Key Points

▪ Stock prices continue to rally as economic data improve and investors remain optimistic about the political backdrop.

▪ We think this optimism may be overdone and markets could be vulnerable to disappointments.

▪ Nevertheless, we have a constructive view toward equities and think a pro-growth investment stance is warranted.

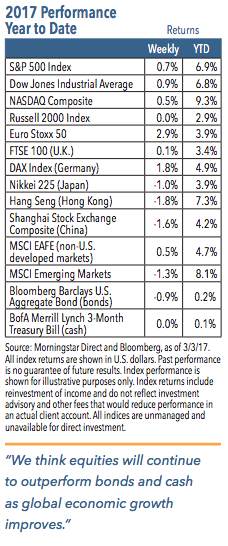

U.S. equities advanced yet again last week with the S&P 500 Index climbing 0.7%.1 Economic data continued to come in better than expected. Consumer confidence reached its highest level since 2001 last month2 while the ISM non-manufacturing index, which measures business activity and employment trends, showed its strongest reading since late 2015.3 As economic data improve, the Federal Reserve indicated a higher likelihood of an interest rate increase later this month.

Potential Risks to Equities:

In lieu of our regular investment themes, we examine five possible market risks:

1. U.S. Politics: Despite growing signs of disunity between President Trump and the GOP Congress, investors still appear optimistic about prospects for pro-growth economic policies. However, we expect investors may lose patience if specifics about issues such as tax policy and health care reform are not forthcoming.

2. European Politics: Perceived risks in Europe have faded as Marine Le Pen’s standing in the French polls has dropped. But the rise of such nationalist candidates may pose a risk to economic growth and equity markets.

3. Earnings: Corporate earnings have improved over the past couple of quarters, but forward-looking expectations may be too high. Consensus expectations are for a double-digit advance in earnings growth for 2017.4 That level will be difficult to achieve, especially since profit margins remain under pressure.

4. Economic Growth: We have seen an almost uninterrupted string of positive growth surprises in the U.S. economy over the past several months. We don’t expect growth to slow, but more bumps are likely in the coming months.

5. The Fed: Investors have largely shrugged off prospects for higher rates, but rising rates could eventually dampen equity market momentum. Additionally, we see a great deal of uncertainty surrounding who Donald Trump will nominate to the Federal Reserve Board of Governors.

Modest Global Economic Growth Favors Risk Assets

For much of this decade, global economic growth has been relatively soft and desynchronized between regions. Over the past nine months, however, economic data has generally improved in most markets simultaneously. Not surprisingly, this has coincided with a strong rally in equities and other risk assets.

We expect economies to diverge slightly over time, but the global economy should continue to improve. In the United States, the expansion is old in terms of years, although we see few signs of stress that would signal a coming recession. We could see additional acceleration if pro-growth political policies come to fruition. China continues to be an important engine of global growth, especially for commodityproducing nations. Chinese growth is likely to fade, however, due to policies designed to shift the economy to be more domestically focused. The eurozone is in an early stage of economic expansion, as Europe emerges from its debt-fueled recession. But Europe still faces political risks and structural problems.

On balance, we have a constructive view toward the global economy and believe it is moving from a deflationary to reflationary phase. The rebound in inflation since mid-2016 has pushed global bond yields higher and contributed to a dramatic shift in equity market leadership from defensive sectors to cyclical areas.4 We expect these trends will persist, which leads us to favor risk assets from a portfolio construction perspective.

At the same time, we believe equity markets may be ahead of themselves. The pace of the current rally is not sustainable and investors may be overly optimistic about the political, economic and earnings environment. As such, we think a pullback or correction is possible at some point. Over the intermediate and long-term, we think equities will continue to outperform bonds and cash as global economic growth improves.

1 Source: Morningstar Direct, as of 3/3/17

2 Source: Conference Board

3 Source: Institute for Supply Management

4 Source: FactSet

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. The Dow Jones Industrial Average is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the Nasdaq. The Nasdaq Composite is a stock market index of the common stocks and similar securities listed on the NASDAQ stock market. The Russell 2000 Index measures the performance approximately 2,000 small cap companies in the Russell 3000 Index, which is made up of 3,000 of the biggest U.S. stocks. Euro Stoxx 50 is an index of 50 of the largest and most liquid stocks of companies in the eurozone.FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. MSCI EAFE Index is a free float-adjusted market capitalization weighted index designed to measure developed market equity performance, excluding the U.S. and Canada. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. Bloomberg Barclays U.S. Aggregate Bond Index covers the U.S. investment grade fixed rate bond market. The BofA Merrill Lynch 3-Month U.S. Treasury Bill Index is an unmanaged market index of U.S. Treasury securities maturing in 90 days that assumes reinvestment of all income.

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy or sell securities, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors.

A WORD ON RISK

This information represents the opinion of Nuveen Asset Management, LLC and is not intended to be a forecast of future events and this is no guarantee of any future result. Information was obtained from third party sources which we believe to be reliable but are not guaranteed as to their accuracy or completeness. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Non-investment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

CFA® and Chartered Financial Analyst® are registered trademarks owned by CFA Institute. Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

© 2017 Nuveen Investments, Inc. All rights reserved.

Read more commentaries by Nuveen Asset Management