Valuations and regulations are among the trends that we’re watching in this industry

Bank stocks have spun their wheels for most of 2017. Year to date through June 9, the KBW Bank Index (BKX) had risen 3.03% compared to 9.61% for the S&P 500 Index. Banks fizzled as the reflation trade faded and the outlook for fiscal stimulus and meaningful regulatory changes was delayed by the political situation in Washington, DC. However, I believe the banking industry may warrant another look for three reasons:

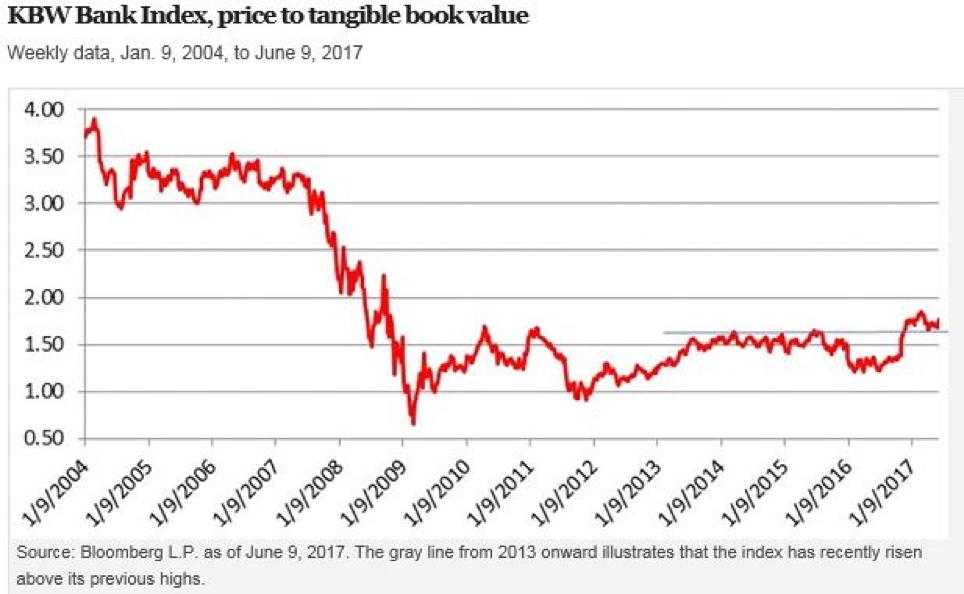

1. Banks are still inexpensive, while regulation may be slowly loosening

Large banks remain inexpensive in a market focusing more closely on stretched valuations. Although a return to the pre-financial crisis valuation high is not expected, the BKX was trading at 1.76x tangible book value in the week ended June 9, and had recently crossed above the post-financial crisis highs before settling back to hold the old highs established between 2014 and 2015.1 It has been trading at a near 50% discount to its pre-financial crisis price-to-tangible-book ratio of 3.51.1 In contrast, the S&P 500 Index was trading at 8.78x tangible book value and trading 35.6% above the Oct. 2007 pre-financial crisis valuation high.1

There is a chance for bank valuations to expand as the regulatory environment eases. The Treasury Department’s banking regulation plan released June 12 appeared to be well-received by Wall Street analysts, stoking hopes that banks might be able to more efficiently utilize their balance sheets and improve returns on capital. Moreover, the Treasury Department’s plan came on the heels of the House of Representatives passing the Financial CHOICE Act, which is a roll back of the Dodd-Frank financial regulations.

The BKX’s return on equity was about 8.5%, on June 9, 2017, compared to a peak just over 16.0% in February 2007 prior to the crisis.1 A return to 2007 return on equity levels is unlikely, in my view, but I see room for expansion in a looser regulatory environment.

2. Loan growth may be bottoming

One headwind to banking sector returns has been a slowdown in lending. Some of the weaker growth is related to tough year-ago comparisons, but a second factor is a function of weaker economic activity in 2015 and early 2016.

Loan growth was occurring at a double-digit pace in the first half of 2016 before tailing off and recently marking a lull of just 2% year-over-year in May.1 As 2017 progresses, I expect those year-over-year comparisons to look more favorable and help support the growth rate. More importantly, history suggests that the ISM Manufacturing Index can lead loan growth by roughly one year, as shown in the chart below. The index hit a relative low in August 2016 at 49.6 and rose to a recent peak of 57.7 in February 2017 before trending sideways to slightly lower in recent months.

3. Mean revision in Treasury market volatility could potentially improve trading profits:

Volatility in the Treasury market, measured by standard deviation, has been historically low and a drag on trading profits. As shown below, the Merrill Lynch Option Volatility Estimate (MOVE) Index finished the week ended June 9 at 52.55. It has seen these levels just 1.4% of the time on a weekly closing basis since Jan. 5, 1990.1

On May 31, both JP Morgan Chase and Bank America noted that second-quarter trading revenues would be hurt by calm markets. A lift in volatility is possible not only on a mean reversion basis, but as the debate over the Federal Reserve unwinding its balance sheet heats up and the European Central Bank looks to end its quantitative easing program with signs of improved economic growth in Europe.1 Additionally, over the past 20 years, there has been a positive relationship between increased Treasury market volatility and rising 10-year Treasury yields.2 Bank shares tend to display strength during periods of rising interest rates.3

A risk to watch

One risk to the value factor and higher bank valuations may rest in low inflation. The Consumer Price Index excluding food and energy has declined from a recent year-over-year peak of 2.3% to 1.7% in May.1 The decline has been driven by motor vehicles, apparel, and household furnishings and operations. Low inflation is a dynamic that could cap long-term interest rates and flatten the yield, while suppressing excitement over a reflation trade.

ETFs of interest

Investors interested in exposure to banks may want to explore the PowerShares KBW Bank Portfolio (KBWB) or examine the PowerShares S&P 500 Value Portfolio (SPVU). SPVU has nearly 23% exposure to banks and nearly 40% exposure to financial shares as of June 14, 2017.

1 Source: Bloomberg L.P., data as of June 9, 2017

2 Source: Bloomberg L.P., data from June 14, 1997, to June 13, 2017. The correlation between Treasury volatility (the MOVE Index) and the 10-year Treasury yield was 0.19, and the beta of a regression was 0.09, with a t-test of 6.26.

3 Source: Bloomberg L.P., data from June 14, 1997, to June 13, 2017. The correlation between bank stocks (BKX Index) and the 10-year Treasury yield was 0.297, and the beta of a regression was 0.32, with a t-test of 10.03.

Nick Kalivas

Senior Equity Product Strategist

PowerShares by Invesco

Nick Kalivas is a Senior Equity Product Strategist representing the PowerShares family of exchange-traded funds (ETFs). In this role, Nick works on researching, developing product-specific strategies and creating thought leadership to position and promote the smart beta* equity line up.

Prior to joining Invesco PowerShares, Mr. Kalivas spent the majority of his career in the futures industry, delivering research, strategy and market intelligence to institutional and high net worth clients centered in the equity and interest rate markets. He was a featured contributor for the Chicago Mercantile Exchange, and provided research services to a New York-based global macro commodity trading advisor where he supplied insight on equities, fixed income, foreign exchange and commodities. Nick has been quoted in the Wall Street Journal, Financial Times, Reuters, New York Times and by the Associated Press, and has made numerous appearances on CNBC and Bloomberg.

Nick has a BBA in accounting and finance from the University of Wisconsin – Madison and an MBA from the University of Chicago Booth School of Business with concentrations in economics, finance, and statistics. He holds the Series 7 and Series 63 registrations.

*Beta is a measure of risk representing how a security is expected to respond to general market movements. Smart beta represents an alternative and selection index based methodology that may outperform a benchmark or reduce portfolio risk, or both.

Important information

Blog header image: Who is Danny/Shutterstock.com

Past performance is not a guarantee of future results.

The KBW Bank Index is a float-adjusted, modified-market-capitalization-weighted index that seeks to reflect the performance of publicly traded companies that do business as banks or thrifts in the US. An investment cannot be made into an index.

Correlation is the degree to which two investments have historically moved in relation to each other.

Reflation refers to a monetary policy intended to curb the effects of deflation. The reflation trade refers to the practice of investors looking to buy value and cyclical stocks in an effort to benefit from periods of strengthening economic growth, rising inflationary pressures and increasing interest rates.

Tangible book value is a company’s total assets minus liabilities and intangible assets.

Price-to-tangible-book ratio compares a company’s stock price with its tangible book value.

Return on equity (ROE) is a measure of profitability, calculated as net income as a percentage of shareholders’ equity.

The ISM Manufacturing Index, which is based on Institute of Supply Management surveys of more than 300 manufacturing firms, monitors employment, production inventories, new orders and supplier deliveries.

The Consumer Price Index measures change in consumer prices as determined by the US Bureau of Labor Statistics.

Volatility is a statistical measurement of the magnitude of up and down asset price fluctuations over time.

Standard deviation measures a portfolio’s or index’s range of total returns in comparison to the mean.

T-test: After an estimation of a coefficient, the t-statistic for that coefficient is the ratio of the coefficient to its standard error. That can be tested against a t distribution to determine how probable it is that the true value of the coefficient is really zero. A value over the absolute value of 2.0 is seen as statistically significant.

Regression is a statistical measure that attempts to determine the strength of the relationship between one dependent variable and a series of other changing variables. Regression helps investment and financial managers to value assets and understand the relationships between variables.

The Merrill Lynch Option Volatility Estimate (MOVE) Index is a yield curve weighted index of normalized implied volatility on one-month Treasury options.

There are risks involved with investing in ETFs, including possible loss of money. Shares are not actively managed and are subject to risks similar to those of stocks, including those regarding short selling and margin maintenance requirements. Ordinary brokerage commissions apply. The fund’s return may not match the return of the Underlying Index. The fund is subject to certain other risks. Please see the current prospectus for more information regarding the risk associated with an investment in the fund.

Investments focused in a particular industry, such as banking, are subject to greater risk and are more greatly impacted by market volatility, than more diversified investments.

The funds are non-diversified and may experience greater volatility than a more diversified investment.

A value style of investing is subject to the risk that the valuations never improve or that the returns will trail other styles of investing or the overall stock markets.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC, investment adviser. Invesco PowerShares Capital Management LLC (PowerShares) and Invesco Distributors, Inc., ETF distributor, are indirect, wholly owned subsidiaries of Invesco Ltd.

©2017 Invesco Ltd. All rights reserved.

Three reasons to consider bank stocks by Invesco