Friday’s eye-opening decline in the strongest gainers for 2017 has many people wondering:

Is it time for new market leadership?

Last Week Recap

The big news last week was the Comey hearing and speculation about what it meant. Markets have not been reacting to the political news, but it still commands media attention. CNBC provided non-stop coverage.

The punditry did spend time on my question from last week – bonds versus stocks – but seemed happy to turn to the action on Friday instead.

The Story in One Chart

I always start my personal review of the week by looking at this great chart from Doug Short via Jill Mislinski. The loss for the week was only 0.3%, but Friday’s trading added some excitement to a slow, summer Friday afternoon.

Doug has a special knack for pulling together all the relevant information. His charts save more than a thousand words! Read the entire post for several more charts providing long-term perspective, including the size and frequency of drawdowns.

Note to Readers

Thanks to all of those who offered suggestions for changes in WTWA and encouragement about my main mission. There are many great ideas that I am trying to implement and many loyal readers who like things as they are. Here are the changes so far:

- Eliminating much of the material repeated every week and placing it in a static source. I need to find a good way to encourage new readers to check out the background.

- Reducing the calendar to summarize my own views on what is most important.

- Moving the Silver Bullet to a standalone series. I am trying to make it more visible, not diminishing the importance. I realize that this is a bit less convenient for current leaders, but I hope they will help me out in establishing this.

- Moving the trading ideas to the Stock Exchange series. Once again, please read and give this a chance. WTWA readers must be aware of the different time frame.

- Changing the emphasis of the weekly theme to what I see as more important, with secondary consideration to media attention.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

The economic news last week was mixed, but the market reaction was positive.

The Good

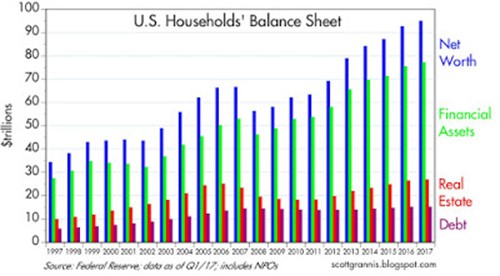

- Household balance sheets show new records in wealth in nominal, real, and per capita terms. (Scott Grannis).

- Rail traffic improved in May. (Calculated Risk). (See also Steven Hansen at GEI).

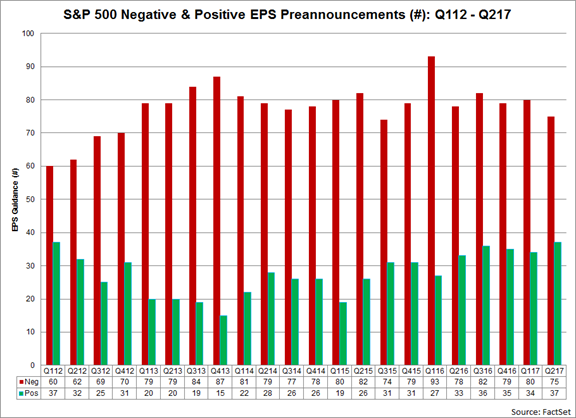

- Earnings announcements are the most positive since 2012. (FactSet). (Brian Gilmartin).

- ISM services registered 56.9. The strong value beat expectations. There was also strength in employment, business activity, and new orders. (ISM).

- Commercial real estate is looking stronger according to the Dodge Momentum Index. This is claimed to be a leading indicator. See Calculated Risk for analysis and charts.

The Bad

- Little progress in the debt ceiling debate.

- Factory orders dropped 0.2%, the first decline in five months. (Reuters).

- Wholesale sales declined to levels usually associated with recessions. (Steven Hansen at GEI). The lower inventories are also likely to affect Q2GDP.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

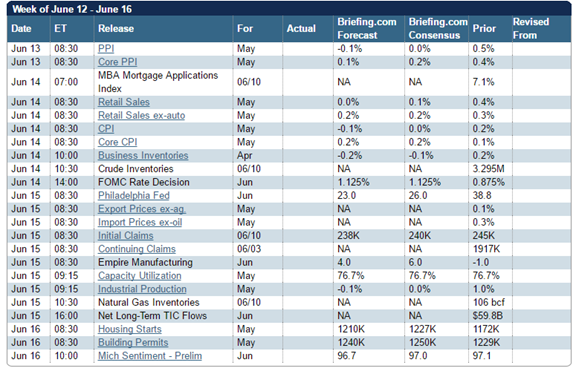

The Calendar

It is a fairly light calendar. The FOMC meeting will be most important for markets – especially the press conference. Watch for hints about future policy and a resulting change in the slope of the yield curve. There will be some FedSpeak in the days after the meeting.

I am also interested in building permits

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

The Fed decision will be a popular topic, but the week will begin with a deeper look at Friday’s trading. People will be asking:

Is there a change in market leadership?

Here some of the early explanations:

-

The FANG stocks were dramatically over-valued. A shift was long overdue. Anything might have started it.

-

The Amazon crash captured the attention of the CNBC crew, where they cited the rapid decline in a major name. The focus was mostly on Amazon, but partly on retail strength.

-

The rapid selling is evidence of inherent danger in the current market. Flash Crash redux.

-

Overall, the change in the major indexes was not that great. The differential effects happened too quickly to be called a rotation, but could it be the start of one?

Whatever the reason, it was not just a flash crash in AMZN.

As usual, I’ll have more in my Final Thought. I have an unprovable, but plausible hypothesis. It fits the evidence and timing from the chart above.

Quant Corner

We follow some regular featured sources and the best other quant news from the week.

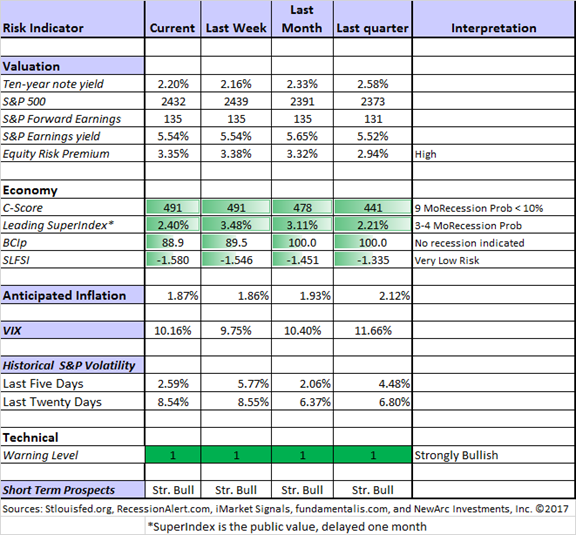

Risk Analysis

I have a rule for my investment programs. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

The Indicator Snapshot

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score.

RecessionAlert: Strong quantitative indicators for both economic and market analysis.

Georg Vrba: Business cycle indicator and market timing tools.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

Doug Short: Regular updating of an array of indicators. Great charts and analysis.

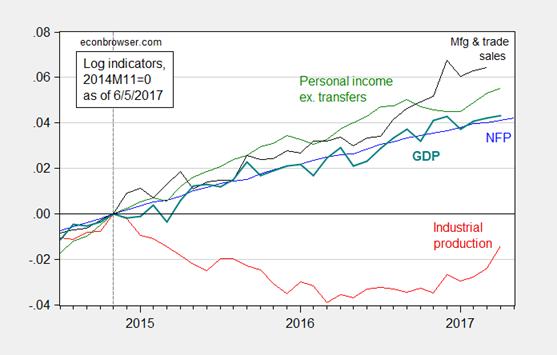

Wisconsin economist Menzie Chinn (Econbrowser) Has his own helpful variant of the Big Four chart we often show here. He sees slowing growth, but no sign of a recession.

Insight for Investors

Investors should have a long time horizon. They can often exploit trading volatility!

Best of the Week

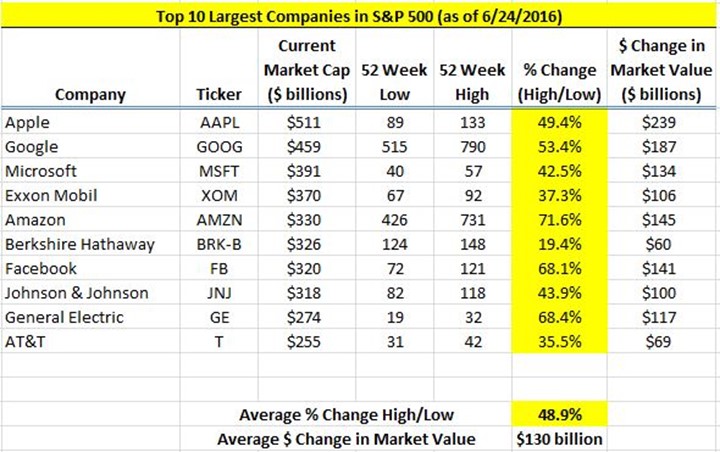

If I had to pick a single most important source for investors to read this week it would be David Van Knapp’s comprehensive and thoughtful response to investors who buy good companies without regard to price.

He does a nice introduction and valuation. He explains that valuation affects probability, not certainty. And he uses some great examples. He explains that markets are not efficient, despite what you learn in school. He illustrates with another good example.

Especially devastating is his refutation of the facile and self-serving argument that has gained recent popularity: large cap stocks are never mispriced because markets are so efficient. He writes:

…the idea that large-cap stocks are never mispriced ignores the data. It is clear that even the largest companies go through periods of mispricing. The following table shows the differences between the 52-week highs and lows for the biggest members of the S&P 500 right after the Brexit vote last June.

My summary cannot do justice to this fine work. Read it carefully. Read it twice!

Stock Ideas

Brian Gilmartin reviews the pluses and minuses for GE, including both fundamental and technical analysis. He notes the importance of the upcoming earnings report, and the attractions of a dramatic alternative for those with a growth portfolio.

Chuck Carnevale explains that attractive valuation based upon earnings is just a starting point – a way to avoid mistakes. As usual, he provides a helpful specific example.

Blue Harbinger analyzes closed-end funds, with special attention to risk. Mark produces a few ideas worth consideration.

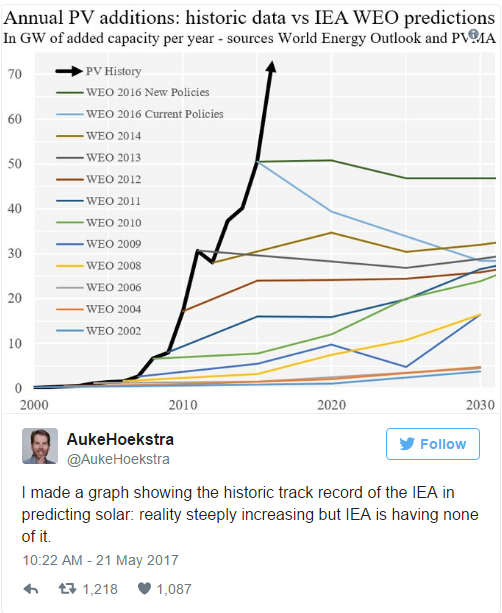

Business Insider highlights an interesting chart from Twitter. It shows the lagging expectations for solar energy growth.

Subscription Sources

I read these sources, sharing a touch of the content so that you can decide whether to buy an issue yourself.

Barron’s has even more stock information than usual. It is the mid-year roundtable issue with ideas from nine participants. There are also interesting articles on energy stocks, tech stocks, and emerging market ETFs.

Personal Finance

Abnormal Returns always has first-rate links for investors. Once a year he takes a well-deserved vacation and substitutes a series of stimulating questions posed to the financial blogging community. I always appreciate being part of this project, and I give special thought to my answers. Looking at this year’s results, I see that my colleagues have done the same. You will find plenty of good advice.

Seeking Alpha Senior Editor Gil Weinreich reads extensively and has a great imagination. Nearly every day the raises an interesting topic for advisors and investors alike. This week I thought his discussion of financially fair divorce and divorce software was especially interesting.

[Mrs. OldProf wandered into my home office as I was doing this research and started scowling. Mystified by this, and eventually figuring out the problem, I explained that my reading was professional research, not personal. Her normal cheerful smile returned. There is a lesson there somewhere.]

Market Outlook

Fear and Greed Trader has another nice market summary. Especially helpful is his analysis of the recent claims of market skeptics. He also identifies some sectors that are benefiting from the rotation that is this week’s theme.

Watch out for….

Those turning good news into bad. Charlie Bilello joins in on one of my favorite topics. He lists many things that you might consider as part of the perfect market environment:

The following attributes might come to mind:

1) High returns with low volatility and 2) low drawdowns, with 3) global participation, 4) both stocks and bonds rising, 5) the economy expanding, 6) earnings growing, and 7) an easy Central Bank.

Sound too good to be true? Let’s take at where we are today…

He follows this introduction with a data-filled answer to each question. He then answers the key question: Is this as good as it gets?

I don’t know, but for investors it’s pretty darn close. The challenge, as we know from history, is that just because something is really good doesn’t mean the next stage has to be really bad. If it were, the game would be easy. You would just sell everything today and wait until everything is really bad next month to buy everything back at a lower price.

But that’s not how the market works. Most of the time, really good environments continue to be good for some time and even when they’re less good, they’re still ok. And importantly, investors can still make money in the transition from really good to ok.

Final Thoughts

Not every market ripple needs an explanation, but Friday’s trading was pretty interesting. None of the TV pundits had a good explanation. Here is what I observed:

Not much was happening; it was a typical, quiet summer Friday. I noticed a decline in Nvidia (NVDA), a company featured on the Stock Exchange a few weeks ago. It has been a profitable trade, and we still hold it in some programs. Since the decline was 10% or so in a few minutes, there must be some news. Checking out my sources I learned that a negative report had been issued by Citron Research, a noted short-seller. CNBC caught up with this, and invited Citron’s CEO to participate in the discussion. Jim Cramer and Josh Brown, both NVDA fans, were also part of the impromptu debate. One question was why Citron picked this particular moment for the report. The (rather lame) answer was “valuation” and some colorful analogies. There was no fresh news. Within a short time, the entire tech sector was selling off hard.

I remarked to my team that this was a pretty safe way to make money. You get really short, and maybe inform some friends about your plan. You write a report, release it, and your pals give it exposure. A slow Friday afternoon is a perfect time. You go on TV. As the stock craters, you cover your shorts and enjoy the weekend, having made a lot of money in a couple of hours.

This is a completely legal business model, if the reports are factual. By coincidence, Jesse Barron has a feature on The Bounty Hunter of Wall Street in this week’s New York Times Magazine. It features Andrew Left, the Citron CEO. I strongly recommend that you read it and study the examples. Compare them to Friday’s events.

What can you do to protect yourself? As I have often said, do not use stop orders that become market orders when your price is touched.

Does this mean new leadership for the market? We’ll have a better idea soon, but it is something important to watch.

What worries me…

- Lack of compromise in government. Many believe that gridlock is good. Not so. We will need bi-partisan compromise to deal with the big issues like growing government debt and entitlement programs.

- Growing tension with Russia, and within Russia.

…and what doesn’t

- The idea of a “complacent” market. It is a poor description. We have a balance of widely divergent opinions and ideas. A stalemate – at least for now.

- The Fed decision. We are far from the point when these rate hikes will make a difference. (See analysis by Fed expert Tim Duy).

© New Arc Investments