Rick provides his take on the Fed’s most recent rate hike and makes the case against an overly rigid view of price change.

The Federal Reserve (Fed) last week proceeded with policy normalization as we expected, raising rates by 0.25%. The Fed’s policy move was fully justified, in our view, despite some of the handwringing regarding rate increases from many market commentators focusing on another weak inflation print.

We believe the central bank’s employment and inflation mandates are effectively accomplished at this stage, when viewed in the proper forward-looking context. Monetary policy is supposed to be forward looking and not overly focused on short-term transitory, seasonally weak data.

It’s also important to recognize that this Fed is normalizing rates from excessively low levels with a keen eye on adjusting the path if U.S. inflation disappoints further. The Fed rightly recognized some of the softness in recent top-line and core inflation (as measured by today’s traditional metrics) and made it clear it will respond accordingly going forward.

Yet we believe the excessive obsession some market watchers have with the Fed hewing to its 2% inflation target is shortsighted. Here’s the truth about the Fed and inflation: The Fed adopted its 2% inflation target only quite recently, in 2012. Prior to that, the central bank was comfortable with an inflation level slightly lower than 2% and looked past the small variations around its previously preferred target range.

Today, massive technological disruptions and long-term demographic trends are remaking the inflation landscape, and we believe both investors and policy makers need to abandon an overly rigid view of price change.

Historically, technological innovation has proved to be deflationary, exerting downward pressure on prices. This is evident in the chart below, showing the drastic drop in computing and storage costs over the last 60 years. Based on the chart below, an iPhone in 1991 storage and computing cost dollars would be worth $1.44 million—per phone. An iPhone today costs a miniscule fraction of that.

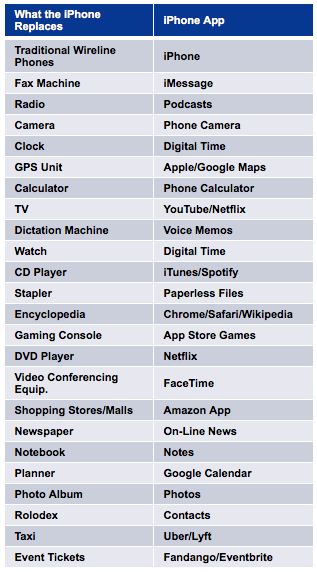

Technological innovation is disrupting traditional business models of many industries, putting a lid on prices and influencing inflation in the economy overall. Just consider some of the industries the iPhone and its associated apps have disrupted:

We believe technology’s downward pressure on prices is partly behind recent soft Consumer Price Index (CPI) readings. We have witnessed a precipitous decline in wireless service prices lately, as firms compete fiercely for customers and introduce “unlimited data” calling plans to gain, or maintain, market share. Remarkably, this has resulted in a near 13% year-over-year decline in wireless telephone services prices, which at the margins is weighing on recent CPI readings. See the chart below.

Clearly, we will want to carefully scrutinize future CPI data releases, as technology-influenced factors are likely to continue to serve as a disinflationary headwind to overly rapid increases in the aggregate price level.

The world’s aging population, meanwhile, is likely to keep growth—and inflation—lower than they have been in the past. Aging populations generally draw more from the economy than they contribute to it.

Inflation, and how it impacts consumption and investment, varies radically by industry (consider the price deflation in food, apparel, transportation costs, etc. versus the persistently stable to rising inflationary dynamics in services). And yet perhaps unhelpfully, the Fed’s 2% mandate is directed toward system-wide price stability. This is an increasingly challenging paradigm to execute upon today in the more modern commerce era we live in.

Going forward, in order to understand the appropriate long-term levels of rates and inflation, policy makers and investors will need to focus on the big-picture trends transforming the inflation landscape. In the meantime, global financial conditions remain highly accommodative, the Fed’s latest move made sense, and we believe the U.S. economy will handle this policy transition quite well.

Rick Rieder, Managing Director, is BlackRock’s Chief Investment Officer of Global Fixed Income and is a regular contributor to The Blog.

© BlackRock

© BlackRock

Read more commentaries by BlackRock