With the outcome of last year’s Brexit vote paving the way for the UK to leave the European Union (EU), British Prime Minister May began the formal divorce proceedings last month.

And now, she has surprisingly called for a snap election, earlier than expected, on June 8.

In the meantime, I keep hearing from investors, what does this mean for the markets? In Europe? In the UK?

Not just any deal will do

The politics of the outcome of the Brexit referendum are complex. Let’s leave it to say that many who supported her, expected Prime Minister May to draw a much firmer line than the realities of both the EU and UK economies could withstand.

After all, according to the UK Office for National Statistics (ONS), as the UK’s closest neighbor, the EU is the destination of 44% of the UK’s exports of goods and services and the source of 53% of its imports as of 2016. The same data shows that exports to the EU account for ±13% of the UK’s Gross Domestic Product (GDP) and are a much bigger share than the EU’s equivalent exports to the UK at ±4% of GDP.

The EU also regulates a lot of important issues, such as nuclear energy, air travel and of course external trade with non-EU countries. If the UK were to simply leave the EU without any kind of deal, it would risk serious disruption in trade, supply chains, air travel, energy supply and of course immigration.

The prospect of lorries stacking up in Dover, grounded airplanes and an influx of immigrants from Calais weighs on May and her supporters.

This is likely part of the reason May has called a snap election. If the latest polls are correct1, she will be able to increase the Conservative majority, which will allow her to work around some of the more hardcore Brexit factions.

Coming to terms

Given this situation, the Prime Minister is working to modify her approach. As a first step, she announced that the UK might need to pay a divorce settlement as part of the exit agreement.

A second step entailed her conceding that even if the EU were to allow exit and trade agreement talks to partly run in parallel, it’s very likely there will need to be a bridging agreement that preserves the status quo.

In a third step, by calling for a snap election now, May has extended the timeline for the next general election from 2020 (one year after Brexit is expected to be completed in 2019) to 2022. Thus, instead of confronting voters one year after Brexit, she will now have three years.

And finally, a tacit understanding is developing that many of the regulatory bodies will probably need to be duplicated. That, combined with the need for free trade, means the future relationship might actually not turn out to be that different from its current EU membership.

Four things to watch in the months ahead

The election campaign: We will be closely watching on what Brexit platform May will campaign. Will it be her initial Hard Brexit (i.e. leaving without any deal between the UK and EU) line or her current Not-so-Hard Brexit (i.e. taking more of a long-term discussion/divorce proceedings-like approach) line? Markets are currently anticipating the latter, but we think most of the impact of her change in stance is behind us.

The tenor of negotiations: On April 29, the EU will formally approve its response to the UK’s notification that it invokes Article 50. The guidelines included in that response will draw the EU’s battle lines.

In my view, the outlook is not great for the UK for next steps on the Brexit. The draft EU response, which is fairly strict in its terms, has met with almost universal approval from the EU members.

And with all the Gibraltar-like political scores still left to settle, it may make for acrimonious negotiations that could prompt market volatility. If this is the case, it is likely to create more uncertainty that could weigh on the UK’s economy.

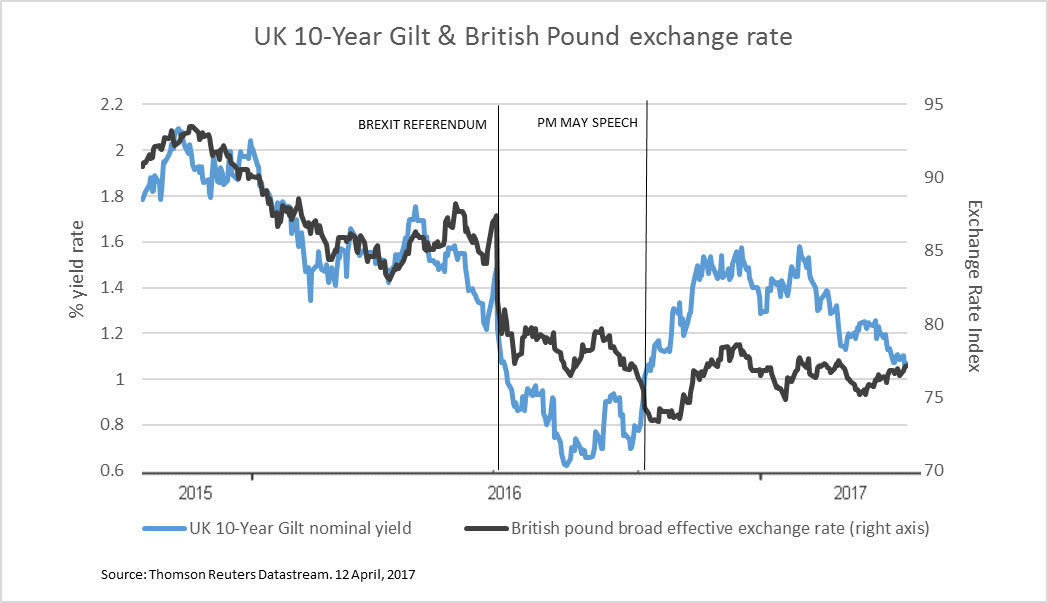

Market reaction to ongoing negotiations: As negotiations progress, it will be important to watch the market’s reaction. If the market reacts strongly to the first setback like it did when May made her first hard Brexit speech (see chart below), that could be worrying.

If instead markets are largely unfazed, that would indicate that the risks are likely already mostly priced in. As I’ve noted before, the pound exchange rate is still the best indicator in this regard. Indeed, its reaction to the call for a snap election was promising. However, our team of investment strategists also watches the yield on the British 10-year government bond, the Gilt2, as an indicator of the expected economic fallout.

Economic developments: The UK economy has done remarkably well in the aftermath of the referendum, but now the impact of the large decline in the pound is starting to be felt, as we recently noted in our Global Market Outlook- Q2 Update.

Living standards have started to decline as wage growth3 decelerates and inflation picks up.4 Survey-based leading indicators such as producer confidence5 are still strong, but business investment, according to March 15, 2017 ONS data, continues to decline.

I expect the British economy to slowly lose momentum, but will be on the lookout for conditions to worsen more quickly. Consumer spending and housing activity will be particularly important to watch in the months ahead.

So, keep an eye on the election campaign, the negotiations and UK economic indicators in the months to come. I don’t believe there is any reason to panic and run from UK opportunities, but potential political risk does need to be closely monitored.

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page.

Investing involves risk and principal loss is possible.

Past performance does not guarantee future performance.

These macroeconomic forecasts do not constitute a projection of the stock market or of any specific investment.

Forecasting is inherently uncertain and may be incorrect. It is not representative of a projection of the stock market, or of any specific investment. Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

This material is not an offer, solicitation or recommendation to purchase any security. Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type.

The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional. The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity.

Please remember that all investments carry some level of risk. Although steps can be taken to help reduce risk it cannot be completely removed. They do no not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns. They do no not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

Non-US markets entail different risks than those typically associated with US markets, including currency fluctuations, political and economic instability, accounting changes, and foreign taxation. Securities may be less liquid and more volatile.

Russell Investments’ ownership is composed of a majority stake held by funds managed by TA Associates with minority stakes held by funds managed by Reverence Capital Partners and Russell Investments’ management.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the “FTSE RUSSELL” brand.

Copyright © Russell Investments 2017. All rights reserved.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.

UNI - 11036

1 Wikipedia. British political polls from May 2015 through April 2017.

2 Gilts are bonds that are issued by the British government and generally considered low risk. Gilts are the U.K. equivalent to U.S. Treasury securities.

3 UK Office for National Statistics. February 15, 2017.

4 UK Office for National Statistics. March 15, 2017.

5 Market PMI UK Services Report. April 5, 2017