After another soft start to the year, the U.S. dollar has been strengthening in recent months. Increasing confidence in a less tentative Federal Reserve (Fed), coupled with higher interest rates, has pushed the dollar up roughly 2.5% from its February low (source: Bloomberg). To the extent the Fed is hiking more aggressively in an environment in which the Bank of Japan (BOF) and, potentially, the European Central Bank (ECB) remain in an easing mode, the dollar is likely to continue to find support.

A cheaper euro or yen provides a lift to Europe and Japan, which in general are more export driven than the more domestically oriented U.S. economy. The challenge is that what the dollar gives, it also takes away. Although European or Japanese companies become more competitive, for dollar-based investors the returns to these markets are reduced to the extent that the dollar rises against the euro and the yen.

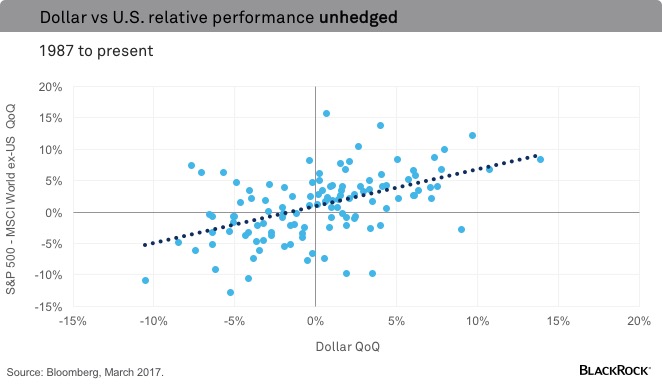

Looking back on the last 20 years, this effect can be quite powerful. Take the relationship between U.S. and non-U.S. equity returns. For the U.S. I used the S&P 500, and for international developed markets, the MSCI World ex-U.S. Index. During the past 20 years, despite the headwind from a stronger dollar, U.S. equity markets outperform when the dollar is rising. The reason? When the dollar is rising, it boosts the return of the S&P 500 against the return from international markets that are denominated in euro, yen and other currencies. See the chart below.

This relationship is particularly strong during periods of market volatility, when the dollar is often appreciating the fastest. During these periods, not only is the dollar rising against most international currencies, but the U.S. is also outperforming as it is viewed as a relative ”safe harbor” compared to other markets. A good illustration of this phenomenon was the third quarter of 2008. The dollar, measured by the DXY Index, surged nearly 10% on panic buying. At the same time, while the U.S. market got hit, it still significantly outperformed the MSCI World ex-U.S. Index as investors sought the relative safety of U.S. assets.

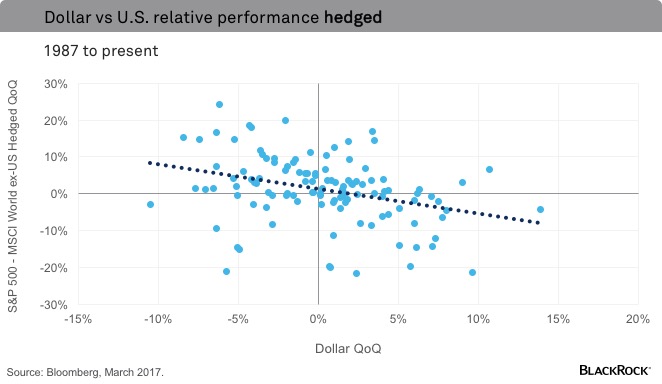

The dollar and U.S. relative performance often move together during times of stress. However, under more normal market conditions a rising dollar can actually provide a bigger boost to international markets, if your currency exposure is hedged. Looking back over the past 20 years, the relationship between quarterly changes in the U.S. Dollar Index and the relative performance of the S&P 500 versus other developed markets inverts when the foreign currency component is hedged back to dollars. Under this strategy, the MSCI World ex-U.S. Index actually tends to outperform the S&P 500 when the dollar is appreciating. See the chart below.

The lesson for investors is this: Although overseas markets offer opportunities, the currency effect can dominate, particularly in a rising dollar environment. Investors looking to take advantage of a stronger dollar by investing abroad should consider strategies that hedge at least some of the non-dollar exposure. In the absence of a hedge, betting against an appreciating currency may not be the best strategy.

Russ Koesterich, CFA, is Portfolio Manager for BlackRock’s Global Allocation team and is a regular contributor to The Blog.