Steady economic growth

The U.S. economy showed weakness in the first quarter, but that is typical in the first quarter of each year and the economy seems to be rebounding. We’re watching closely for any changes in the corporate tax structure and any indication of an infrastructure plan that could have any near-term impact. Beyond the actual passage of any legislation, we’re watching for any short-term impact on business confidence, which has been important since the U.S. presidential election last year.

Economic stimulus in China has faded somewhat as a market factor this year. That is due in part to the Chinese government trying to balance infrastructure-driven stimulus and its housing market with a restructuring of the economy, state-owned enterprises (SOEs) and commodity oriented SOEs, and lately the financials market and the “shadow banking” system in China. The government appears to be focused on balancing controls on these areas with its growth plans, and that process is worrying the markets a little now.

We added to holdings in a couple of Chinese banks in addition to a more general increase in the financial sector position. Our largest holding in China remains AIA Group Ltd., a Hong Kong-based insurance company. Overall demand for insurance products in China, Hong Kong and other Asian markets remains strong. The Shanghai government recently published a five-year plan that included a push toward increased insurance penetration there, so we believe the backdrop is good for that long-term holding in the Fund.

We have shifted more exposure in the Fund to Europe, where we still are finding pockets of relative value. We think a key question is how rapidly Europe’s economy can continue to rebound, especially if China’s economy slows a bit. More importantly, we are alert to what that may mean for the European Central Bank and its quantitative easing policy, the value of the euro versus the U.S. dollar and dollar strength in general.

A look at sectors

We have added to the Fund’s holdings in the industrials sector through a number of new positions. In the last several years, most industrials exposure was in aerospace, defense and some transportation stocks. We have broadened our exposure over the last several months, focusing on areas in which valuations have yet to discount sustained improvement. In our view, a number of large companies based in Europe that have products in multiple industries now offer a more attractive valuation while providing similar end markets and geographic exposure. We think the broader geographic and end-market mix may be useful if global economic growth becomes less synchronized in the future.

After positive performance in 2016, we think the energy sector may be settling into a consolidation phase. The Organization of Petroleum Exporting Countries (OPEC) and non-member oil producers led by Russia agreed at a meeting May 25 to extend the production cuts they agreed to last year until March 2018. The oil-producing countries seek to reduce what they consider a global glut of crude oil that has sharply pressured prices – and producers’ revenues – during the past three years. OPEC’s cuts have helped push oil above $50 a barrel this year. The price rise this year also has prompted renewed activity from U.S. shale oil producers, who are not part of the agreement to hold the line on production. We think this agreement may allow the energy sector to find a price bottom and start to consolidate.

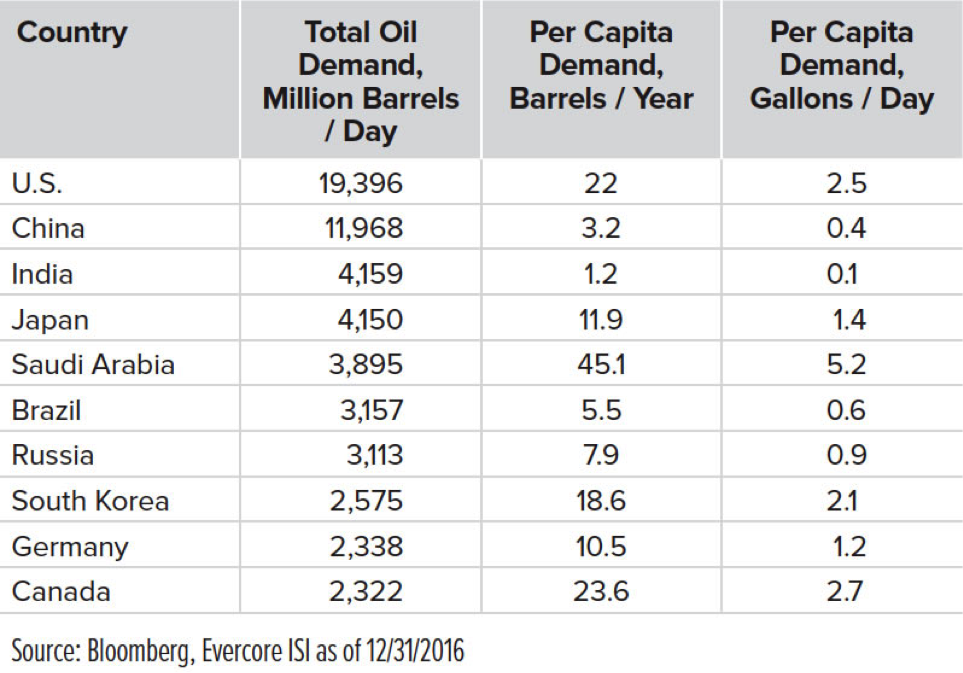

What happens when consumers in China and India demand more oil?

Our strategy still is to focus on what we consider high-quality, low-cost companies. We continue to favor the large oil services companies that can grow earnings through volume growth, pricing increases and high incremental margins. In general, we think crude oil is likely to remain around $55 per barrel for an extended period.

The Fund’s primary exposure in the energy sector has been through the North American exploration and production (E&P) companies. We look for companies that have good exposure to the key resource areas, particularly the Permian Basin. We also look for the operators that have low costs and the ability to develop those resources. We think those factors are key in an environment that has an inventory overhang that may take time to fully resolve. That adds to the focus on companies that can continue to get growth production in a low-price environment.

We have maintained the Fund’s exposure to the two largest oil services companies, Halliburton Co. and Schlumberger Ltd. These companies had to give up pricing during the financial downturn. As activity increases, we think they will be able to increase prices and growth.

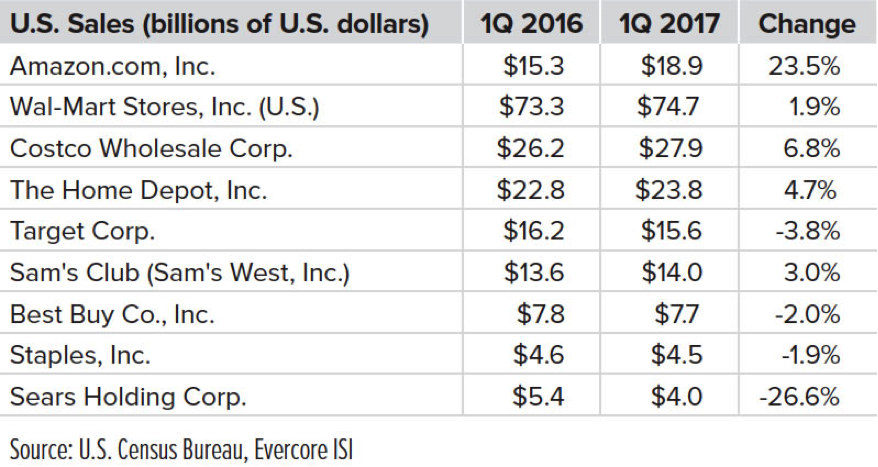

In retail, we believe disruption will continue from online, mobile e-commerce businesses. That clearly is reaching critical levels in the U.S. but also is gaining acceptance even in emerging markets. Disruptors in the portfolio include Amazon, Inc., Alibaba Group Holding Ltd. and MercadoLibre, Inc. The last two have the added benefit of low penetration rates in China and Latin America, which leads us to believe there still is a long fairway of potential opportunities.

Amazon captured nearly one-quarter of recent retail sales growth

The composition of the Fund’s portfolio looks a bit different when compared with holdings in late 2016. We have increased the allocation to domestic equities to nearly 54% of assets and international equities to 20%. We reduced the gold allocation from 8% to 5%. We also have made changes in the fixed income components of the portfolio. We rotated from about a 7% allocation to U.S. Treasuries into a 3.5% position in Treasury Inflation Protected Securities; moved to nearly 7% in emerging markets sovereign debt, specifically in Mexico and Brazil; and reduced the corporate bonds allocation to nearly 9.5%. The large changes in the corporate bond and equity allocations primarily are because of the transaction related to the Fund’s Formula One holdings, as described below.

Update on private investments

During the past seven quarters, we have had opportunities to manage down the size of the illiquid private investments held by the Fund. The private investments have become less of a performance headwind recently, compared with prior quarters. A key positive development was related to our largest illiquid private investment, the equity and loan notes issued by Delta Topco Limited, the parent company of Formula One.

The acquisition of Delta Topco Limited by Liberty Media Corporation was announced in the third quarter of 2016 and the acquisition closed early in 2017. The Fund received a combination of cash, approximately $55 million in principal amount of exchangeable redeemable loan notes due July 23, 2019, issued by Delta Topco Limited and restricted shares of Liberty Media Corporation’s Series C Liberty Formula One non-voting common stock (FWONK). On May 24, 2017, we had the opportunity to sell about one-half of the Fund’s total position in FWONK shares.

This year, we also sold our private investment in Ithaca Holdings, LLC, a worldwide music management business, which is one of the underlying positions within Series I of Media Group Holdings, LLC. The remaining private investments within Media Group Holdings, LLC now comprise less than 1% of the Fund’s assets under management.

Past performance is no guarantee of future results. The opinions expressed are those of the Fund’s managers and are not meant as investment advice or to predict or project the future performance of any investment product. The opinions are current through May 2017, are subject to change at any time based on market and other current conditions, and no forecasts can be guaranteed. This commentary is being provided as a general source of information and is not intended as a recommendation to purchase, sell, or hold any specific security or to engage in any investment strategy. Investment decisions should always be made based on an investor’s specific objectives, financial needs, risk tolerance and time horizon.

Diversification does not guarantee a gain or protect against loss in a declining market. It is a method to reduce risk.

Top 10 Equity Holdings as a percent of net assets as of 04/30/2017: Liberty Media Corp., Class C, 6.04%; JPMorgan Chase & Co., 2.36%; Microsoft Corp., 2.09%; Kraft Heinz Co., 2.04%; Citigroup Inc., 1.96%; Philip Morris International, Inc., 1.90%; Adobe Systems, Inc., 1.77%; AIA Group Ltd., 1.73%; Halliburton Co., 1.64%; Pfizer, Inc., 1.63%.

Risk factors: The value of the Fund’s shares will change, and you could lose money on your investment. The Fund may allocate from 0 to 100% of its assets between stocks, bonds and short-term instruments of issuers around the globe, as well as investments in precious metals and investments with exposure to various foreign securities. International investing involves additional risks, including currency fluctuations, political or economic conditions affecting the foreign country, and differences in accounting standards and foreign regulations. These risks are magnified in emerging markets. Fixed-income securities are subject to interest-rate risk and, as such, the net asset value of the Fund may fall as interest rates rise. Investing in high-income securities may carry a greater risk of nonpayment of interest or principal than higher-rated bonds. The Fund may focus its investments in certain regions or industries, thereby increasing its potential vulnerability to market volatility. The Fund may seek to hedge market risk on various securities, increase exposure to various markets, manage exposure to various foreign currencies, precious metals and various markets, and seek to hedge certain event risks on positions held by the Fund via the use of derivative instruments. Such investments involve additional risks, as the fluctuations in the values of the derivatives may not correlate perfectly with the overall securities markets or with the underlying asset from which the derivative’s value is derived. Investing in commodities is generally considered speculative because of the significant potential for investment loss due to cyclical economic conditions, sudden political events, and adverse international monetary policies. Markets for commodities are likely to be volatile and the Fund may pay more to store and accurately value its commodity holdings than it does with the Fund’s other holdings. These and other risks are more fully described in the Fund’s prospectus. Not all funds or fund classes may be offered at all broker/dealers.

Read more commentaries by Ivy Investments