Of course, we’d argue that convertible securities are appropriate for strategic portfolio allocations, as a means of seeking lower volatility equity exposure over full and multiple market cycles.

But as interest rates rise, it’s that time in the cycle when many advisors are turning to convertibles for shorter-term tactical overweights. Convertible bonds, which combine characteristics of stocks and traditional fixed-income securities, have historically outperformed fixed income during periods of rising interest rates (see the analysis in our Readying Your Clients’ Portfolios for Rising Interest Rates post).

If you’re evaluating convertible funds now, make sure you recognize the difference between what an actively managed fund does versus a passive.

The Complexities of a Single Security and the Market as a Whole

In our view, those who seek to buy “the market” via a passive fund defeat the purpose of investing in convertibles securities. Here’s why:

- Convertibles combine characteristics of stocks and traditional fixed income securities, providing unique opportunities for managing risk and enhancing returns.

- The characteristics of a single convertible may change over time. Convertible securities have varying degrees of equity and fixed income sensitivity, and these characteristics may change for a given convertible over time.

- At various times, the convertible market as a whole—and thereby the passive fund tracking it—may look a lot like the equity market and other times a lot like the bond market.

In the image below, the first graph depicts the convertible market on March 1, 2000, as the equity market was peaking and the technology bubble was just about to burst. An investor who had favored a passive or index-like convertible strategy would have been overexposed to equity downside.

By February of 2009 (second graph), the pendulum had swung to the other extreme. As the markets troughed in the liquidity crisis, more than two-thirds of convertibles were trading as “credit-sensitive.” An investor who chose to mimic the broad market would have been positioned for limited participation in the equity market’s subsequent upside.

The third graph shows the market as of March 31, 2017, the latest data available. Here again, the market tilted more toward credit than toward equity—is that what you want at this point?

What Active Management Can Do

It's not simply the use of convertibles in a strategy that makes it work, but how convertibles are used to achieve a particular investment objective.

We believe active management is necessary in order to maximize the potential benefits of exposure to convertible securities. Passive strategies can’t adjust to changes in either an individual convertible’s characteristics or to the characteristics of the convertible universe as a whole.

A passive strategy that just follows where the market goes misses out on the opportunity that an active manager has to rebalance and optimize risk/reward.

As an active manager whose Founder, Chairman and Global CIO John P. Calamos, Sr. is generally credited for pioneering the use of convertible securities, Calamos’ focus is on trying to achieve the best possible risk-reward so we can participate in the upside of the equity market while also cushioning the downside.

In a core allocation, the most equity-sensitive convertibles may be too vulnerable over the long term to downside movements in the market. The most credit-sensitive convertibles might not provide enough opportunity for upside participation. Our objective as an active manager is to identify convertibles that offer balanced attributes, a blend of credit and equity sensitivities.

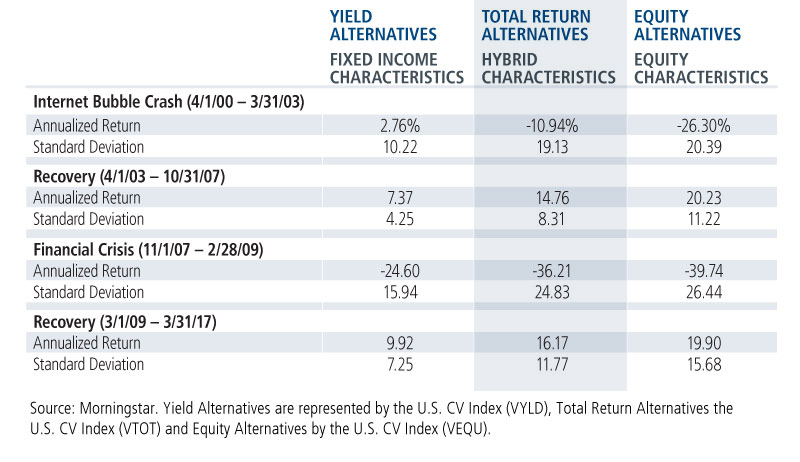

The Benefit of Balance

The table below shows the outcome—annualized returns and standard deviations—of actively optimizing for total return over several recent market cycles.

Convertibles with total return characteristics provided:

- Participation in rising equity markets

- Greater downside protection than the more equity-sensitive issues during declining markets

In short, active management of a convertible bond fund can consistently pursue total return.

© Calamos Investments

http://www.calamos.com

© Calamos Investments

Read more commentaries by Calamos Investments