Debt has been a performance enhancing drug for many companies the past several years. Faced with a sluggish economy, CEOs have taken advantage of low interest rates and a favorable fixed income market to raise cash for acquisitions and share buybacks.

For disciplined investors looking to own businesses that can improve results organically without leveraging balance sheets, the “juicing” trend has been particularly frustrating.

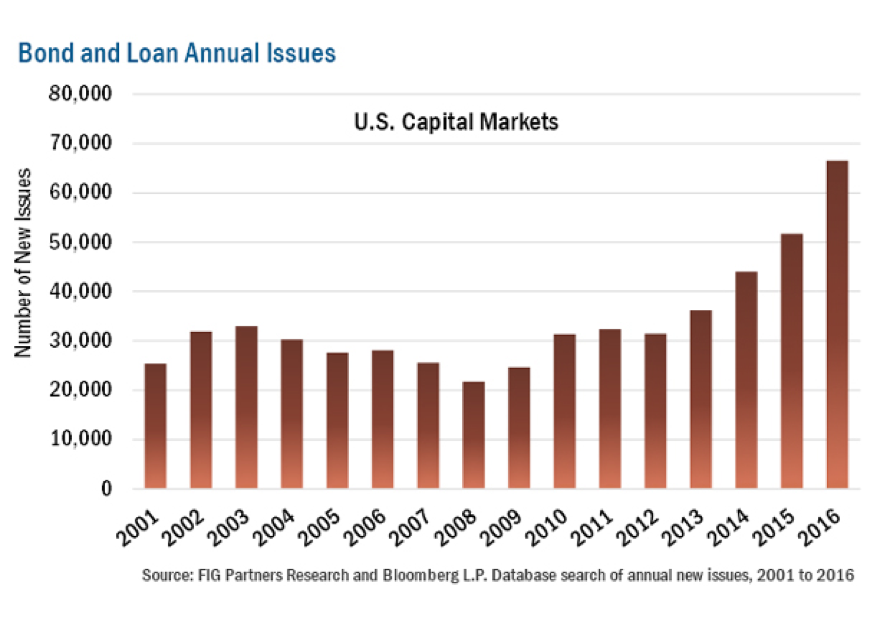

Consider the deterioration in balance sheets during the current bull run. Total debt ratios have remained relatively stable but the use of long-term borrowing has grown. Between March 2009 and the end of 2016, the average long-term debt-to-capital ratio for companies in the Russell 3000® Index has jumped by a third from 33.7% to 44.6%. Abnormally low rates have delayed the sting of borrowing costs, but we believe the era of cheap money is winding down. As costs to service debt rise, the widespread surge in borrowing could be a stumbling block for many businesses.

We understand the temptation for management to use debt in a sluggish economy but also know history hasn’t been forgiving. As the chart shows, borrowing has spiked and a rise in defaults could follow. As a result, we think in the quarters ahead businesses that have been running with clean balance sheets will regain the advantage.

Disclosure:

Past performance does not guarantee future results.

Investing involves risk, including the potential loss of principal. There is no guarantee that a particular investment strategy will be successful. Value investments are subject to the risk that their intrinsic values may not be recognized by the broad market.

The statements and opinions expressed in this article are those of the presenter(s). Any discussion of investments and investment strategies represents the presenter’s views as of the date created and are subject to change without notice. The opinions expressed are for general information only and are not intended to provide specific advice or recommendations for any individual. Any forecasts may not prove to be true.

Economic predictions are based on estimates and are subject to change.

Definitions: Total Debt/Total Capital Ratio: of a stock is calculated by dividing the short- and long-term debt obligations of the company by its total capital, which is represented by the company's debt and shareholders' equity, which includes common stock, preferred stock, minority interest and net debt. Russell 3000® Index: is a market capitalization weighted equity index maintained by the Russell Investment Group that seeks to be a benchmark of the entire U.S. stock market and encompasses the 3,000 largest U.S.-traded stocks, in which the underlying companies are all incorporated in the U.S. All indices are unmanaged. It is not possible to invest directly in an index. Russell Investment Group is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of the Frank Russell Investment Group.

©2017 Heartland Advisors heartlandadvisors.com

2017031

© Heartland Advisors

Read more commentaries by Heartland Advisors