Sluggish growth and aggressive central bank actions following the Global Financial Crisis pushed interest rates down to unprecedented levels, even negative outside the US, for longer than many would have expected. Investors’ resultant demand for yield (and growth) has supported an unusually disparate group of stocks, all of which might experience meaningful and justified deratings as interest rates begin to lift off from historic lows. This poses a particular concern for us as value investors because we must continuously be on guard against stocks whose apparent cheapness is actually a sign that their fundamentals are in imminent danger of deteriorating. Indeed, there are many monsters lurking beneath the bed that the Fed has made.

We are especially interested in identifying companies whose business model, or stock price, has benefited from the prolonged period of unconventional monetary policy that may be on the verge of ending. Investors in US companies offering high yields, carrying heavy debt loads, issuing debt to buy back stock, or expecting high growth rates have all prospered on the back of the decline in interest rates. These stocks, while different in many defining characteristics, are all negatively exposed to rising rates. Meanwhile, we believe more unloved groups such as US financials, materials, and higher quality value names are well-positioned to outperform on a relative basis if monetary conditions continue to tighten.

Bond surrogates: stocks with a high beta to bonds

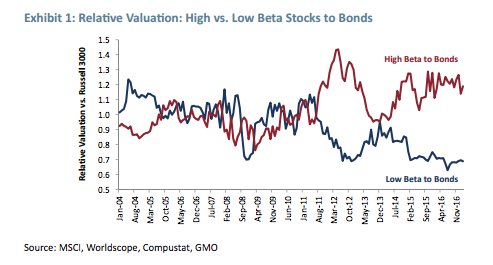

As Exhibit 1 indicates, US stocks whose returns are most sensitive to bonds have seen their valuations climb dramatically since late 2008/early 2009. Bond surrogates are defined as the top quartile of the market on trailing 1-year beta to 7- to 10-year US government bonds.1 This group currently trades at a 20% premium to the market. We compare these stocks to those in the bottom quartile, which have seen their relative valuations decline precipitously. The valuation gap between stocks with the most and least sensitivity to bond prices is near the widest it has been over the last 12 years. Investors have preferred to own companies whose business models and/or balance sheets are most amenable to a low rate world. Stocks with a negative beta to bonds have, by comparison, been shunned.

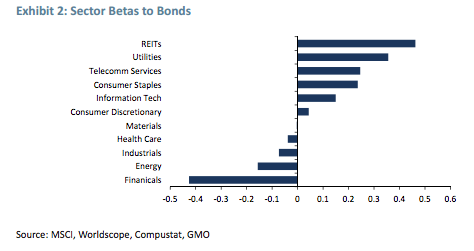

The composition of the high beta to bonds cohort is no mystery. It consists primarily of companies from the REITs, Utilities, Telecommunication Services, and Consumer Staples sectors, which traditionally offer higher yields and/or stable and predictable cash flows (see Exhibit 2). The valuations of these high-yielding bond surrogate stocks expanded aggressively in the rate cutting aftermath of the Global Financial Crisis (GFC) and more so during the first cycle of the European Credit Crisis in 2011. Many of the companies in this high-yield cohort are less economically sensitive and of higher quality than the broad market, offering safety in an uncertain world. REITs are perhaps the exception, but their rich yields have proved too tantalizing to yield-starved investors. Given current elevated valuations for these stocks, however, their role as “safer” equities is suspect at best. Even if one believes lower rates will last a while longer, this possibility may already be priced in. If, however, one’s view is that longerterm yields are set to rise, then bond-like equities look like an explicit anti-value position.

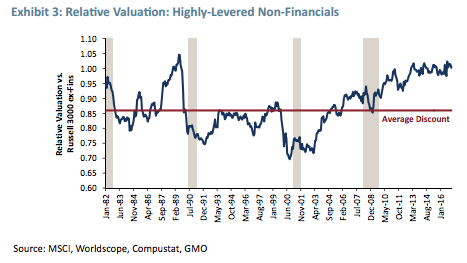

Highly-levered stocks

Highly-levered non-financial companies2 represent another beneficiary of the low rate world. Historically, companies burdened with the most significant debt loads have traded at about a 14% discount to the market on our composite value metrics. As Exhibit 3 indicates, that discount tends to widen leading into and during recessions as cash flows dry up, interest coverage wanes, and defaults rise.

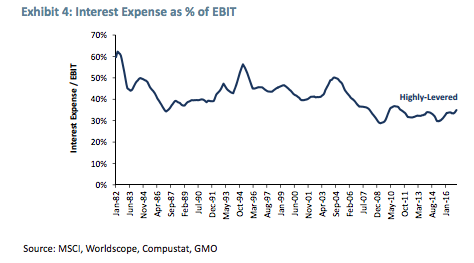

Aggressive action by the policymakers muted the market’s negative reaction to levered companies during the GFC. Immediately following the crisis, levered firms were valued in line with historical norms. Since 2010, investors have been anticipating stronger earnings growth, due partly to falling interest burdens from the lower rates on offer, and re-rated these firms accordingly. Today, the most levered companies trade near parity with the market, offering no discount for their more precarious balance sheets. Perhaps the market has forgotten what can happen to levered firms in an economic downturn? As Exhibit 4 shows, the median percentage of EBIT being diverted to interest payments for this cohort of companies has remained roughly constant since the GFC. Interest payments have grown in line with EBIT, even as interest rates have fallen. This should be a clear warning sign to anyone familiar with the vicious dynamics of forced deleveraging.

Financial engineers: swapping debt for equity

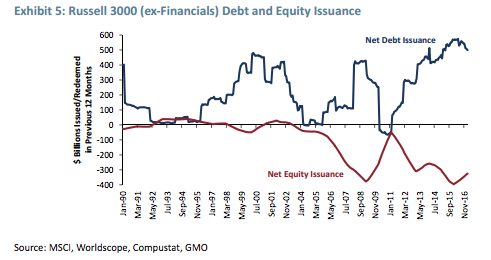

Winner number three in the low rate environment has been middle-of-the-road financial engineers. The blue line in Exhibit 5 displays the amount of debt issued by US companies (excluding financials) on a rolling 12-month basis while the red line indicates how much equity was redeemed (negative net issuance). Our colleague, James Montier, has written much about this massive debt for equity swap.3 Faced with low growth prospects and friendly financing markets, companies have taken advantage of lower interest rates to raise large amounts of debt to buy back stock. This has had the effect of improving both EPS and, presumably, executive compensation, while massively shifting the overall capital structure in favor of debt over equity. This behavior, as the chart suggests, has been widespread. A curious thing for the equity market to cheer, but c’est la vie.

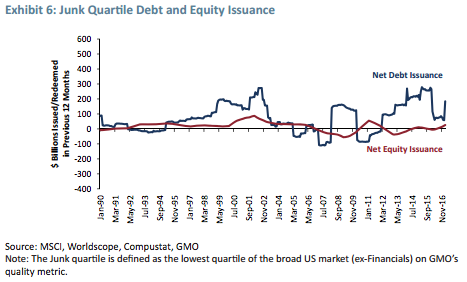

Of course, not all companies are equally guilty. Some firms are probably engaged in responsible balance sheet management, while many others are undoubtedly ensuring the future employment of bankruptcy lawyers. GMO’s quality metric is a useful lens through which to view this phenomenon.4 While low quality, junky companies have certainly been responsible for a large portion of the debt issued, they are surprisingly not the worst offenders as far as the debt for equity swap goes. Exhibit 6 shows that junky companies have, in aggregate, not been large buyers of their own stock. Perhaps low quality firms were wise to refinance their debt at lower rates and extend their maturities, but balance sheets have expanded and they remain prone to economic downturns and rises in interest rates. This, however, is par for the course when it comes to low quality companies. The real dangers lie elsewhere.

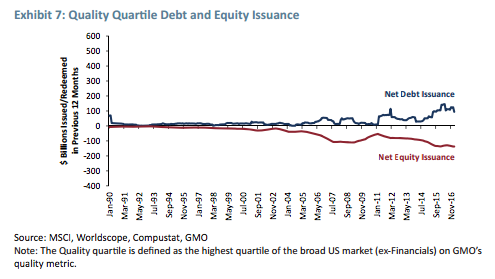

At the other end of the spectrum, quality companies have also re-engineered their balance sheets using cheap debt and have indeed been swapping debt for equity (see Exhibit 7). Before casting judgment, it should be remembered that many high quality firms are global multi-nationals that have significant offshore cash holdings. For these firms, the low interest rate environment presented a unique opportunity to effectively distribute this cash to shareholders in a tax-efficient manner. Further, given their superior business models, quality companies can sustain higher debt loads and the financial engineering was arguably in the best interests of shareholders. For our purposes, we are willing to give the high quality cohort as a whole the benefit of the doubt. Quality as a group, and particularly select Technology, Health Care, and Consumer Staples companies, looks quite attractive relative to the broad US market on valuation grounds.

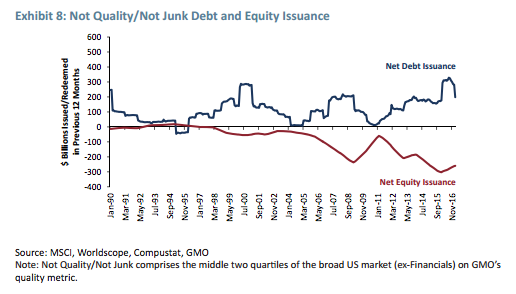

This leaves us with a large cohort of “middle quality” companies: firms that are neither quality nor junk. As can be seen in Exhibit 8, these firms have aggressively partaken in the debt for equity frenzy. In fact, the cumulative dollars spent on share buybacks since the GFC has been nearly matched by the total debt issuance. These companies have significantly altered their capital structures in order to boost earnings in a low growth, low rate environment. Unlike quality companies, most of these middling companies do not have the business models that can sustain dividends and buybacks while simultaneously servicing their newly higher debt loads once their interest payments increase or their cash flows shrink. This is a large and heterogeneous group of companies and not all of them are guilty of levering up to buy back equity. The worst offenders, however, span the entire spectrum from Consumer-oriented names to Industrials and Technology firms. Many members of this middle quality group stand a real risk of getting de-rated very quickly should interest rates rise and shareholders awaken to the reality that significantly less of the pie will be left over for them after the new legions of bondholders have taken their share.

Growth stocks

The last group of stocks that have become distorted due to the Fed’s aggressive monetary policies are traditional growth stocks. In a slow growth world, investors have sought companies delivering higher earnings growth. As interest rates have fallen, growth companies have benefited disproportionately from lower discount rates because most of their cash flows are weighted further in the future. In a world where near- and medium-term cash flows are hardly less valuable than cash today, the promise (or perhaps hope) of even marginally higher cash flows in the distant future can look very attractive indeed.

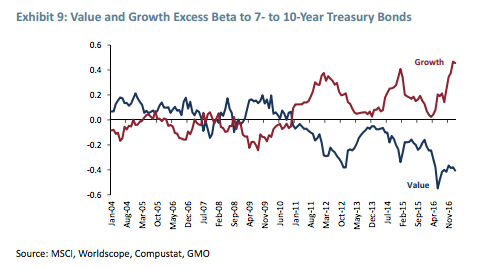

Since the beginning of the low interest policies in 2008/2009, the disparity between growth and value stocks’ sensitivities to bonds has generally widened, especially after 2014 when all of the world’s major central banks were fully engaged in some form of extreme monetary easing. As Exhibit 9 indicates, growth’s excess beta to bonds has increased substantially since the GFC while value has moved from positive to quite negative.

Exhibit 9 should be interpreted5 as follows: Given a 1% fall in the price of 7- to 10-year bonds, all else equal, we would expect value to outperform the market by 0.4% and growth to underperform the market by about 0.5%. On a relative basis, growth stocks stand to lose to both the market and to value stocks if and when rates begin to rise in earnest. In fairness, a decent portion of the spread between value and growth is being driven by the negative beta of financial stocks to bonds as shown in Exhibit 2. This, though, does not change our belief that growth stocks are primed for a meaningful de-rating when investors begin to discount the future more aggressively.

Navigating the path ahead

A strange brew of companies have benefited from the low rate environment over the last cycle. High yielders, aggressively-levered companies, financial engineers, and growth stocks have high valuations and sensitivities to rising rates. Investors have prized these somewhat disparate attributes, which have benefited a wide range of sectors from Consumer Staples to Resources to Specialty REITs, with some companies in these sectors, of course, having more than one of these characteristics. While any tightening in US monetary policies could be slow and shallow, even small increases in rates could move discount rates up, harming these “low rate beneficiaries.” Investors beware.

We should note that many bond surrogates, highly-levered firms, and would-be financial engineers are to be found within the standard value indices. Therefore, an investment approach that recognizes attractively-priced quality names, screens out companies that engage in questionable balance sheet management, and is attuned to the goings-on in the corporate bond markets will be required to safely navigate the equity markets as interest rates continue their ascent off of zero.

As a final thought, both Brexit and the election of President Trump have introduced a large amount of economic uncertainty into the investment equation. For example, the Trump administration has discussed a variety of tax, trade, and other policies. Some, if implemented, could change the long-term value of companies while others would have little impact. Markets, either way, could become more volatile. A border adjustment tax in the US is one policy that would impact companies quite differently. Heavy importers like the Retail sector would certainly be losers given higher import costs. Such a tax, moreover, could be deemed to be a stealth tariff, possibly triggering a trade war. The unravelling or modification of long-standing trading relationships and changing industrial and economic policy in the UK, Europe, and the United States will most certainly create new winners and losers within the corporate sector, but it is far too early to know who stands to benefit.

The traditional value investor’s admonishment that “the greatest sin is to overpay for assets” becomes ever more important as the future value of assets gets harder and harder to forecast. Applying a high discount rate to cash flows that will not occur until far in the future is a rational response to heightened economic and political uncertainty and would likely, in terms of relative returns, be kind to value investors and harmful to growth-oriented investment styles. With this in mind, it is worth recalling that the immediate response of the equity market to Brexit and the 2016 US election was to strongly favor value over growth.

Neil Constable: Dr. Constable is the head of GMO’s Global Equity team. Previously at GMO, he was the head of quantitative research and engaged in portfolio management for the Global Equity team’s quantitative products. Prior to joining GMO in 2006, he was a quantitative researcher for State Street Global Markets and a post-doctoral fellow at MIT. Dr. Constable earned his B.S. in Physics from the University of Calgary, his Master’s in Mathematics from Cambridge University, and his Ph.D. in Physics from McGill University.

Rick Friedman: Mr. Friedman is a member of GMO’s Asset Allocation team. Prior to joining GMO in 2013, he was a senior vice president at AllianceBernstein. Previously, he was a partner at Arrowpath Venture Capital and a principal at Technology Crossover Ventures. Mr. Friedman earned his B.S. in Economics from the University of Pennsylvania and his MBA from Harvard Business School.

Disclaimer: The views expressed are the views of Neil Constable and Rick Friedman through the period ending April 2017, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Copyright © 2017 by GMO LLC. All rights reserved.

Copyright © 2017 by GMO LLC. All rights reserved.

1 The beta to bonds is calculated as the trailing 1-year beta of each stock to the iShares 7-10 Year Treasury Bond ETF (IEF), an ETF that tracks a basket of 7- to 10-year US government bonds, after controlling for the overall market, which we proxy with the Russell 3000. For regression junkies: We ran a bivariate regression of individual stock returns on both the daily returns of the overall market and the returns of IEF. The coefficient on the daily returns of IEF represents the return in excess of the market return for a given move in IEF.

2 The highly-levered group consists of the top one-third of companies in the Russell 3000 on GMO’s composite leverage metric, which includes multiple measures relevant to levered firms (e.g., debt/assets, interest coverage).

3 See “The World’s Dumbest Idea,” December 2014 and “Six Impossible Things Before Breakfast,” March 2017. These white papers are available with registration at www.gmo.com.

4 Recall that our quality metric is derived from a firm’s level of profitability, the stability of profitability, and overall level of indebtedness. High quality firms typically have competitive advantages conferred by intellectual property, brands, or dominant market positions. Low quality firms typically operate in businesses with low barriers to entry or are particularly exposed to cyclical economic forces.

5 The “excess” beta is the coefficient on the daily returns of IEF in a regression that includes both the daily returns of IEF and the daily returns of the Russell 3000. It represents the return of a stock in excess of the market return for a given move in IEF.

© GMO

Read more commentaries by GMO

Aggressive action by the policymakers muted the market’s negative reaction to levered companies during the GFC. Immediately following the crisis, levered firms were valued in line with historical norms. Since 2010, investors have been anticipating stronger earnings growth, due partly to falling interest burdens from the lower rates on offer, and re-rated these firms accordingly. Today, the most levered companies trade near parity with the market, offering no discount for their more precarious balance sheets. Perhaps the market has forgotten what can happen to levered firms in an economic downturn? As Exhibit 4 shows, the median percentage of EBIT being diverted to interest payments for this cohort of companies has remained roughly constant since the GFC. Interest payments have grown in line with EBIT, even as interest rates have fallen. This should be a clear warning sign to anyone familiar with the vicious dynamics of forced deleveraging.

Aggressive action by the policymakers muted the market’s negative reaction to levered companies during the GFC. Immediately following the crisis, levered firms were valued in line with historical norms. Since 2010, investors have been anticipating stronger earnings growth, due partly to falling interest burdens from the lower rates on offer, and re-rated these firms accordingly. Today, the most levered companies trade near parity with the market, offering no discount for their more precarious balance sheets. Perhaps the market has forgotten what can happen to levered firms in an economic downturn? As Exhibit 4 shows, the median percentage of EBIT being diverted to interest payments for this cohort of companies has remained roughly constant since the GFC. Interest payments have grown in line with EBIT, even as interest rates have fallen. This should be a clear warning sign to anyone familiar with the vicious dynamics of forced deleveraging.