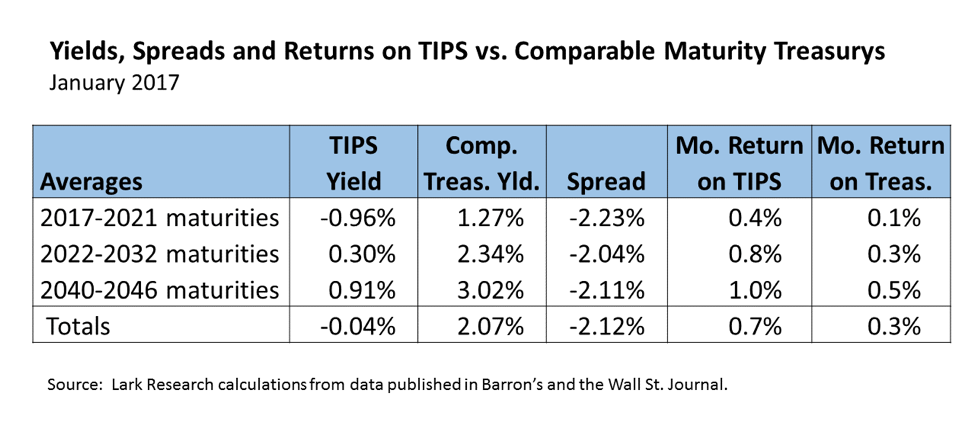

After the run-up in the fourth quarter, both TIPS and comparable maturity Treasurys delivered positive returns during the first month of 2017. According to my estimates, TIPS posted a monthly return of 0.7%, modestly better than the 0.3% return on comparable maturity Treasurys. (By comparison, the S&P 500 earned a total return of 1.8%.)

Investor purchases reduced the average TIPS yield during January from 0.24% to -0.04%, a decline of 28 basis points. The average yield on comparable maturity Treasurys increased by 1 bp to 2.07%. As a result, the TIPS spread increased by about 30 bp to 2.12%.

As is usually the case, longer maturity issues were more volatile, in this case delivering higher total returns, but with less change in average yields than the shorter maturities. The average TIPS-Treasury spread was the highest since early 2014.

At this time, technicals suggest that the odds favor a continuation of the modest rally in Treasury bonds, retracing more of the sharp declines experienced from early November to mid-December. The November-December sell-off in Treasurys was due to expectations of stronger economic growth and rising interest rates. If we do see a bond market rally, I would expect that this would be accompanied by a decline in inflation expectations. Consequently, straight Treasurys should outperform TIPS, possibly bringing the spread back toward its five year average of 180 basis points.

February 7, 2017

Stephen P. Percoco

Lark Research, Inc.