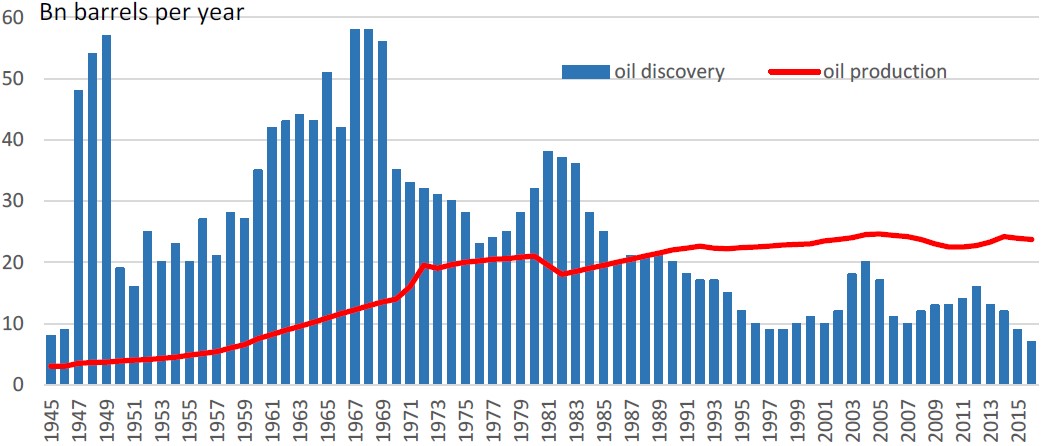

This is not a joke, but neither should you worry if you are long oil, as the price will most likely hit (at least) $100 long before it heads south, and that is due to a rising deficit between oil production and new oil discoveries (exhibit 1).

I should also point out that, strictly speaking, I should have said fossil fuels, not oil, in the headline above, but there wasn’t enough room for all those extra characters! In other words, what I meant to say is that fossil fuel (oil, gas and coal) prices will most likely approach $0 over the very long term.

Just to complicate matters even further, strictly speaking, not even that is correct. What will happen to fossil fuel prices in the future is anybody’s guess, but what almost certainly will happen at some point is that demand for fossil fuels will approach zero.

Now to why that is. To begin with, a reminder. Energy is critical to everything we humans do. Without energy, we would soon run out of things to eat; we wouldn’t be able to use our iPads – a device that appears to be more important than food to many youngsters these days – and industry would die virtually overnight. Economically, nothing is more important than energy.

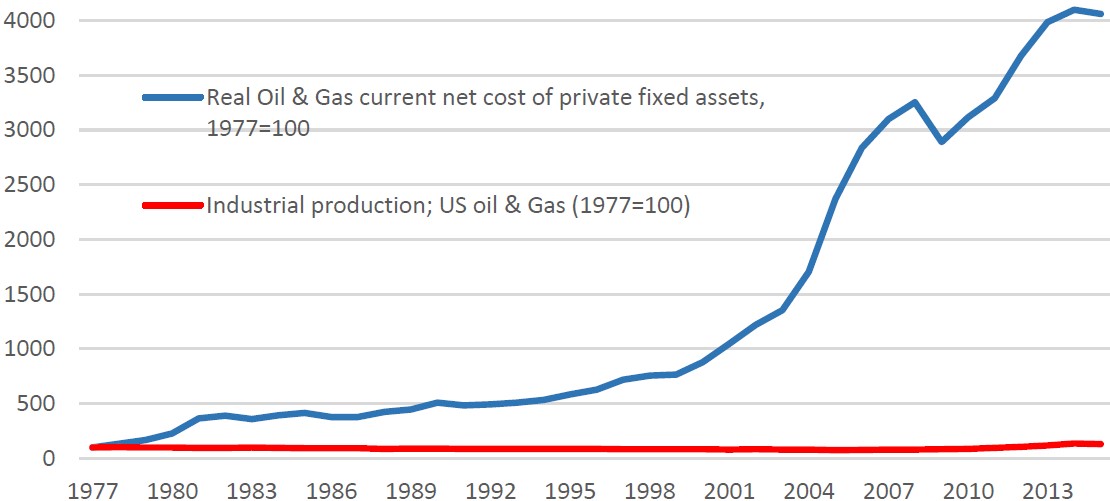

Phrased slightly differently, one could say that GDP simply cannot grow at a reasonable rate without access to energy at a reasonable cost. In that context, I note that, in the US, it requires 31 times more capital stock to extract a barrel of oil today than it did in 1977, just before ‘everything’ started to decline (exhibit 2).

What do I mean by that? Back in December last year, I first touched on the subject of declining ‘everything’. GDP growth is in decline – both in nominal and real terms – and has been in decline since the 1970s; productivity and workforce growth the same. Inflation is falling; consequently, interest rates are declining, and equity markets have also delivered more modest returns in recent years.

The problem in a nutshell

The problem in a nutshell is the geological depletion of existing fields and the growth of higher cost, geologically less attractive, fields. While drillers are more efficient today than they were, say 40 years ago, the increased share of more complex fields has dramatically increased infrastructure requirements.

Tying up so much capital in one industry has become a significant drain on productivity in other parts of the economy. That has again reduced the appetite – and the capital stock available – for energy exploration projects and, consequently, oil production has exceeded new oil discoveries for twenty consecutive years. The oil industry is quite simply doing a poor job in terms of replacing existing production. This will eventually have a major, and overwhelmingly negative, impact on GDP growth, all other things being equal.

Global oil production

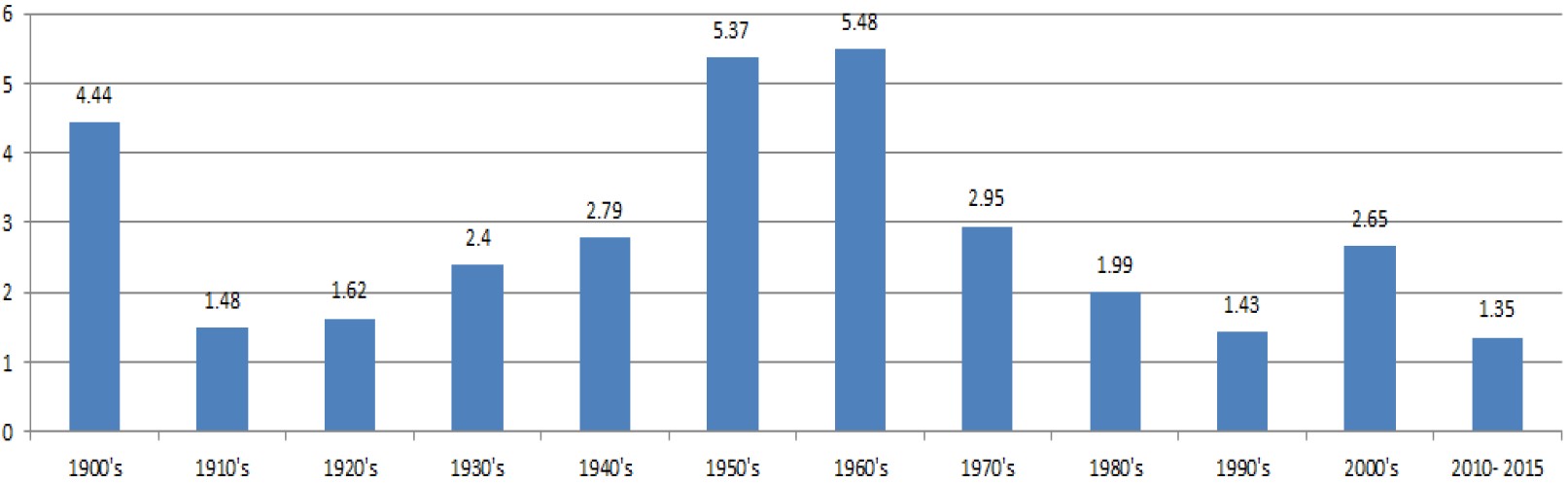

Global primary energy production has grown from 487 million tons of oil equivalents (‘mtoe’) in 1900 to 12,798 mtoe in 2015 – an annualised growth rate of nearly 3%. Behind that number hides some significant variations, though.

The growth in energy production peaked in the 1950s and 1960s and has been slowing ever since (exhibit 3). A post World War II drive away from using coal as a direct source of motive power towards using it indirectly via electricity boosted productivity – and hence GDP growth – in the 1950s and 1960s. In the decades that followed, global energy production continued to increase as the economy expanded, but at a slowing pace.

As the global economy runs out of cheap oil, shale oil is widely considered the saviour but, in the bigger scheme of things, shale’s role is limited. Despite the sharp ramp-up in oil production from shale reserves, in the six years from 2010 to 2015, the annual increase in energy production was only 1.35% – the slowest pace since the 1900s.

If one were to exclude shale, the 1.35% annualised growth rate would only drop to 0.90%, so shale’s importance shouldn’t be exaggerated. I would certainly have expected shale to have made a more significant contribution to energy production growth in recent years.

Does shale production have a future?

US shale oil production peaked in March 2015. While nearly everybody has blamed the subsequent decline in growth rates on low oil prices, there is another way to think about it. As productivity growth has flattened, so has GDP growth. The combination of low (or no) GDP growth and high (and rising) energy production costs has resulted in energy prices that are still punitively high for the global economy.

Now, consider the fact that energy is a primary driver of GDP growth – both explicitly and implicitly. The US economy has clearly benefitted from having a handful of shale oil and gas fields that have proven very productive.

However, once you move away from those 5-6 sweet spots, productivity in the US shale industry drops immensely. Not a single shale field has been identified in the last couple of years, where productivity isn’t at least 30% – and in some cases up to 90% – below that of the top shale fields in the country.

I also note that production is no longer accelerating in several of the top US shale fields. In two of the very largest ones – Bakken and Eagle Ford – growth in production began to decelerate a couple of years before oil prices collapsed in 2014. With oil prices being well over $100 when that happened, you would have thought there are other reasons behind the decelerating growth rate – not falling oil prices.

When shale first emerged as a serious contender, production costs were (in most cases) in the $80s, but they have since dropped quite dramatically. The top US shale fields are now cash flow positive when oil prices are in the low $50s, and that obviously makes the industry a more serious contender at prevailing oil prices.

However, I also note that smaller US shale fields, as well as shale fields outside the US, need much higher oil prices to prevail. At present, even the most productive non-US fields need at least $65 to break even on a cash basis – and much higher prices to break even on a total cost basis. That will most likely change over time, but the appetite to invest in shale outside the US may be limited in the short term as a result of that.

The only conclusion I can reach is that shale production won’t grow as much as (nearly) everyone expects and, consequently, it won’t necessarily provide the ‘100% rainproof’ ceiling on oil prices that is the widely perceived result of the fracking technique. I don’t expect shale to go away anytime soon, but neither do I expect it to become more than a modest factor in determining the overall balance between global supply and demand in oil and gas.

Fusion energy - a new and cheaper energy form

As I have stated frequently over the past few years, workforce growth and productivity growth are the two most fundamental drivers of GDP growth. With the outlook for workforce growth being rather pedestrian for many years to come, the only way GDP can grow at a meaningful rate is through superior productivity growth.

In other words, we need to find ways to accelerate productivity growth, and the consensus seems to be that automation will do precisely that. I am not convinced, though. Automation may lift productivity growth one or even two percentage points per year, but if you do the maths, it quickly becomes depressingly clear that an increase in productivity growth of that magnitude is not sufficient. Something far more radical needs to happen.

This is where fusion energy enters the frame. Nothing would have a bigger impact on productivity growth than virtually unlimited access to cheap energy, and that is precisely what fusion energy brings to the table. Instead of separating nuclear particles, as you do in nuclear power plants today (a technology called fission), you bring nuclear particles together, and that technology is called fusion.

Fusion is the most basic form of energy in the universe. It is what powers the sun and the stars, where energy is produced by a nuclear reaction in which two atoms of the same lightweight element, usually an isotope of hydrogen, combine into a single molecule of helium.

When mankind attempts to replicate that process, the most important ingredients are sea water and lithium, both of which are in ample supply; hence vast amounts of energy could be produced at a very reasonable cost – at least theoretically. Even better, the fusion process does not suffer from all the safety issues that accompany traditional nuclear power. So far so good, but there is a problem – and a big one at that.

Scientists can produce plenty of energy from fusion but not in a controlled way. The best example is the hydrogen bomb, where a huge amount of energy is released in a highly destructive manner. If the same amount of energy could be released gradually – in a controlled manner – we would have found the eternal solution to planet Earth’s energy requirements.

We would have virtually unlimited access to cheap fuel, and greenhouse gasses would be a thing of the past. There would be little or no nuclear waste, and productivity would rise dramatically across the world, allowing us to deal with the mountain of debt in front of us. Quite simply, the ability to commercialise fusion energy would resolve some of the biggest challenges mankind is faced with today.

Having said that, creating a controlled fusion reaction has proven very difficult. Because the nuclei have the same charge, they will electrically repel each other. To overcome the natural repulsion of the nuclei, you must give them sufficient energy. That means heating them up to about 12 million degrees but, as you heat a gas or plasma up, it expands and the atoms move further apart.

The trick is to contain the heated plasma long enough that the nuclei have the chance to collide and overcome the repulsive force. Scientists have now reached that point and have achieved energy breakeven, but there is still a long way to go before the technology can be rolled out commercially.

A race against time

As fossil fuel exploration and production ties up more and more capital, productivity growth continues to decelerate, with GDP growth ultimately turning negative. However, that is only if we cannot find a new and cheaper energy form such as fusion energy.

I am often confronted with the view that we don’t need fusion energy to fix our problems. Renewables – solar in particular – can do precisely the same. Whilst correct that greenhouse gasses will be greatly reduced as we ramp up energy production through renewables, it is still far too expensive a solution to address the productivity problem.

If governments around the world were half as smart as they claim to be, research budgets into commercialising fusion would be multiplied. It is by far the best medication for a struggling global economy, as fusion will have a much more dramatic impact on productivity and hence on GDP growth than anything automation can ever deliver.

However, it is a race against time. The global economy could quite possibly sink well before fusion reaches a state where commercialisation becomes viable – a point we won’t reach for many years. Scientists say fusion on a commercial scale is still 30 years away, but the joke is that they said exactly the same 30 years ago. Hence the need for more research resources.

Finally, before I wrap this letter up, an important point. When I say that, one day, we will no longer demand any fossil fuels, it is not entirely correct. Some residual demand for oil for various purposes (e.g. classic cars) will always exist and will probably keep oil prices above $0 for many decades, but I am sure you get my point.

Concluding remarks

As I see the landscape in front of me, as far as energy is concerned, three observations stand out:

- the world is running out of cheap oil;

- rising demand for energy from a relatively fast growing Asia can only put further upside pressure on energy prices in the short to medium term; and

- fusion energy will almost certainly become commercially viable at some point – the only question is when.

The combination of those three circumstances suggest to me that fossil fuel prices are likely to be quite volatile in the years to come. At this relatively early stage, I am reluctant to be too concise in terms of timing. I simply don’t know what will happen first. All I am convinced about is that the end result won’t be overly pleasing for fossil fuel producing nations.

For that reason, a long-only strategy in energy is entirely the wrong strategy. There will be some exceptionally high returns to be earned by being short fossil fuels at some point over the next few decades and, for that reason, I will follow the research progress on fusion energy very closely.

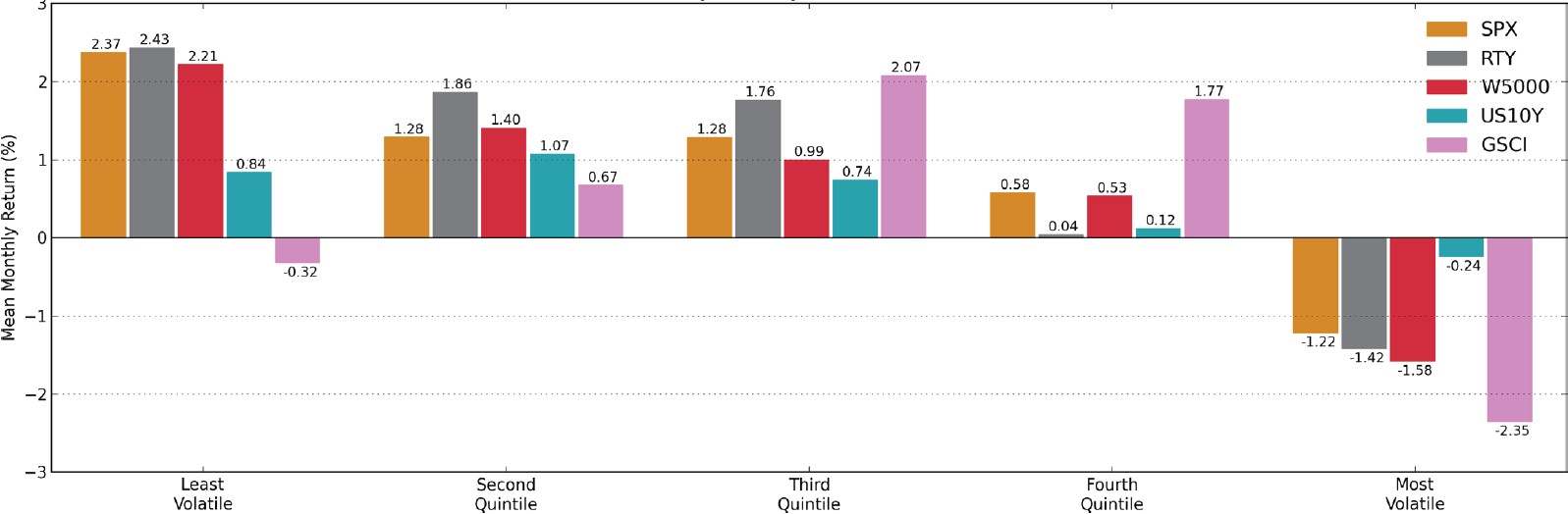

Secondly, unlike bond and equity prices, both of which do best when volatility is very low, commodity prices do quite well when volatility is above average, provided it is not exceptionally high (exhibit 4).

For all these reasons, a long/short strategy in fossil fuels ought to be a core element of your portfolio in the years to come, but you may have to take a deep breath every now and then. Nobody knows the exact timing of all of this.

© Absolute Return Partners

Read more commentaries by Absolute Return Partners