One of the most common questions that we’ve heard/received from clients over the past year has been our view on active versus passive management. Active management has come under significant pressure due to its underperformance relative to passive over the past few years, particularly in the very competitive US large cap space, as well as the broader theme of fee compression in the industry. This theme is well illustrated by mutual fund flows over the past couple of years. According to Morningstar, passive fund strategies in the U.S. experienced inflows of $505 billion in 2016, while active funds saw outflows of $340 billion. Will this trend continue, or will active management again have its day in the sun? (As we are an active manager ourselves, we have referenced third party consultant research for this piece).

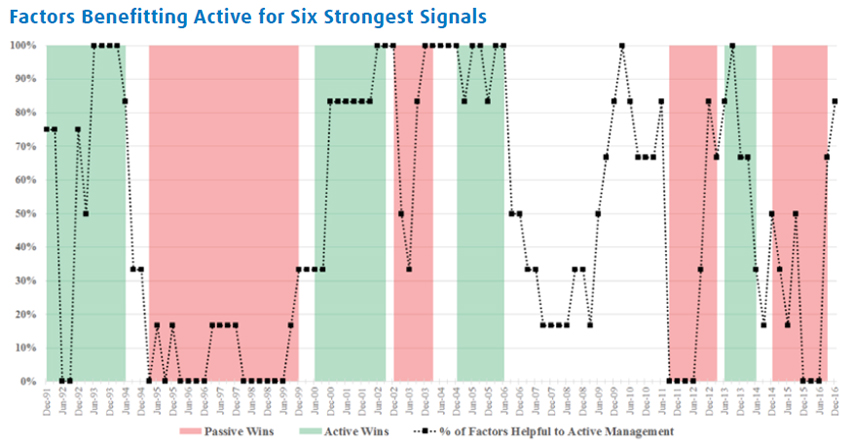

Factors Benefitting Active for Six Strongest Signals

Source: Leuthold Weeden Capital Management

What Matters in Assessment of Active vs. Passive?

There are a number of factors which tend to influence the relative performance of active vs. passive management. These factors include metrics such as the performance of U.S. small caps minus U.S. large caps (positive number typically favors active management) and the relative performance of positive earning companies minus negative earners (again, a positive number typically favors active management). The above chart from Leuthold Weeden highlights some of these factors. It is somewhat remarkable how quickly these factors have changed in favor of active management after appearing to bottom out in late 2015/early 2016. One can see from the chart that active vs. passive performance tends to be cyclical and that these cycles tend to last at least a couple of years.

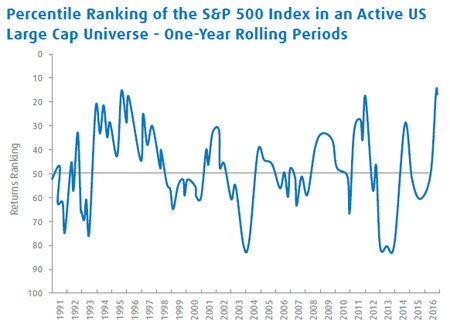

Callan Associates, a consultant, has calculated where the S&P 500 Index ranks relative to its peer group of active managers in the large cap universe on a one-year rolling basis (to illustrate, a ranking of 50 means that the S&P 500 index is right in the middle of peer returns and a ranking of 20 means the S&P 500 ranked higher than 80% of fund managers). This chart illustrates the extent to which passive management has outperformed active management over the past five years. It again shows the cyclicality of active and passive relative performance.

Source: Callan Associates

In light of all this, we advocate a thoughtful portfolio construction approach which uses a combination of active and passive. Too often, the discussion seems to be an all or nothing proposition. Active managers differ substantially in the amount of risk (tracking error) they take, turnover, cost etc. Passive funds can differ widely on cost, the index that they track, and implementation process (i.e. index replication vs. sampling). Additionally there are parts of the market where active management has proven to be able to add value and/or lower risk and different types of market environments which favor active vs. passive management.

In our multi-asset funds, we utilize a combination of active and passive management. In areas that we believe to be more efficient, such as U.S. Large Cap equities and U.S. Mid Cap equities, we tend to employ more passive exposure. While we are not confident in our ability to predict the precise timing of a “sea change” in performance between active and passive, it appears to us that many factors are lining up in favor of active management.

BMO Global Asset Management - Multi-Asset Solutions Team

Contributors:

Jon Adams, CFA, Chicago

Michael Dowdall, CFA, Chicago

Steve Bell, London

Paul Taylor, CFA, Toronto

Unless otherwise noted, all data is as of the date of publication. You should consider the Fund’s investment objectives, risks, charges and expenses carefully before investing. For a prospectus, which contains this and other information about the BMO Funds, call 1-800-236-3863. Please read it carefully before investing. BMO Asset Management Corp. is the investment adviser to the BMO Funds. BMO Investment Distributors, LLC is the distributor for the BMO Funds. Member FINRA/SIPC.. BMO Funds are not marketed or sold outside of the United States. This is not intended to serve as a complete analysis of every material fact regarding any company, industry or security. The opinions expressed here reflect our judgment at this date and are subject to change. Information has been obtained from sources we consider to be reliable, but we cannot guarantee the accuracy. This presentation may contain forward-looking statements. “Forward-looking statements,” can be identified by the use of forward-looking terminology such as “may”, “should”, “expect”, “anticipate”, “outlook”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof, or variations thereon, or other comparable terminology. Investors are cautioned not to place undue reliance on such statements, as actual results could differ materially due to various risks and uncertainties. This publication is prepared for general information only. This material does not constitute investment advice and is not intended as an endorsement of any specific investment. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. Investors should seek advice regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Investment involves risk. Market conditions and trends will fluctuate. The value of an investment as well as income associated with investments may rise or fall. Accordingly, investors may receive back less than originally invested.

Past performance is not necessarily a guide to future performance.

BMO Global Asset Management is the brand name for various affiliated entities of BMO Financial Group that provide investment management and trust and custody services. Certain of the products and services offered under the brand name BMO Global Asset Management are designed specifically for various categories of investors in a number of different countries and regions and may not be available to all investors. Products and services are only offered to such investors in those countries and regions in accordance with applicable laws and regulations. BMO Financial Group is a service mark of Bank of Montreal (BMO).

BMO Asset Management Corp., BMO Investment Distributors, LLC, BMO Private Bank, BMO Harris Bank N.A. and BMO Harris Financial Advisors, Inc. are affiliated companies. BMO Private Bank is a brand name used in the United States by BMO Harris Bank N.A. BMO Harris Financial Advisors, Inc. is a member FINRA/SIPC, an SEC registered investment adviser and offers advisory services and insurance products. Not all products and services are available in every state and/or location. All investments involve risk, including the possible loss of principal.

Securities, investment advisory and insurance products are: Not FDIC Insured – No Bank Guarantee – May Lose Value. © 2017

© BMO Global Asset Management

Read more commentaries by BMO Global Asset Management