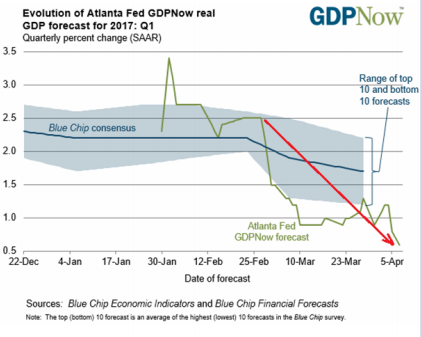

• The year has gotten off to a poor start as evidenced by the very weak Q1 GDP growth. First quarter 2017 US GDP growth was one of the weakest in the past decade.

• As was our expectation, the municipal bond market has recovered solidly since the late 2016 selloff. Munis have returned over +3.35% year-to-date.

• Our emphasis, on credit selection, across each of our strategies, is a key differentiating factor.

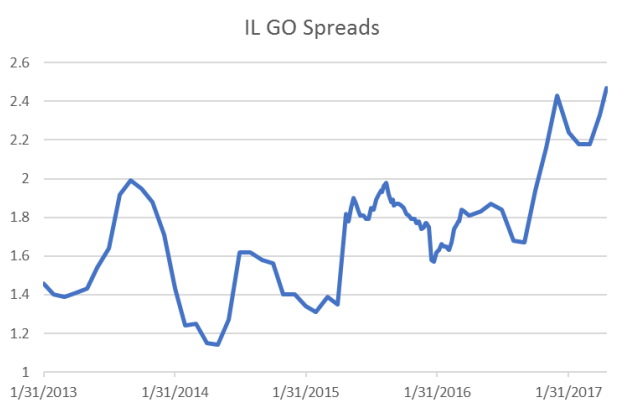

• Puerto Rico, the State of Illinois, the City of Chicago, and the State of Connecticut have seen their spreads widen materially.

• Investors have the opportunity to take advantage of some of the highest equity valuations in a generation to preserve capital by reallocating the proceeds toward municipal bonds.

• Given the attractive yields available on municipal bonds today, when compared to taxable bonds, we believe munis are positioned to outperform going forward.

“It was the best of times, it was the worst of times…” to borrow a phrase from Dickens’, Tale of Two Cities. As 2016 came to a close it seemed truly the best of times for many. Following the US election, there was renewed hope and optimism for growth initiatives, as well as public policies, which generated a sense of certainty and euphoria about the future. The expectation was that the long-beleaguered US economy would finally get up off its knees and experience renewed growth. A pro business administration and like-minded Congress were expected to act quickly on a conservative agenda based on the repeal and replacement of the Affordable Care Act, together with enactment of substantial tax reform, thereby stimulating growth and employment through private investment. As our clients and loyal readers may recall, we wrote extensively, in our December Market Commentary, about what we believed was a broad market overreaction to this perceived certainty. We discussed, in detail, the challenges of governing and the risks of future policy mistakes. We also shared our view that the market reaction could be severe should the country’s impatience surrounding the timing and scale of these initiatives devolve into disappointment and frustration. The US equity market is particularly vulnerable, in our view, as it has marched to ever greater heights, upward toward, what we believe to be, levels of significant overvaluation. Stocks clearly have not priced-in the probability that political inaction or missteps could result in significant economic stagnation or decline.

The year has gotten off to a poor start as evidenced by the very weak Q1 GDP growth, see Figure 1 below.

Figure 1

First quarter US GDP growth represented one of the weakest in the past decade. Slowing automobile sales, together with retail and restaurant industries, are facing their own sales recessions, clearly illustrating the challenges the US economy faces. Of note, the Fed has not raised interest rates with US GDP this slow since the 80’s. The Fed’s decision to pursue further tightening of financial conditions, by raising short-term interest rates, is happening at a time when US households are the most indebted they have been since 2007. This will certainly slow economic growth in the future. We, therefore, believe the probability of a US recession is increasing.

We shared, in our December 2016 Market Commentary, our expectation that the municipal bond market would recover solidly from the selloff in late 2016. Indeed it has. At the time of the writing of this commentary, munis have returned over +3.35% yearto-date, according to Bloomberg/Barclays Muni Index. Our investment strategies have benefited as well. Increasingly investors are seeking ways in which to enhance taxfree income in a low interest rate environment. Our emphasis, on credit selection, across each of our strategies is not only a key differentiating factor between ourselves and our peers, but the value we add by delivering higher tax-free income to our clients also illustrates the strength of our disciplined investment philosophy and process. For example, in recent months, our long-held decision to avoid debt backed by the Commonwealth of Puerto Rico, the State of Illinois, the City of Chicago, and the State of Connecticut has been rewarded as credit spreads have widened indicating significant and sustained credit deterioration, see IL GO spreads in Figure 2 below.

Figure 2

The credit crisis in each of these regions has continued to deteriorate causing bonds backed by these issuers to underperform dramatically. While we seek to strategically add value through credit selection, as a manager of large portions of our clients accumulated wealth, we understand fully that our clients would prefer to avoid the type of credit deterioration taking place within these select localities. For this reason, we continue to patiently monitor these situations closely as we await signs of credit stabilization.

With respect to the muni market more broadly, we were pleased that the Presidents recent outline of tax reform made no mention of munis, providing even greater confidence that concerns regarding the potential loss of municipal bond tax-exemption were significantly overstated. Therefore, given the attractive yields available on municipal bonds today, when compared to taxable bonds, we believe munis are well positioned to outperform going forward. Individual investors are being offered the opportunity to de-risk their overall asset allocations, given the meaningful overvaluation that persists in equity markets. Investors can picking up attractive tax-free/taxable equivalent returns by increasing their allocations to municipal bonds.

We remain acutely sensitive to the possibility that a growing parade of companies in the automobile, retail, and restaurant industries may begin to scale back production and lay off employees. We believe political, geo-political, and economic stresses are growing resulting in a period of increased uncertainty and volatility. The Fed is currently ill-equipped to address a significant financial crisis were one to occur in our view. Therefore, it is an appropriate time for investors to take advantage of some of the highest equity valuations in a generation in an effort to preserve capital by reallocating toward municipal bonds.

Best Regards,

Andrew Clinton

President

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Clinton Investment Management, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. The PSN universes were created using the information collected through the PSN investment manager questionnaire and use only gross-of-fee returns. The PSN/Informa content is intended for use by qualified investment professionals. Please consult with an investment professional before making any investment using content or implied content from any investment manager. advice from Clinton Investment Management, LLC. A copy of our current written disclosure statement discussing our advisory services and fees is available for review upon request.

© Clinton Investment Management, LLC

Read more commentaries by Clinton Investment Management