|

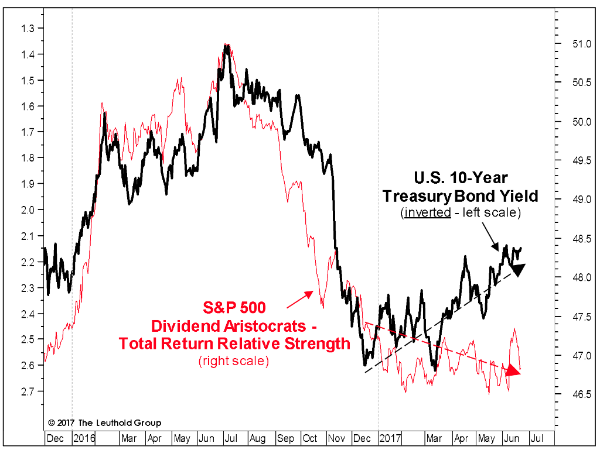

One of this year’s many perplexing leadership trends has been the weak relative action of the once-coveted S&P 500 Dividend Aristocrats in the face of a solid bond market rally. We certainly aren’t complaining, since we’ve been highlighting the valuation risks embedded in these bond-like stocks for what seems like forever, and have very little exposure to them in our managed accounts. But we’d have expected the nearly half-point drop in the 10-year Treasury yield since mid-December to have generated a much stronger bid for the Aristocrats than seen YTD.

We’re always intrigued when a longstanding market relationship, like the one pictured, begins to break down. Capitalizing on that breakdown can be quite another thing, however. One must first assume that the relationship will eventually reassert itself. The investor must then correctly choose among the two diverging data series. If, in this instance, the bond market proves more accurate in its assessment of the world, the Aristocrats should rally sharply (at least on a relative basis) to close the performance gap that’s recently opened up. If investors in bond-like stocks are instead the prescient ones, then bond yields should rally back to the peaks made in mid-December and again in mid-March.

In recent months, we’ve discussed a comparable performance divergence between Energy stocks and crude oil, arguing that the collapsing relative strength of the Energy sector foreshadowed another downswing in the underlying commodity. That proved on the mark. In this case, despite the popular market maxim that “bond investors usually get it right,” we’ll side again with the equity investors—expecting that the performance gap will be closed by rising bond yields. (And if we’re right, owning the Aristocrats won’t be a pleasant experience, either.)

© 2017 The Leuthold Group

|

|

|

Read more commentaries by The Leuthold Group