Talking about the housing market always evokes a strong, and often emotional, reaction. This is usually because the powerful vested interests (owners, investors, speculators, politicians, lenders, real estate agents and other intermediaries) can’t bear to think of the consequences of a decline in house prices. In the case of politicians, this is ironic because they constantly talk about making housing more “affordable” but, by definition, this means lower prices.

It has been a few short years since the onset of a nation-wide fall in house prices in the United States precipitated the greatest and most troubling global economic slump since the 1930s. The massive debt accumulation and creative use of derivatives meant that housing was the epicenter of a debt crisis that only moderated after governments around the world threw more debt into the pot and assumed or guaranteed many of the losses of the private sector. Global banking rode to the edge of the precipice and literally teetered on the edge. Many banks were only saved from failure after governments took control by spending taxpayer funds. This remains the case today with several high profile banks.

In this modern world should we not be surprised that “sophisticated” bankers with all sorts of tools at their disposal can get it so wrong that they can send the entire world into a recessionary tailspin? Could it happen again?

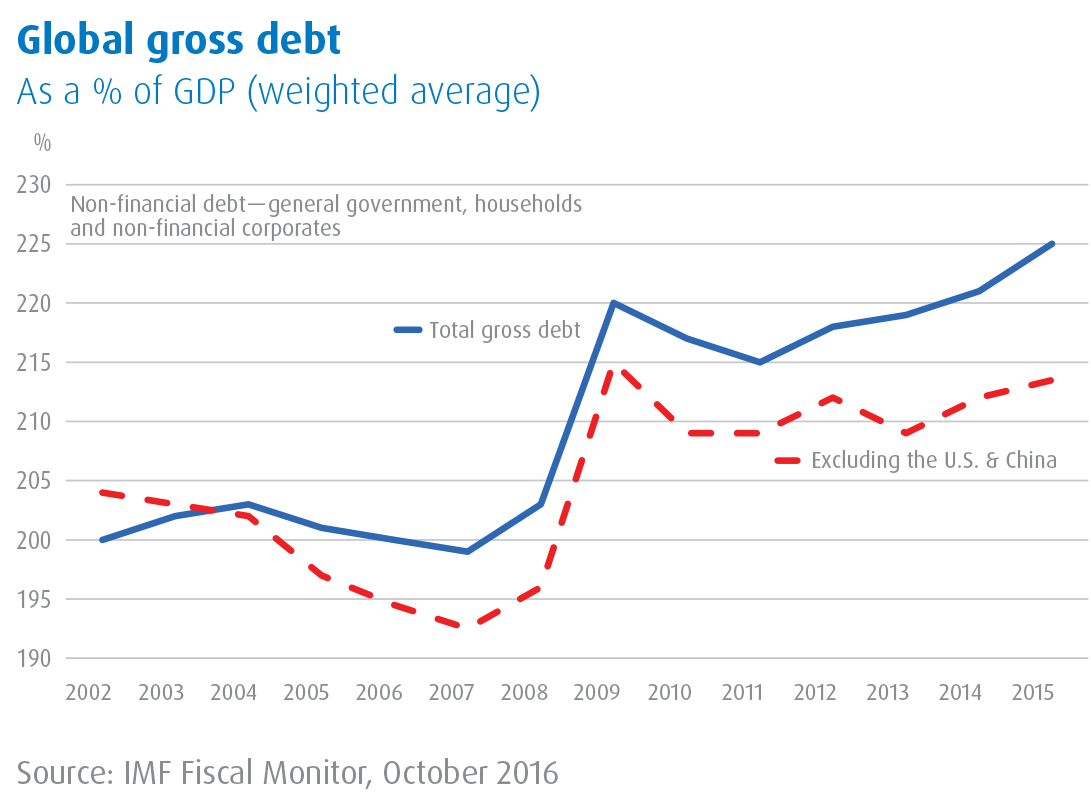

The thing that troubles us most is that global debt, relative to GDP, is now higher than at the onset of the financial crisis. To be sure, the debt has been shuffled about with a marginally higher proportion in the hands of government than previously, but this gives us little comfort.

Debt is debt and one way or another it has to be paid back or forgiven. If the latter, it is implied that it is possible to find sufficient lenders prepared to take a sizeable hit to their viability to enable order and balance to be restored. This strikes us as unlikely. If the former it implies that the world can grow faster than the rate of debt accumulation for an extended period. This strikes us as improbable — particularly when one takes into account the economic history of the post-1970s era. This is when financial deregulation got underway in earnest and the accumulation of debt became easy and commonplace.

It is a sad but true fact that housing is once again pushing the boundaries of debt and economic common-sense. Animal spirits are running hard in many markets and the mere mention of the possibility of a fall in house prices is considered to be the imaginings of a lunatic. It’s just one more sobriquet to be proudly earned by Pyrford.

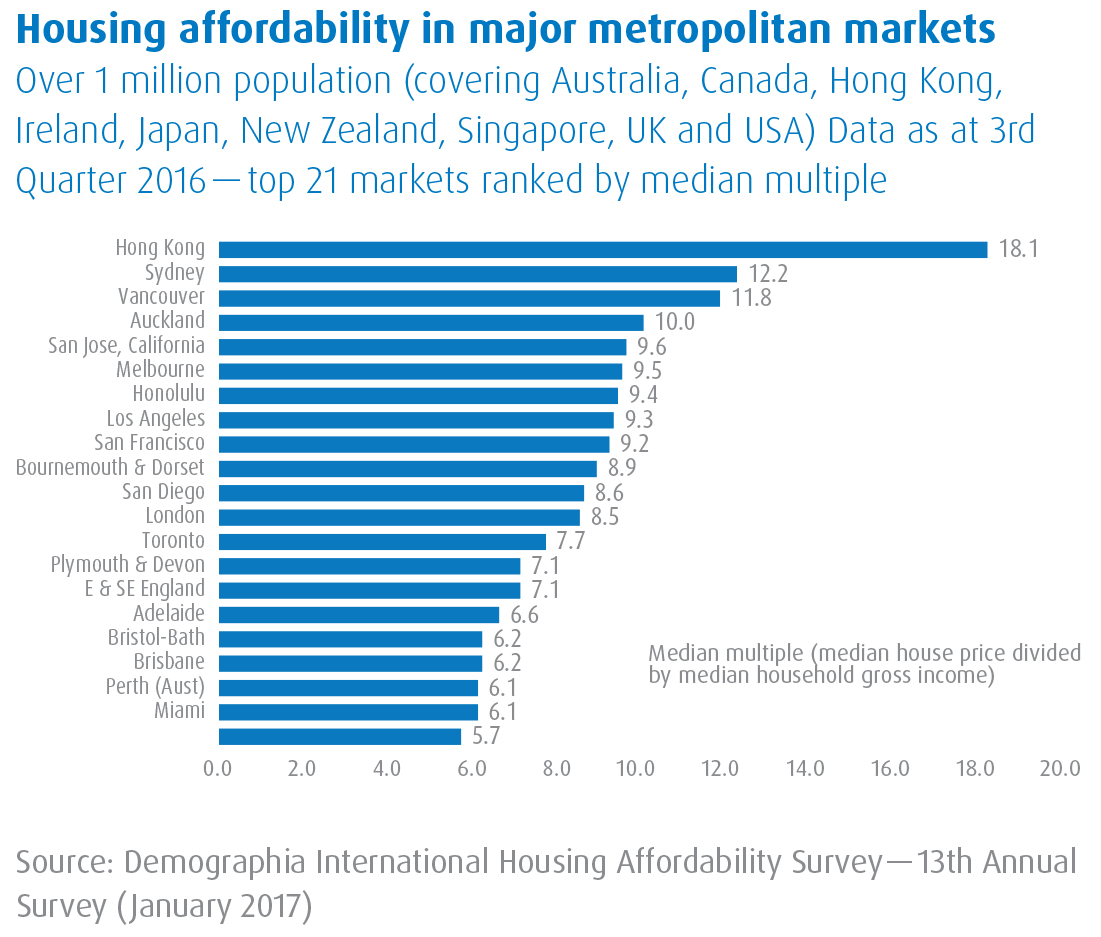

Each year at this time we like to highlight the work undertaken by the Demographia group — an organisation that painstakingly assembles housing affordability data in nine developed countries. We reproduce part of their findings below:

Housing affordability in major metropolitan markets Over 1 million population (covering Australia, Canada, Hong Kong, Ireland, Japan, New Zealand, Singapore, UK and USA) Data as at 3rd Quarter 2016 — top 21 markets ranked by median multiple

Demographia, very sensibly, rank housing affordability on the basis of the median house price divided by the median household income. In the “old’ days (not too long ago!) it was reckoned that a multiple of around 3.0 or less was about right — and this was supported by many studies. In the U.S., for example, Demographia point out that median multiples were overwhelmingly below 3.0 until the 1970s and remained at that level in most housing markets until the early 2000s. Demographia rate a multiple of 3.0 or less as “affordable”; 3.1 to 4.0 as “moderately affordable”; 4.1 to 5.0 as “seriously unaffordable” and 5.1 or more as “severely unaffordable.”

In the above chart all of the cities listed are classified as “severely unaffordable.” The accolade as the priciest of the bunch goes, once again, to Hong Kong. Some observers will consider Hong Kong a special case because of its tiny area and high population density. This is, of course, true, but ultimately it boils down to supply. The Hong Kong government controls the land and derives a significant proportion of its revenue from property. It tightly controls how much new land is released to developers — an example of a vested interest helping maintain high prices. Other relevant factors include the many ex-pats, who frankly aren’t too bothered about the cost of accommodation, as well as a number of rich “mainlanders” (absent landlords) who have diversified their wealth into the Territory.

Nevertheless, it remains the case that more than 90% of the population are ethnic Chinese who have migrated to Hong Kong mainly from the near-north provinces over the last 60 or more years (the fastest rates of growth occurred in the three decades following WW2). It is these people and, in particular, their children and grandchildren who are shouldering the burden of extraordinarily expensive housing (median income of HK$300,000 and median house price of HK$5,422,000).

Several times in the last half-century the real estate market has yo-yoed spectacularly in Hong Kong and to suggest this will never happen again is a statement we’re not prepared to make.

Australian capital cities figure prominently in the list of “severely unaffordable” markets with Sydney topping the list by a significant margin. This city is currently caught up in a buying frenzy. In the weekend prior to this edition of Global Investment Insights being put to rest, the auction clearance rate in Sydney was a near-record of 81.1%. Buyers are snapping up virtually anything that comes on the market at prices that make the eyes water. According to Demographia, as of Q3 last year, the median household income in Sydney was A$88,000 and the median house price an astonishing A$1,077,000.

On this page is a photo of a house that sold for A$2.3 million in February. This is an unrenovated and quite unremarkable property located around eight miles due west of Sydney’s CBD. It previously sold for A$700,000 eight years ago. To save you working it out, that’s capital growth compounding at an annualized rate of 16%.

In the past five years median household income in Sydney has increased by A$9,000 but median house prices have increased by A$439,000. Prices are now beyond the reach of mere mortals. Anyone attempting to purchase their first home needs to have the benefit of a lottery win or wildly generous parents.

Household debt in Australia relative to gross household disposable income already represents one of the highest ratios in the world. Interest rates are key to when (not if) the nonsense will end. The Reserve Bank of Australia is only too well aware of the precipice on which Australian housing sits and is trying to talk down the buying frenzy without raising interest rates. Rates in the U.S. are finally on the march and Australia, and most other countries in this increasingly integrated financial world, will inevitably follow suit. The era of disinflation is over. Start getting used to the new (old) normality.

Recently the Victorian State government in Australia, in typical cack-handed political fashion, announced that it would eliminate stamp duty for owner-occupier purchases of dwellings priced under A$600,000. They did this (supposedly) in the naïve belief that it would help reduce the cost of housing. Far from it — the “savings” will simply be added to the property price by the seller. This is no different from all the public money handed out in the form of first-home-owner-grants and the like during the Great Recession (which, incidentally, Australia largely avoided). These grants simply inflated the price of houses and increased government debt.

Australia employs a long-standing tax wheeze called negative gearing, which enables house buyers to purchase any number of houses, leverage them to the point where the total investment is running at a loss, after taking rental income, interest and expenses into account and then write the loss off against their regular income. If held for more than twelve months only half the capital gain is taxable. How cute is that? To suggest that it is an extreme distortion of the tax system, that it puts constant upward pressure on house prices, encourages speculation etc. etc. results in howls of protest from all the vested interests, Global Investment Insights — Q1 2017 Page 3 including most politicians. This is seen as a sacred cow of the taxation system and it will take a courageous political leader to dismantle or even just amend the structure — but perhaps we are into oxymoron territory there.

Of course this whole pack of negatively geared cards relies on one thing — ongoing house-price inflation. If house prices falter (and, dare we say it, start to fall) these heavily leveraged “investments” are going to start looking pretty silly. Group psychology can turn on a penny and a few forced sales can suddenly turn into a deluge.

Selective amnesia seems to afflict the general public when it comes to property. They quickly forget that prices can and do fall. Take a look at what happened in the U.S. in 2007 - 2009 (and Spain, Portugal, Ireland, Greece, the UK et al.)

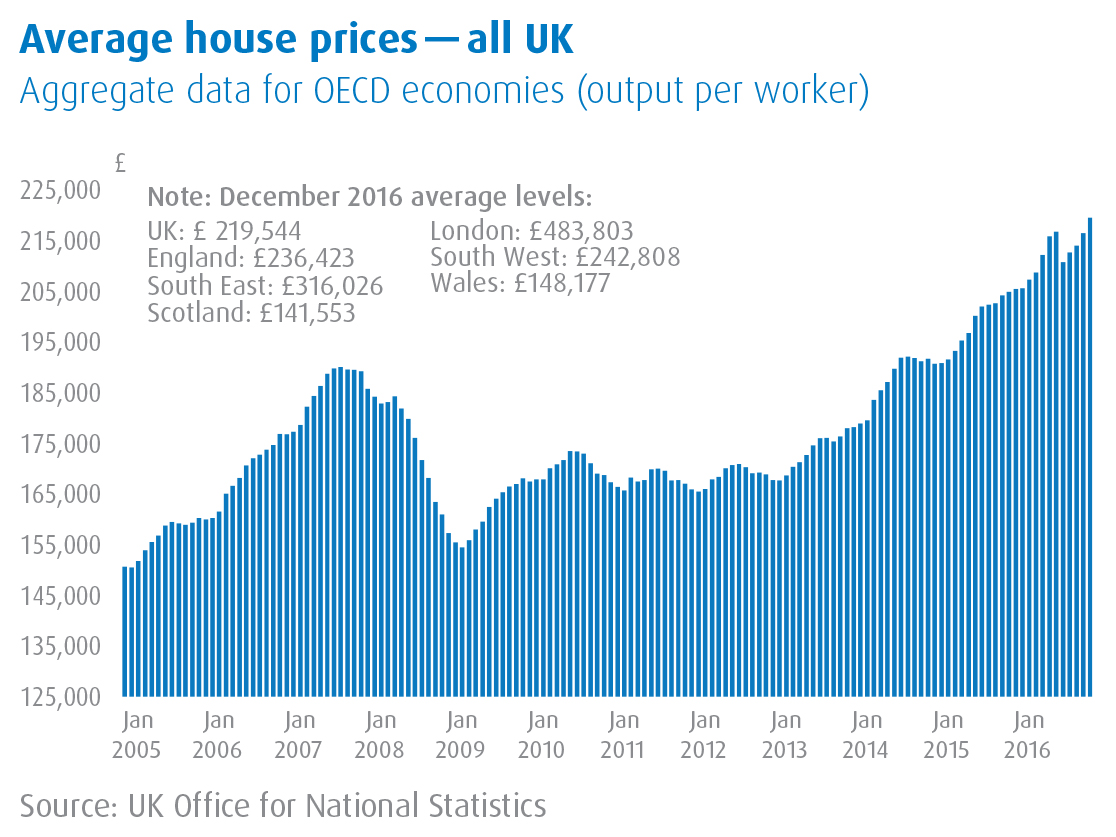

In the UK, where the decline in prices was milder than in many other countries, it was still sufficient to rattle the teeth of heavily geared home-owners and give many bankers heart palpitations. Look at the chart to the right. The pre-recession peak for an average of all-UK prices was in September 2007 at £190,032 and the post-recession low was £154,452 in March 2009 — a fall of 19%. In the prosperous South East (around London) average prices fell by 20% over the same period. In the U.S. the average peak to trough fall was around 21% (all-U.S. data) — and that was sufficient to take the world economy to the edge. Of course, thanks to quantitative easing and other unorthodox measures, prices then picked up and passed pre-recession highs — and that is precisely why we are concerned!

We have tended to focus on Australia in this diatribe but as the country’s largest five cities are all featured in Demographia’s Top 20 “median multiple” list we feel it merits special mention. Don’t think we are complacent about the many others that are in the “severely unaffordable” category, because they all induce a troubled sleep.

All investments involve risk, including the possible loss of principal.

Foreign investing involves special risks due to factors such as increased volatility, currency fluctuation and political uncertainties. High yield bond funds may have higher yields and are subject to greater credit, market and interest rate risk than higher-rated fixed-income securities. Keep in mind that as interest rates rise, prices for bonds with fixed interest rates may fall. This may have an adverse effect on a Fund’s portfolio.

Investments cannot be made in an index.

This presentation may contain targeted returns and forward-looking statements. “Forward-looking statements,” can be identified by the use of forward-looking terminology such as “may,” “should,” “expect,” “anticipate,” “outlook,” “project,” “estimate,” “intend,” “continue” or “believe” or the negatives thereof, or variations thereon, or other comparable terminology. Investors are cautioned not to place undue reliance on such returns and statements, as actual returns and results could differ materially due to various risks and uncertainties. This material does not constitute investment advice. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. Investors should seek advice regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Investment involves risk. Market conditions and trends will fluctuate. The value of an investment as well as income associated with investments may rise or fall. Accordingly, investors may receive back less than originally invested.

Pyrford International Ltd. (Pyrford) is a registered investment adviser and a wholly owned subsidiary of BMO Financial Corp. BMO Global Asset Management is the brand name for various affiliated entities of BMO Financial Group that provide investment management and trust and custody services. Certain of the products and services offered under the brand name BMO Global Asset Management are designed specifically for various categories of investors in a number of different countries and regions and may not be available to all investors. Products and services are only offered to such investors in those countries and regions in accordance with applicable laws and regulations. BMO Financial Group is a service mark of Bank of Montreal (BMO).

BMO Asset Management Corp. is the investment adviser to the BMO Funds. BMO Investment Distributors, LLC is the distributor. Member FINRA/SIPC.

BMO Asset Management Corp., BMO Investment Distributors, LLC, BMO Private Bank, BMO Harris Bank N.A. and BMO Harris Financial Advisors, Inc. are affiliated companies. BMO Private Bank is a brand name used in the United States by BMO Harris Bank N.A. BMO Harris Financial Advisors, Inc. is a member FINRA/SIPC, an SEC registered investment adviser and offers advisory services and insurance products. Not all products and services are available in every state and/or location.

Investment products are: NOT FDIC INSURED — NOT BANK GUARANTEED — MAY LOSE VALUE.

© 2017 BMO Financial Corp. (5639958, 4/17)