Is the Fed Moonlighting or Are We Still in La La Land? The Envelope Please...

Learn more about this firmThe start to 2017 has been filled with high profile snafus, from blown soft drink commercials, to overbooked flights gone viral. None were more visible than the Oscars. French elections? North Korea? Syria? Yeah, yeah, but did you see the Oscars? In the biggest auditor flub since Enron, the wrong winner for the top award, Best Picture, was accidentally announced at the Academy Awards, much to the chagrin of all involved.

With markets seeking to avoid similar toe-stubbing in the policy arena, we examine the drivers of the fixed income markets for the near term. In doing so, we consider President Trump’s fiscal policy influence, Janet Yellen’s monetary policy impacts and evolving exogenous geopolitical dynamics. So, who or what will determine the market’s course moving forward?

Who’s driving the bus?

The surprise election of Donald Trump as President of the United States has dominated the news cycle as it pertains to markets (and pretty much everything else.) The new administration’s policy proposals (fiscal stimulus, deregulation and corporate and personal tax reform) were baked into market assumptions nearly immediately in late 2016, causing a significant increase in expectations of growth and inflation. These expectations impacted markets broadly and had significant implications for fixed income specifically. Interest rates rose nearly 100 basis points during the fourth quarter and credit spreads tightened, reflecting a more favorable corporate landscape. In the midst of this recalibration, the market seemingly shrugged off the Fed’s second rate increase and market consensus shifted to a fiscal policy driven world.

However, the reflation trade, dubbed by some as the ‘Trump trade’ hit a snag with the Republican failure to secure sufficient votes for their bill to repeal and replace Obamacare in March. The inability to maintain party support for the first major legislative initiative has led to reduced expectations of other reflationary policy initiatives. While many recognize the challenges surrounding the realities of policy implementation, the pull forward of positive economic news risks a heightened reaction to potential disappointment.

With this snag, monetary policy again took center stage. The Fed reestablished its significant role vis-à-vis a well telegraphed rate hike for the second consecutive quarter. Additionally, the Fed struck a more hawkish tone beginning to discuss not only further rate hikes, but the eventual wind down of the balance sheet.

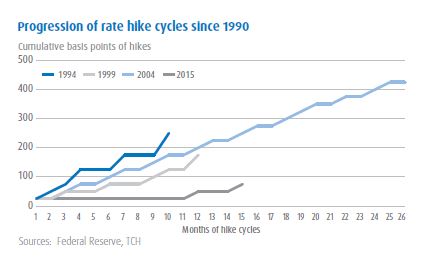

Three’s a streak… it has happened before

The Fed has talked of a path to normalization for years; with the March rate hike now being the third hike in fifteen months, it feels that we have ‘officially’ entered a rate hike cycle. Each time the Fed has hiked rates three times has widely been recognized as a full-on hike cycle and the current period has a vibe of continuation.

There have been three distinct hike cycles since 1990:

- In 1994, the cycle began with Fed Funds at 3% and the first three hikes were in consecutive months beginning in February. That cycle included 7 distinct hikes within twelve months, including three 50 basis point moves and one 75 basis point move (yes really.)

- In 1999 – 2000, the cycle began when the Fed Funds rate was 4.75% (likely greater than the terminal point of the current cycle) and the first 3 hikes occurred in June, August and November of the same year.

- The 2004-2006 hike cycle began when the Fed Funds rate was 1%, the current upper bound of the Fed Funds rate range. The first three hikes were in June, August and September of the same year. This was the longest of the three cycles, lasting almost exactly two years from the first hike to the last.

These historical comparisons highlight a few noteworthy features of the recent time period:

- The current cycle is, as we have long suggested, a prolonged drawnout process.

- Only one other cycle spanned three years of hikes (04-06), but that cycle averaged nearly 6 hikes per year.

- No cycle has been as slow to begin as the current one – with the longest of the past three taking six months before the third hike, whereas this cycle has spanned three years to achieve the same 75 basis points of increase that was delivered in November 1994.

- The lack of Fed actions from 2008 – 2015 was more the aberration than the norm, there has been only one other year since 1990 without a Fed rate hike or cut (1993.)

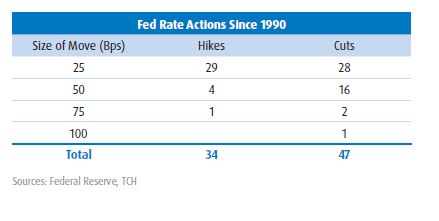

While each cycle is unique and the speed and length of cycles cannot be interpreted as a guide for subsequent cycles, in examining the period since 1990, certain trends still emerge. The Fed feels more free to cut rates in large increments with only 60% of cuts being 25 basis points versus 85% of hikes. The large moves (75 basis points or more) are almost exclusively cuts, (three of four), representing rapid responses to crises. As would be expected, incrementalism is favored for normalization. There have been more cuts (47) than hikes (34), reflecting the long term downward trend in rates broadly over the period.

Certainly, if chattering Fed officials are to be believed we have only seen the start of the normalization path. Though their speeches have suggested we are looking at an accelerating rather than constant path, the expectations for the end of the cycle remains significantly lower than past cycles, with the Fed ‘dot plot’ unchanged with a 3.0% long term Fed Funds rate. The eventual unwind of the Fed’s large balance sheet will be another distinct feature of this cycle as previous easing cycles had included only more traditional monetary policy tools.

For multiple years, the Fed had suggested, intoned, hinted and nearly begged for multiple hikes, but only delivered one at the 11th hour. Though the Fed has long been market aware, the current regime has seemed especially so.The March hike had the distinct feel of the Fed seizing an unexpected opportunity the market had granted, especially after coming up short in 2015 and 2016.

Politics makes strange bedfellows

That opportunity came about after two speeches on February 28th. President Trump delivered his first address to a joint session of Congress. The speech had a strongly stimulative tone, reiterating many of his key campaign proposals and suggesting fiscal policy would be a key driver of the economy for the upcoming period. The same night, San Francisco Fed President John Williams said he expected a rate hike would get “serious consideration” at the next Fed meeting (March 14-15). Prior to the two speeches, the Fed Funds Futures had implied a 52% likelihood of a rate hike at the March meeting, but by morning the probabilities moved higher, exceeding 80%.

It is hard to imagine two more polar opposites in American public life than the Chair of the Fed and the President of the United States. Janet Yellen, the dry academic, is a stark contrast to Donald Trump, the colorful businessman. Yet, the February 28th example illustrates the unorchestrated current symbiosis between the two.

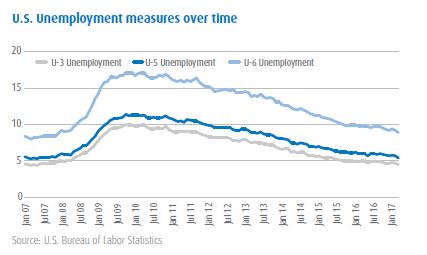

Another shared view, has been the position with regard to unemployment. While headline unemployment has improved for years, a fact that had been raised to suggest the Fed had been overly accommodative, Chair Yellen argued that slack in the labor markets remained. To illustrate this non-headline weakness, she cited various other metrics including underemployment and longterm unemployment to suggest there was a continued role for accommodation. More bluntly, as one might predict, President Trump quipped at an Iowa rally that “the unemployment number, as you know, is totally fiction.” Similarly, (now treasury Secretary) Steve Mnuchin, said in congressional testimony “the average American worker has gone absolutely nowhere. The unemployment rate is not real.” Trump and team have suggested use of the U-5 unemployment measure, which includes discouraged workers, as opposed to the more common U-3 headline unemployment, which does not include discouraged workers in the calculation. The U-6 unemployment measure, which includes underemployed workers, has also been frequently cited as evidence of slack in the labor markets.

None of this is to suggest collaboration between the executive branch and the Fed, which has vociferously maintained its independence. That they share similar ends should not be surprising, but the similarity of their language is noteworthy. This confluence is particularly interesting as we seek to sort through the seeming opposite directions they are now heading.

While the Fed had long sought fiscal stimulus to pair with its monetary stimulus, they are seeking to recede from active stimulus (while remaining accommodative at least for now). By contrast, President Trump is aiming to expand stimulus, though the effects could be weakened by a monetary policy normalization.

So where do we sit in terms of policy cycles?

Is good news good news?

In our commentary from the first quarter of 2015, we asked “When will good news be good news?” At the time, market confidence felt weak enough that good economic news was viewed through the primary lens of whether the Fed would view the news as an opportunity to step back support, which ultimately would be bad for investors. While reduced Fed support can always be viewed as a short-term negative, the current market feel is very different.

In the absence of countercyclical policy, the question would be moot, but the especially large role of the Fed during and after the 2008 crisis justifies the focus placed on the interplay of economic data and monetary policy. If cycles are to be managed by the Fed, then the question of what good economic data means, in terms of monetary policy, becomes essential. From 2008 until 2015, the question could be answered that good economic news meant fears of a countercyclical decrease in support by the Fed.

It feels now that while the Fed is looking at good news as a reason to pull back, the market is comfortable with the level of economic strength to weather the Fed’s reaction. More precisely, as the Fed has not yet gotten to neutral policy, the market views the Fed’s normalization pace as appropriate (or perhaps even generous) given the level of positive news and sentiment.

The market digested the March and December rate hikes with almost no reaction. Even since it was revealed in Fed minutes that the Fed began discussing a wind down of the $4.5 trillion balance sheet, interest rates have declined rather than moving higher, as one might expect were the market on life-support or overly reliant on monetary policy (a la taper tantrum.)

As either the Fed normalization process surpasses market comfort or market data begins to imply overheating, the question will again become more poignant. As it stands, good news appears to be good news, and bad news to be bad news. When either accelerates sufficiently, we would expect the Fed (which continues to be ‘data driven’) to act accordingly. What seems less likely in the near term is bad news being bad enough to provoke a countercyclical response (and thus becoming good news.) More likely, good news provides room for continued moderate normalization or that limited bad news forestalls an already historically slow normalization. Little in the current data suggests the need for forceful action from the Fed to slow an overheating economy and, as such, it seems the Fed will navigate between data points and policy rhetoric with caution.

Drumroll please!

Just as it appeared that fiscal policy had overtaken monetary as the key determinant, markets were reminded that the legislative process can be rougher than an overbooked United Airlines flight. The Fed does not face the same 435 House votes or 100 Senate votes in setting monetary policy, but is just as eager to avoid its own blunder-induced moment in the sun.

Patience is required in observing the dance between the current fiscal and monetary landscape. In this setting, while fiscal policy is a subset of a broader political agenda, the Fed is acting as the counterweight, accelerating normalization as confidence increases, presumably to slow if the Trump/reflation trade fades more significantly.

This uncertainty, amplified by developments in North Korea, Syria and any advances or steps back in the global populist moment, lends to potential short-term volatility. Though markets, bolstered by consumer confidence, have been moderate in their reaction to date, volatility has been most evident at the sector level, such as healthcare near the Obamacare repeal vote or anything Mexico-related near the election. These rhetoric driven reactions and the market’s propensity to overreact have created opportunities, as policy matures from talking points to legislation.

Other policy initiatives to follow may reignite the Trump trade, including a tax package which is being discussed. Personal and corporate tax reform are likely to draw greater party-line support and its success, or lack there-of, could sharply impact confidence on the ability to deliver on the broader suite of market friendly policies. Fiscal stimulus in the form of infrastructure, another key policy proposal, theoretically should be able to appeal across party lines.

While the feel of the market is that good news is back to being good news, the ultimate good news will be when neither monetary policy nor fiscal policy are the key focuses and the organic economy is leading the way. Until then, the winner for biggest driver of markets in 2017 is… oh, wait… is this the right envelope?

Portfolio positioning

Interest rates/duration: Holding duration towards the lower end of relative benchmark range for now, with a bias towards returning to neutral position as fiscal and monetary policy evolve; underweight Treasuries, favoring non-government sectors instead

Credit: Global demand for U.S. fixed income remains strong; Broadly speaking, U.S. corporate balance sheets have managed the credit cycle well; the ever-evolving US political news flow continues presenting upward pressure on volatility, creating opportunities as sectors and subsectors risks are repriced; credit spread compression to near historical averages suggest a more balanced approach to risk

Mortgages: U.S. agency MBS to realize continued support from Fed reinvestment for the time being, but discussions regarding the Fed balance sheet and political rhetoric around the agencies justifies greater caution as the year progresses; agency MBS remain a relative safe haven during periods of global uncertainty

High yield (HY) and emerging markets (EM): Recent market volatility has created additional bottom-up opportunities across the credit spectrum; HY/EM spreads reflect more concern over global uncertainties, though recent spread widening has been too modest to create compelling valuations at a sector level

Fund updates: first quarter of 2017

BMO TCH Core Plus Bond Fund: The Fund outperformed in the quarter with sector and quality selection contributing to relative performance as the Fund remained underweight Treasuries and overweight credit. Credit was the best performing fixed income sector, benefitting the Fund, as spreads tightened and markets priced in a higher level of future growth. Security selection within corporate credit further added to outperformance for the period. With rates declining mildly in the first quarter, the Fund’s below benchmark duration detracted modestly from relative returns. Investment grade corporate floating rate notes did not keep pace with the performance of broader credit for the quarter, but benefitted from the Fed raising the Fed Funds rate in March.

BMO TCH Corporate Income Fund: Security selection within corporate credit led to outperformance for the period. In particular, names within the technology, chemicals and metals & mining sectors added value, while names within the retail sector detracted from performance. The overweight to corporate versus non-corporate detracted from performance in the period, though the underweight to utilities was additive as that was the sole credit sector with negative excess returns. With rates declining mildly in the first quarter, the Fund’s below benchmark duration detracted modestly from relative returns.

BMO TCH Intermediate Income Fund: The Fund’s outperformance was significantly impacted by a litigation settlement from a crisis-era investment received during the quarter. Overweight credit positioning contributed to performance as it was the best performing fixed income sector, however, the overweight to mortgage backed securities (MBS) detracted modestly from relative returns. The Fund’s lower duration profile detracted modestly from performance during the period. Security selection within corporate credit added further to outperformance for the period.

BMO TCH Emerging Markets Bond Fund: The Fund underperformed in the period largely due to the diversification to quasi-sovereign and corporate debt, which underperformed the sovereign benchmark. Country selection was positive during the period. In particular, the contribution from allocations to Mexico is noteworthy given its position in the epicenter of recent political rhetoric. While Trump’s election was initially perceived negatively for Mexican debt, the Fund’s positioning was additive to performance for the quarter.

Taplin, Canida & Habacht (TCH) is the center of excellence for Income Strategies within the U.S. for BMO Global Asset Management. TCH manages over $10 billion of assets and is a subadvisor for multiple open end mutual funds. We are dedicated to investing on behalf of our clients and servicing them to the highest standards. For ore information about TCH, please visit tchinc.com.

All investments involve risk, including the possible loss of principal.

Keep in mind that as interest rates rise, prices for bonds with fixed interest rates may fall. This may have an adverse effect on a portfolio. Foreign investing involves special risks due to factors such as increased volatility, currency fluctuation and political uncertainties. High yield bond funds may have higher yields and are subject to greater credit, market and interest rate risk than higher-rated fixed-income securities. Keep in mind that as interest rates rise, prices for bonds with fixed interest rates may fall. This may have an adverse effect on a Fund’s portfolio.

Investments cannot be made in an index.

This presentation may contain targeted returns and forward-looking statements. “Forward-looking statements,” can be identified by the use of forward-looking terminology such as “may”, “should”, “expect”, “anticipate”, “outlook”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof, or variations thereon, or other comparable terminology. Investors are cautioned not to place undue reliance on such returns and statements, as actual returns and results could differ materially due to various risks and uncertainties. This material does not constitute investment advice. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. Investors should seek advice regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Investment involves risk. Market conditions and trends will fluctuate. The value of an investment as well as income associated with investments may rise or fall. Accordingly, investors may receive back less than originally invested.

Taplin, Canida & Habacht, LLC is a registered investment adviser and a wholly owned subsidiary of BMO Asset Management Corp., which is a subsidiary of BMO Financial Corp. BMO Global Asset Management is the brand name for various affiliated entities of BMO Financial Group that provide investment management and trust and custody services. Certain of the products and services offered under the brand name BMO Global Asset Management are designed specifically for various categories of investors in a number of different countries and regions and may not be available to all investors. Products and services are only offered to such investors in those countries and regions in accordance with applicable laws and regulations. BMO Financial Group is a service mark of Bank of Montreal (BMO).

BMO Asset Management Corp. is the investment adviser to the BMO Funds. BMO Investment Distributors, LLC is the distributor. Member FINRA/SIPC.

BMO Asset Management Corp., BMO Investment Distributors, LLC, BMO Private Bank, BMO Harris Bank N.A. and BMO Harris Financial Advisors, Inc. are affiliated companies. BMO Private Bank is a brand name used in the United States by BMO Harris Bank N.A.

Investment products are: NOT FDIC INSURED — NOT BANK GUARANTEED — MAY LOSE VALUE.

© 2017 BMO Financial Corp. (5720496, 4/17)