One of the hottest gifts of the recent holiday season was the Amazon Echo, which offers to ease the lives of customers by directing the system with its famous command “Alexa…” This move toward the automation of a greater percentage of our lives has a parallel in the investing world.

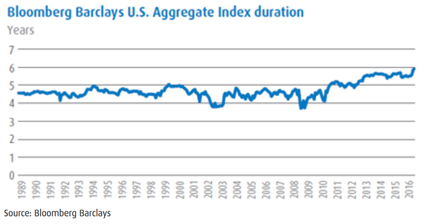

We consider this trend in the wake of the worst quarter for the broad U.S. bond market since 1981. After a nearly 100 basis point rise in Treasury yields resulting in a nearly 3% decline for the quarter, investors are faced with new opportunities and challenges. Between rising expectations of growth and inflation, the broad market yields ended 2016 at their highest level (2.6%) in five years presenting an attractive investment environment. At the same time, benchmark duration has risen to the highest levels (5.9 years) since its inception in 1973 and 30% above the level 10 years ago (4.5 years), which presents new challenges to fixed income investors.

Against this duration and yield backdrop and with the growing trend of automation, we contemplate how the growth of passive investing has impacted not just the individual investors electing a passive approach, but the overall U.S. fixed income landscape. In observing this trend, examining both index construction and the issuance of securities, we find that Treasuries are the fixed income sector most impacted by the growth of passive investing.

Uncle Sam thanks passive investors

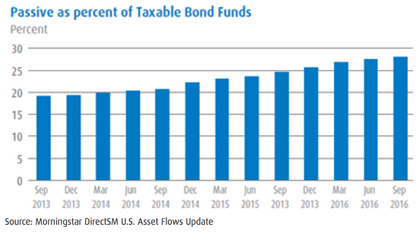

At the end of 2016, the most standard fixed income benchmark, the Bloomberg Barclays Aggregate Bond Index (“Agg”), had a 36% weighting to Treasuries. By contrast, the average allocation to U.S. Treasuries for funds in the Morningstar Intermediate Term Bond category (the largest and broadest taxable bond category) was 18%. Interestingly that category includes passive funds as well, suggesting that generally active managers have less than half the allocation to Treasuries compared to index. That ratio is significant as 90% of flows into the taxable bond category as measured by the Morningstar DirectSM U.S. Asset Flows Update in the past three years have gone into passive funds.

These flows have increased investment in passive fixed income strategies from under 20% of taxable bonds to nearly 30% over that time period. The increase is both large and, with the differential sector allocation, impactful both for the investors making the allocation and the fixed income landscape writ large. As such, it appears that an underappreciated source of support for U.S. rates the past few years has been the increase in passive investing.

Though one cannot necessarily extrapolate from this trend that either the shift towards passive investing or overall flows into the asset class will continue, for each investor making the allocation, the factor risk of rates is higher in a passive approach.

Passive investors prepare to actively fight the Fed

Further examining the impact of the passive trend on Treasuries, we delve in the construction of the index for its treatment of government securities. The rules for inclusion in the Agg exclude “U.S. Treasuries held in the Federal Reserve SOMA” (System Open Market Account). This rule has been in place for a long time, but was designed when the Fed balance sheet was a fraction of its current size and focused on shorter maturity securities. The rule seems logical enough as it removes from the index allocation bonds which the Fed has effectively removed from circulation.

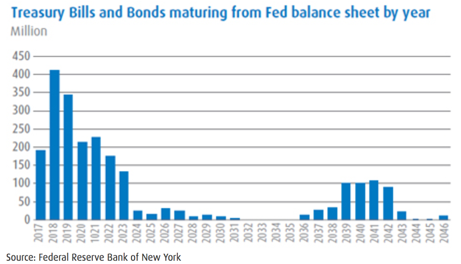

However, as the Fed SOMA has been particularly active since the financial crisis, the amount of Treasury notes and bonds held by the Fed has grown significantly. For context, the entirety of the Treasury allocation in the Agg is $6.75 trillion, meaning that the approximately $2.3 trillion held by the Fed equates a quarter of Treasury notes and bonds (on a notional basis) being excluded from the index. Were those holdings not excluded from the index (or when the Fed eventually eliminates those holdings) the index’s allocation to Treasuries would rise by about 7% to almost 44% of the index. While the support for the securitized sectors is even more dramatic at nearly one third of issuance ($1.8 trillion) of the $5.6 trillion in the Agg held by the Fed, these securities are not removed from the Agg, only from the float-adjusted version of the index.

Further, the Fed has been remitting the interest on its balance sheet, approximately $100 billion a year, to the Treasury department over the last several years. As those securities roll-off and interest payments are no longer collected by the Fed, the Treasury will have a larger deficit to contend with presumably through the issuance of additional Treasuries. And this is before any new fiscal policy and infrastructure projects currently under discussion.

We are not projecting that the Fed will begin eliminating those holdings near term, but at some point they will cease their reinvestment of the maturing principal. When that occurs, the newly available Treasuries will be entering the market and passive investors will be actively allocating a higher percentage to Treasuries, just as the Fed withdraws support from that segment of the market. Contrary to the investment adage of our times, “don’t fight the Fed”, it appears passive investment strategies are set to do just that.

Indices are like a box of chocolate, you never know what you’re gonna get

Similarly, the index’s flexibility on other guidelines opens the possibility of new and perhaps unexpected securities entering the index. For example, with chatter since the election of introducing long-dated Treasuries, the question of the natural buyer for 50-year and 100-year bonds arises. In addition to the two general categories of significant buyers we would normally expect, those in a liability matching programs and yield seekers, we would add another potential buyer: passive investors.

Passive investing in fixed income tends not to mirror index holdings, rather using sampling techniques to emulate the risk factors of the index. Given the somewhat unique nature of these potential long Treasuries, to capture those factor attributes in the passive approach, some combination of these securities may need to be purchased.

As the Treasury has been keen to maintain the liquidity of Treasuries, the start of such a program is not likely to be a one-off event. A built-in and growing buyer base for such issuance may encourage the Treasury to proceed.

In the land of the passive, the one eyed man(ager) is king

In anticipating the Fed’s eventual normalization of policy and decrease in support for markets, we ponder these effects on the market broadly. The trend to passive investing has an underappreciated importance in this scenario given index construction rules.

The addition of Treasuries as the Fed reduces exposure is not necessarily the market call we expect most passive investors are looking to make. Interestingly, the built in buyer for these securities gives the Fed more freedom to withdraw support, knowing that their actions are less disruptive today than prior to the growth of passive investing. Should the trend towards passive investing continue or accelerate, the Fed’s ability to offload securities to those not necessarily seeking that exposure strengthens.

The biggest paradox of all then, is that the Fed and active bond investors may benefit from the trend to passive investing. Passive investors may cushion the blow for other fixed income investors, purchasing more securities as they are released into the market, providing an unexpected buyer whose absence might otherwise have led to a more rapid increase in rates. This buying by passive investors could aid the orderly wind down of the Fed balance sheet, while those seeking to eschew an active market call through index exposure may stand against the Fed.

Alexa, conclude

The phenomenon of passive investing in fixed income has had and continues to have a significant impact on the overall landscape for the bond market. This impact goes beyond the individual investors electing passive strategies and touches on some of the most central issues in fixed income today.

With the continued increase in benchmark duration, new securities potentially being introduced into the market and the eventual wind down of the Fed balance sheet lingering, questions regarding bond market positioning become more poignant. Addressing these questions requires nimbleness, creativity and expertise.

“Alexa, how do I navigate this fixed income landscape?”

Alexa: “Sorry, I don’t know the answer to your question.”

© BMO Financial Asset Management