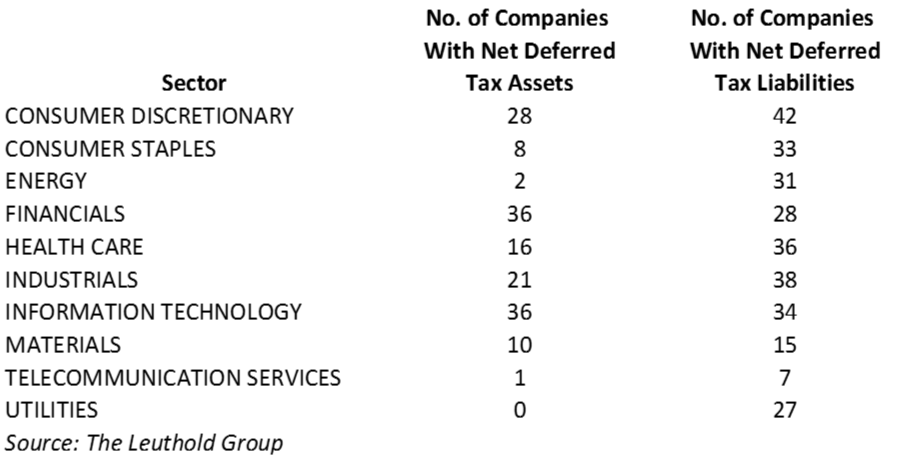

Table 4

The impact on tax expense is the main discussion when analyzing the impact of a changing tax regime. However, change in tax rate can also impact balance sheet items. Depending on whether a company has net deferred tax assets or net deferred tax liabilities, a lower tax rate can be either a positive or a negative.

Deferred tax asset/liability positions are used to record discrepancies in the timing of income and expense recognition for book and tax purposes. The number of discrepancies multiplied by the anticipated tax rate is recorded on the balance sheet. Deferred tax assets can be used to offset future tax payments, and vice versa.

Among the 500 companies we analyzed, the number with net deferred tax assets began to increase in 1996 and peaked out in 2009 (Chart 2). That trend was followed by a steady decrease from 2009 to 2015. Currently, 154 companies have net deferred tax assets to offset future tax payments.

When lower tax rates are anticipated, a company with net deferred tax assets will have to revalue its balance sheet account. Lower tax rates result in a write-down of asset value, which is recorded as a one-time earnings reduction. In contrast, a lower tax rate will have a positive impact on earnings for firms holding net deferred tax liabilities.

Among the ten sectors included in the analysis, only Financials and Technology companies have more net deferred tax assets than net deferred tax liabilities (Table 4). The majority of Telecom and Utilities companies have net deferred tax liabilities, suggesting that these firms will reap a one-time benefit to their bottom lines as they write down their tax liabilities.

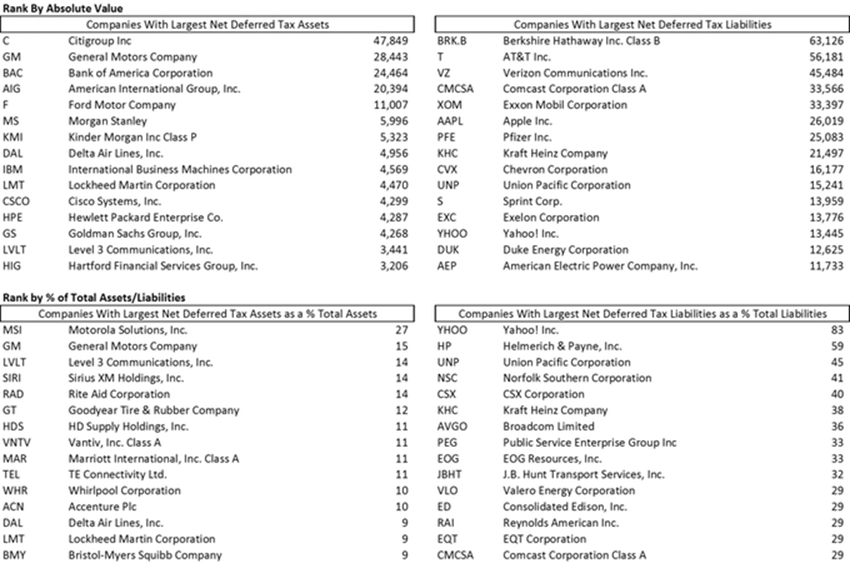

Table 5 lists companies with the largest net deferred tax assets and/or liabilities based on absolute value and as a percentage of total assets or liabilities. Since the impact on earnings is a one-time event for those with net deferred tax assets, investors may discount its effect on results. However, it’s hard to ignore that these companies prepaid tax during a high-tax regime, while those with net deferred tax liabilities are rewarded due to having deferred tax payments to a low tax-rate regime. The readjustment of this balance sheet item results in an increase or decrease of a firm’s value.

Table 5

During a 2004 congressional debate about a potential corporate tax cut, there was a contingent of companies with substantial deferred tax assets which lobbied against such a cut for fear of the one-time hit to earnings. As a result of these companies’ efforts, the American Jobs Creation Act of 2004 did not cut the statutory tax rate, but instead lowered the effective rate for companies through other means. This illustrates that the negative impact of having a large deferred tax asset write-down is true concern for management. Could we see another attempt to circumvent a corporate tax cut under a Trump plan?

Incentive To Delay Or Accelerate Profits May Bring Noise To Earnings

Less transparent than the earnings impact of a deferred tax asset/liability write-down is the incentive for companies to accelerate, or defer, income recognition in response to a coming low tax-rate regime. Companies with a large amount of deferred tax assets have a strong incentive to accelerate income recognition so these assets can be utilized under the high-tax rate environment. For other companies, especially those with net deferred tax liabilities, the incentive is on the opposite end. Management would be inclined to defer income to the lower-rate years. Shifting income across reporting periods was evident in 1986 when statutory corporate tax rates were reduced.

Unlike writing down of deferred tax assets/liabilities that will be recorded as one-time items outside of recurring earnings, discretionary action to accelerate/defer income recognition is not disclosed and could create noise which makes it hard for investors to interpret the earnings trend. For that reason, investors should read between the lines when analyzing earnings around times of tax regime change. We caution against extrapolating revenue and income trends in upcoming quarters as companies attempt to game the various tax proposals on the table.

Conclusion

There is perhaps nothing more important to stock prices than corporate earnings, and there is likely no variable more directly linked to net income than tax rates. Tax expense is a direct reduction of income, and any possibility to lessen that burden is a plus for equities. Trump’s desire to cut corporate taxes is clear, but the details of an ultimate plan may not come for some time. Using simplified assumptions, we formed a preliminary look at how lower taxes may impact earnings. Our research shows that the effects of an across-the-board corporate tax cut would favor certain sectors over others, small caps over mega-caps, and domestically-oriented companies over multi-nationals. Investors interested in conducting more research on the sway of tax policy change can begin with these early signposts and refine their focus as policy specifics begin to emerge and further develop over time.

© 2017 The Leuthold Group

Read more commentaries by The Leuthold Group