“No amount of sophistication is going to allay the fact that all your knowledge is about the past and all your decisions are about the future.”

-Ian Wilson (1923-2014) Former Executive, General Electric

While it might sound obvious, we find it important to remember that knowing about the past only helps you place bets on the future to the extent that the future is like the past. People often make the assumption that the future will be like the past without even realizing it, but sometimes it just isn’t so. A great deal of the art of investing lies in recognizing when events are repeating previous patterns and when things truly are different.

We do not know for how long yesterday’s favorable conditions will extend into tomorrow. We do not expect many more years of breakneck wealth creation. We often think in terms of both the stock market and the economy as following a familiar cycle. Are we in the “high” part of the economic/market cycle?

- Consumer confidence is at a 16-year high.

- Small business confidence is at a 12-year high.

- Stock market volatility is ultra-low. We recently had more than 100 days without a single one percent down day.

- Fully one-third of small public companies lost money last year and no one seems to care (earnings before interest and taxes among Russell 2000 Index companies)1.

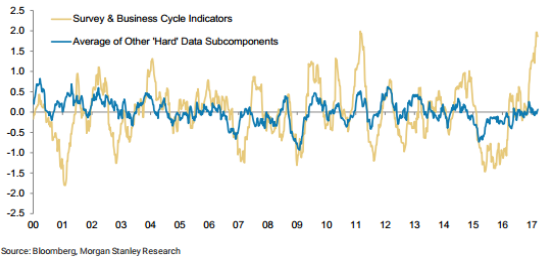

- “Soft” economic data has been a lot stronger than “hard” data. This means that “soft data” which include surveys of consumers and producers about what they think is happening or about to happen, has been a lot stronger than “hard” data, which are direct measurements of some economic reality.

The final point is worth exploring. Models which use a lot of “soft” data are predicting GDP growth of 3% for the first quarter, while those restricted to hard data are predicting less than 1%; this is a huge difference. Sentiment has gotten ahead of reported economic reality; that much is clear. The question is whether (this time) sentiment is a leading indicator (meaning the hard data will follow) or is it a false flag (meaning expectations are over-hyped)?

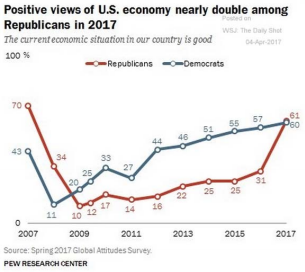

The following chart makes us wonder how much of the improvement in soft data is politically related, and therefore perhaps less a reflection of current conditions on the ground. However, even if the economic confidence doesn’t reflect current conditions, such confidence can have a self-fulfilling effect on economic activity and shouldn’t be completely dismissed. Time will tell. If expectations prove overhyped, and aren’t followed by strong reported economic data, the stock market could stagnate or bleed lower. If the soft data is indeed a leading indicator and robust economic activity follows... will it be enough to exceed the already high expectations and push the market higher?

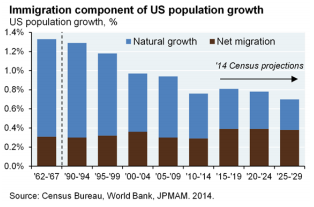

One fact that tempers our economic expectations and which many seem to ignore is that a major portion of GDP growth comes directly from population growth. As the below census data illustrates, population growth has been slowing for some time, with net migration representing half the total. Politics is unlikely to change this in a positive direction unless we start letting in more immigrants. We don’t think that’s very likely. For this reason alone, achieving a vaunted 4% real GDP growth rate will be an uphill battle.

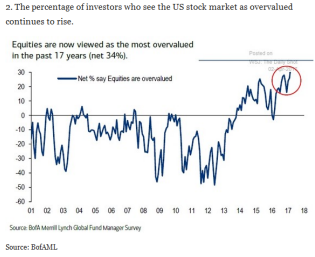

Pondering equity market valuation for a moment, we have seen a bevy of articles describing the current market as the most expensive in history, outside of the roaring 20’s and the dot-com period. A recent Wall Street survey (chart atop next page) captures the rising number of fund managers who believe the stock market is overvalued. We would like to hit back against this view a bit, not least because, in trying to be contrarian, if everyone else thinks the market is expensive, that’s probably a sign that we should be thinking the opposite! As we have said before, stocks are indeed highly valued, but that doesn’t necessarily mean they are overvalued. For one thing, valuation doesn’t necessarily have to mean revert over time. Indeed, equities have maintained a historically high valuation regime since the 90’s.

The big reason for justifiably high equity valuation is (we believe) the low interest rate environment. But the changes in valuation levels over the breadth of history cannot be explained by rates alone (both rates and valuations were low in the 50’s). We recently heard some very interesting and convincing arguments as to why things may have changed2:

Individual stocks are extremely risky, but this can be mollified to a great deal by diversification. With the proliferation of first mutual funds, and later index funds, and now ETFs, it is a lot easier to diversify than it was in the past, which makes investing in stocks less risky. People will pay a higher price for things which are less risky as an asset class.

Today we have a lot more market history than people had in previous decades, which helps inform us that stock fundamentals in aggregate improve over time, and are not as risky as people perhaps thought in the past.

Because of this history, people are much more generally aware of the message that investors will do fine as long as they hold stocks for the long run, as long as they don’t sell them in a panic. This leads to a “network of confidence” where people don’t panic because they don’t expect others to do so. This supports valuations.

As we saw in the 2008 crisis, modern governments are much more inclined than in previous decades to intervene to support markets in a crisis, rather than stand by and scold the imprudent while markets and the economy collapse. This also helps maintain that network of confidence that supports valuations.

Finally, last but not least, investor protections have increased markedly over the decades, which rightfully lead people to have more faith in public companies. If you think modern corporations are a cesspool of greed and misrepresentation, recall that prior to the aftermath of the 1929 crash, insider trading wasn’t even prohibited.

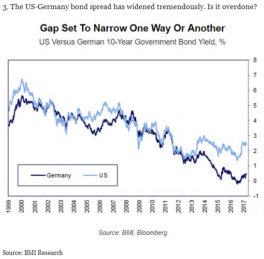

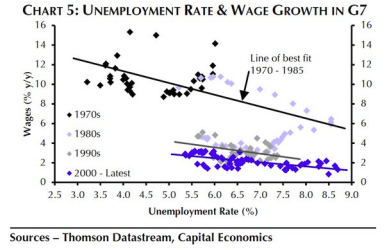

We view current equity valuation as a cautionary yellow light, not a red flag. Valuation is not so much a worry as long as interest rates remain contained. We do see rates going up, but there are important reasons that we suspect such upward movement will be limited in magnitude. First, the long-term interest rates which matter more for the stock market are generally set by the market and only indirectly subject to the Fed’s actions. Second, U.S. rates are already higher than those found in many countries (as compared to Germany for example, at right), which matters in today’s world of global capital flows. Third, there appears to be something, which we have taken to calling “the mysterious global force” pushing down both inflation and rates over time. One way to see this phenomenon is to view the changes in the Phillips Curve, which is a plot of unemployment and inflation3. Not only has the curve moved down in recent decades (lower inflation for a given level of unemployment), but even within the most recent decades, declining unemployment has failed to spark much inflation at all (inflation would in turn cause rates to rise).

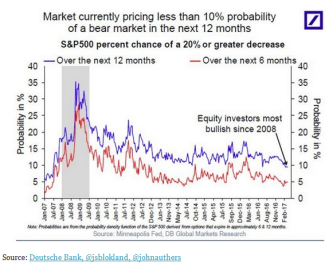

Our biggest investment worry is not valuation, but rather recession... principally so because no one else is worried about this possibility! For example, it is possible to observe the price investors are paying to hedge downside market risk. By this measure, fear of a large drop in the markets is at a post-crisis low. To us this is crazy and the opposite of what should be the case. The chances of a large decline increase, not decrease as markets extend higher and further from the 2008 financial crisis and Great Recession.

As we wrote in the last quarter’s letter, we have been working on positioning our investment portfolios for the day the waters roughen. So far it has worked out well that we made some adjustments to “fade the Trump trade”. In fact, it appears we should have done so more aggressively, as areas of post-election strength have lately reversed meaningfully. The process of positioning the portfolio more defensively is one we call “turning the battleship”. As the name indicates, this process takes time (we aren’t done), and we are ok with that. We know we will not call the top of the market and so prefer a slow and deliberate process that allows us to reduce exposure as time goes on and (usually) risk increases. We also attempt to select good specific replacement securities and that takes time. Lastly, despite a defensive bent we don’t immediately run to large quantities of cash, as we remember that corporate profits generally rise over time and generally take the stock market along.

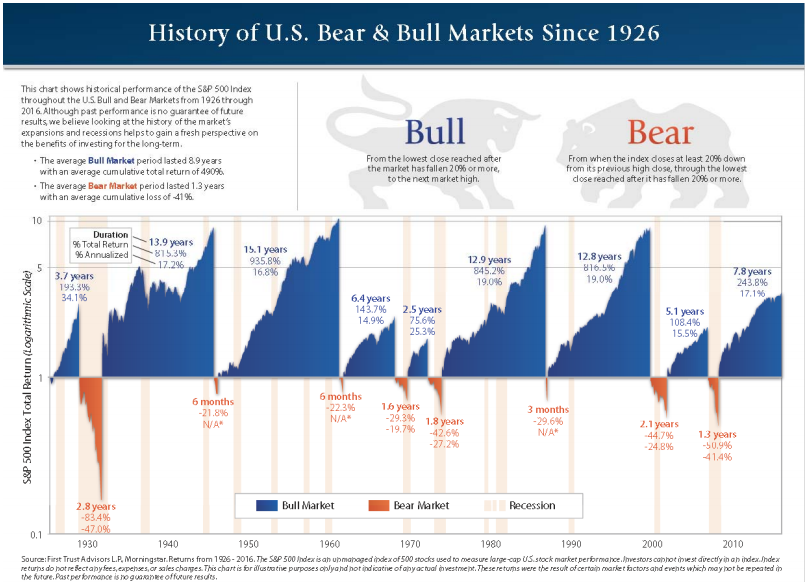

Even if and when we have finally “turned the battleship” to be more defensive, there can never be any guarantee that the stock market won’t drop 50% at any time4. Such 50% declines are stomach-churning, yet they are part of the game and we must expect them (and try to mitigate them as well). Fortunately, though somewhat inevitable, they are tolerable. Why? Because, as we wrote earlier, history indicates that these drops are temporary. We therefore must be prepared not to sell in panic and work to get you and your portfolios through with reduced damage when the time comes. With proper defensive positioning, we will have “dry powder” available to unleash on the markets as they recover. But even with proper positioning, it will hurt when the storm breaks, as we must remind ourselves during the good times.

One might ask why sign up for stock market exposure when one knows their investment may be periodically sawed in half? Why take such risk? Well, because there is another kind of risk: the “risk” that you won’t have gained much at the end of your investment horizon. Viewed this way, over any reasonably long time horizon cash is a much “riskier” investment than stocks! These days, with cash, you’re almost guaranteed to end up with less spending power than you started with. It is really only with relatively short time horizons that stocks have this kind of risk as well. Clients who expect to spend a considerable portion of their account values within the next few years should talk to us about having us shift a portion of their account to fixed income (i.e. bonds), which we will happily do.

This past quarter we sold a portion of our stock in Bank of America (BAC). The initial purchase, in February of 2009 at less than $5 per share, is a good example of how we endeavor to take advantage of market dislocations, in this case deploying some cash reserves near the end of the financial crisis. While we now wanted to take some profits, we did not sell highly-appreciated BAC shares in taxable accounts because it would have triggered a substantial tax bill. We took similar action with Science Applications International Corp. (SAIC) when we sold all our shares except those that were highly appreciated in taxable accounts. In certain cases we believe that the value of delaying the capital gains tax bill for 10 or 20 years (or perhaps forever in the case of inheritance) can outweigh the advantage of getting into a stock with better near-term potential. We only take this approach with quality companies that we expect to be sufficiently profitable over the longer-term that we would be happy to own forever. This represents one of the ways we try to think in terms of after-tax results even though we, along with most any advisor we can think of, only report before-tax results. Any advantages we achieve in this area will not appear on your statements (but should benefit you anyway). Because we are maintaining our SAIC (and partly BAC) positions primarily for tax, not investment reasons, we suggest that any of our clients intending to make charitable gifts consider doing so with BAC or SAIC shares instead of cash. The charity will receive the full value of the shares and any embedded capital gains tax will be avoided entirely.

During the past quarter we purchased shares of Wells Fargo preferred stock. While it remains to be seen if this investment will be a winner, we believe it enabled us to reduce some economic risk in your portfolio while earning substantially more after-tax income compared with holding cash. In general we are not big fans of fixed-income securities (i.e. bonds and preferred issues) unless there is a need to spend the money soon, as noted above. However, this particular Wells Fargo security appears to be mispriced. It does not contain the customary issuer’s call option which can only work against the investor, and yet it yields more than similar preferred stocks also issued by Wells Fargo, which do have the detrimental call provision. This investment isn’t a sure-thing-winner (none are); we will lose money if interest rates go up substantially. However, if we go into a recession, this investment should hold its value relatively well and can be a source of funds to hopefully buy other stocks at a bargain. More importantly, if what nobody expects to happen, happens, and interest rates (gasp!) drop, then we stand to make a great deal of money in capital appreciation on top of the six and one tenth percent dividend yield. Again reflecting on your after-tax results, because this yield comes in dividend as opposed to bond coupon form, it is taxed at a lower rate for higher tax bracket earners. For denizens of the highest tax bracket, this payout is equivalent to earning 8% interest on a regular corporate bond.

Ending this letter where it began, while we know the future is unknowable, we are working hard to be prepared for ways in which it might differ from the past. One thing we don’t expect to change is the general upward direction of the market, as the chart we append at the end of this letter indicates.

Please note, after 20 years in our current location, we are moving to another building in Fashion Island: 500 Newport Center Drive, Suite 680. Please come by and see us sometime. We would welcome the opportunity to talk to you about your investments and how we might be able to help. While our expertise is in stocks, we are happy to attempt to be of service in any financial area.

Sincerely,

John G. Prichard

Miles E. Yourman

1 We will note that all Knightsbridge holdings made a profit last year, with the exception of AIG, which booked a large loss when boosting reserves last quarter.

2 We are indebted to an article, “Diversification, Adaptation, and Stock Market Valuation” posted on www.philosophicaleconomics.com which got us thinking about the above points. We encourage you to read the post in its entirety.

3 The specific graph below plots unemployment versus wage growth, which is used as a proxy for inflation.

4 You can see this on the excellent chart of bull and bear markets at the end of the letter.

Past performance is not indicative of future results. The above information is based on internal research derived from various sources and does not purport to be a statement of all material facts relating to the information and markets mentioned. It should not be construed that the information in this commentary is a recommendation to purchase or sell any securities. Opinions expressed herein are subject to change without notice.

© Knightsbridge Asset Management, LLC

Read more commentaries by Knightsbridge Asset Management