When most investors think of diversification, they think about including stocks and bonds in their portfolio, or US and international investments. Fewer investors think about diversifying among investment vehicles — such as active mutual funds, factor-based exchange-traded funds or passive benchmark strategies. But we believe vehicle diversification is a topic that deserves more attention — our research shows that combining different types of strategies can impact a portfolio’s risk and return characteristics, which may meaningfully affect an investor’s long-term investment experience.

Active and passive outperformance moves in cycles

Just as certain sectors like health care or energy can move in and out of favor, so too can active and passive strategies. There are many reasons why. For example, when market conditions are particularly favorable, stocks can get a boost across the board, making it more difficult for active managers to make choices that meaningfully outperform the broad market. On the other hand, when market conditions are rocky, skilled active managers have more of an opportunity to differentiate themselves.

Studying the effects of vehicle diversification

To illustrate the effects of combining vehicles within a portfolio, we recently conducted a study1 examining about 15 years of performance data for three types of strategies:

- Passive. Strategies that seek to replicate a market-cap-weighted benchmark.

- Active. Strategies that are professionally managed to select investments based on the fundamental merits of a company and its stock or bond. We sought to identify active funds that differentiated themselves from their benchmarks.

- Factor-based. Strategies that weight holdings based on measurable investment characteristics such as their history of volatility or their valuation. We utilized factor data from Eugene Fama and Kenneth French, who are widely regarded as pioneers in factor research.

For simplicity, we limited the scope of the analysis to US large-cap equities, although we believe the study can be replicated and extended to additional asset classes. (See footnote 1 for a description of the study’s methodology.)

We studied three different types of combinations:

- Active funds with passive exposure. We evaluated a 50/50 split between actively managed US large-cap mutual funds and the S&P 500 Index.

- Active funds with a combination of factor-based strategies. We paired each active mutual fund in our study with an equally weighted combination of factor strategies (i.e., size, value, quality, momentum and low volatility).

- Active funds with the lowest-correlated factor-based strategies. We paired each active mutual fund in our study with one factor strategy (i.e., size, value, quality, momentum or low volatility). We chose the factor that had the lowest correlation with the fund — meaning that the past performance of the fund and the factor historically not moved in lock-step together.

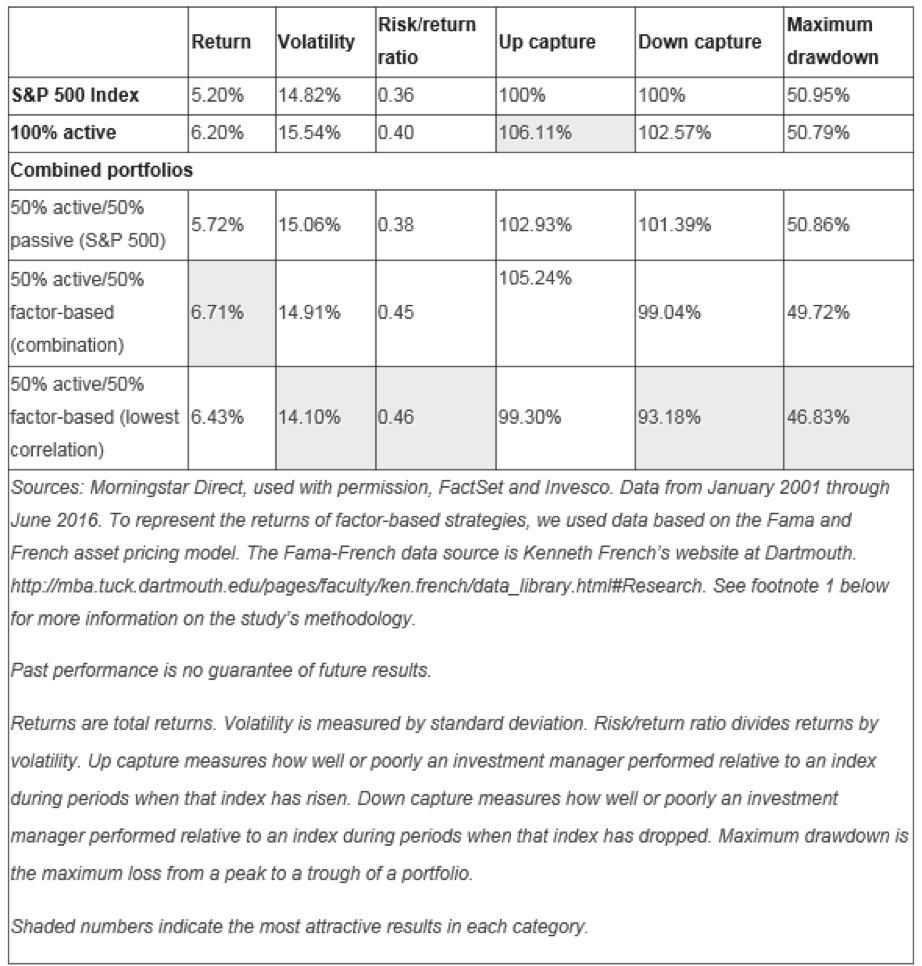

While past performance can’t guarantee future results, our analysis, shown in the table below, shows that diversifying a US large-cap equity portfolio among investment vehicles would have historically boosted risk-adjusted returns and reduced the magnitude of losses as compared with the benchmark S&P 500 Index. Of note, the portfolios that combined active and factor-based strategies resulted in higher total returns and improved risk-adjusted returns versus the S&P 500 Index and the 50/50 active/passive portfolio (illustrated by their higher risk/return ratio).

How we combine investment vehicles

After seeing the results above, the natural question for investors is “How do I combine vehicles in my portfolio?” The easiest way, in our view, is by investing in a strategy that does this work for you. The Invesco Global Solutions Development and Implementation team specializes in constructing high-conviction, multi-asset portfolios. In combining a variety of investment vehicles, our portfolios seek to:

- Diversify among asset classes. Combining actively managed, factor-based and market-cap-weighted strategies could help expand our access to broad asset classes in a way that balances active expertise with cost-effective approaches.

- Manage volatility. Active managers have the potential to deliver higher return, but could carry a disproportional amount of active risk. Passive strategies provide access to markets, but expose investors to broad market risk. Our analysis suggests that pairing such active managers with a factor-based or a passive market-cap-weighted strategy can help reduce volatility without diluting potential return.

- Offset unintended exposure. Active and passive portfolios can sometimes result in unintended market exposures. Supplementing with factor-based portfolios can help balance market exposures.

One example of our multi-asset, multi-vehicle approach is CollegeBound 529. Our comprehensive lineup of college savings portfolios includes active and factor-based approaches; the goal is to outpace the growing cost of higher education in a cost-conscious way.

Conclusion

Over the long term, outperformance has varied among investment vehicles and asset classes. But while many investors already diversify across asset classes, fewer may recognize the potential benefits of diversifying across active, passive and factor-based strategies. We believe that investors need to be prepared for changes in the markets by diversifying across vehicles, and our study shows that blending active and factor-based strategies has resulted in higher risk-adjusted returns compared with the benchmark. There are a variety of ways to implement such a blend, and we encourage investors to talk with their advisors to make sure that their portfolio is tailored to their specific needs and objectives.

1 We gathered performance data, net of fees, for active strategies, passive strategies and factor-based strategies. The data covers monthly returns from January 2001 through June 2016. The investment vehicles are represented as follows:

Passive exposure. We used the returns of the S&P 500 Index as a proxy for the returns of passive strategies.

Active funds. Our initial universe included 1,241 mutual funds represented by US Large Blend, US Large Growth and US Large Value Morningstar categories. We narrowed the universe to create what we believe is a more accurate representation of “active” strategies, by:

- Selecting funds with an available track record of at least three years to account for fund mortality.

- Filtering out top-decile funds (based on three-year performance) to remove performance-chasing, highly risky funds.

- Filtering out bottom-decile funds (based on three-year tracking error) to remove potential benchmark-hugging funds, and including only the most active (top-quintile) of the remaining funds in our sample.

Factor-based strategies. To represent the returns of factor-based strategies, we used data based on the Fama and French asset pricing model for factors including size, value, quality, momentum and low volatility. (See Fama and French, 1993, “Common Risk Factors in the Returns on Stocks and Bonds,” Journal of Financial Economics, and Fama and French, 2014, “A Five-Factor Asset Pricing Model” for a complete description of the factor returns: http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html#Research).

For the purposes of comparison, returns are analyzed net of fees for the representative active funds, net of nine basis points to represent passive strategies, and net of 30 basis points to represent US factor-based strategies.

Duy Nguyen

Portfolio Manager

Chief Investment Officer, Invesco Solutions

Duy Nguyen is a Portfolio Manager and Chief Investment Officer of Invesco Solutions, which provides customized multi-asset investment strategies for institutional and retail clients. In this role, Mr. Nguyen is responsible for the overall strategy and direction of the team’s investment process. This involves guiding the research agenda, overseeing the quality of all portfolio implementation, and communicating the investment process to internal and external teams.

Prior to joining Invesco in 2000, Mr. Nguyen served as assistant vice president and quantitative equity analyst for Van Kampen American Capital, as well as vice president and director of quantitative services of FactSet Research Systems, Inc. Mr. Nguyen regularly lectures for the graduate program at the University of Houston and is part of the Advisory Committee of the Cougar Fund.

Mr. Nguyen earned a BBA at The University of Texas at Austin and an MS degree from the University of Houston. He is a CFA charterholder.

Important information

Blog header image: Stanisic Vladimir/Shutterstock.com

Diversification does not ensure a profit or eliminate the risk of loss.

Correlation is the degree to which two investments have historically moved in relation to each other.

Standard deviation measures a portfolio’s range of total returns and identifies the spread of a portfolio’s short-term fluctuations.

Passively managed index funds generally don’t retain active portfolio managers because they are structured to track an index, whereas actively managed mutual funds seek to outperform their benchmark index and often have higher management fees.

Before investing, consider whether your or the beneficiary’s home state offers any state tax or other benefits that are only available for investments in that state’s qualified tuition program.

For more information about CollegeBound 529, call 877 615 4116 or visit CollegeBound529.com to obtain a Program Description, which includes investment objectives, risks, charges, expenses and other important information; read and consider it carefully before investing. Invesco Distributors, Inc. is the distributor of CollegeBound 529.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC, investment adviser. Invesco PowerShares Capital Management LLC (PowerShares) and Invesco Distributors, Inc., ETF distributor, are indirect, wholly owned subsidiaries of Invesco Ltd.

©2017 Invesco Ltd. All rights reserved.

Active or passive? How investing in both could drive portfolio returns by Invesco