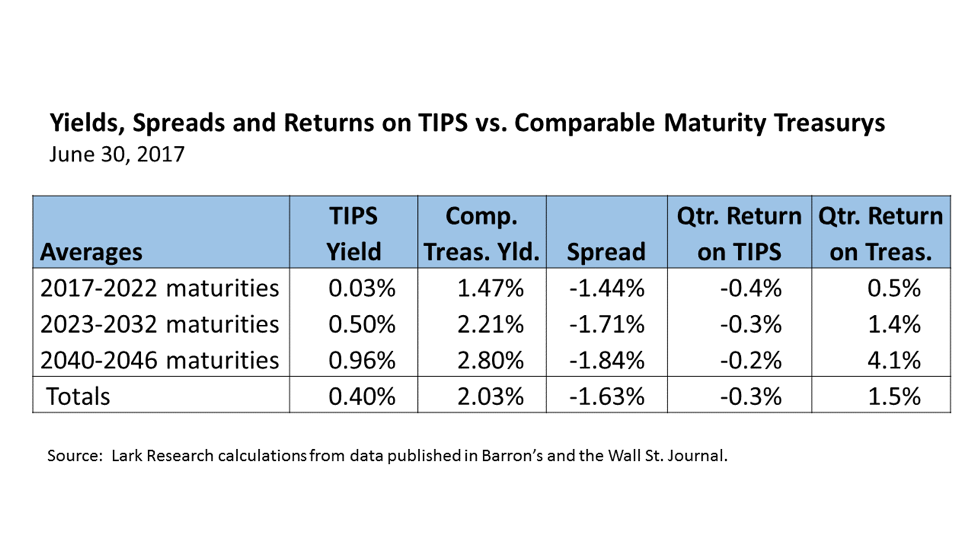

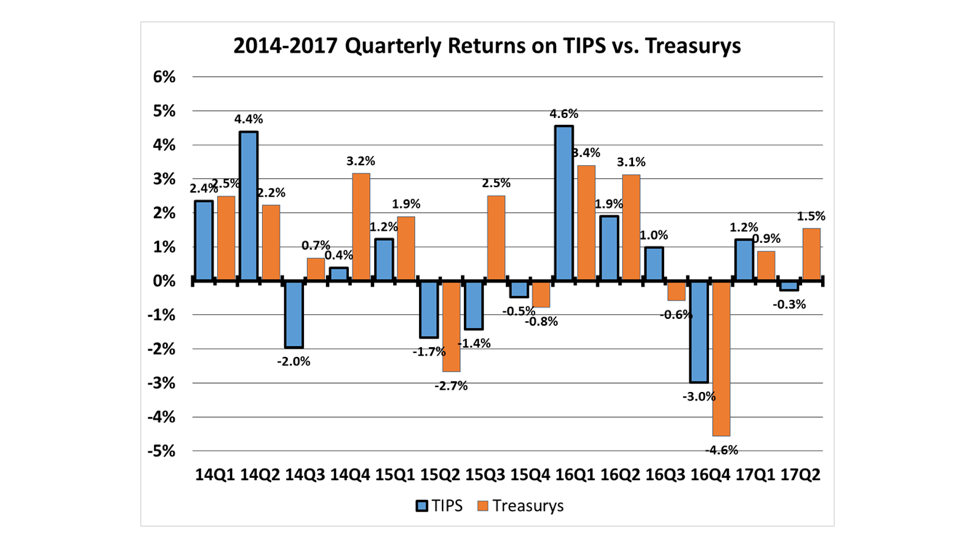

TIPS underperformed comparable maturity straight Treasury securities significantly in the 2017 second quarter. The average TIPS lost -0.3% in the quarter, while straight Treasurys gained 1.5%. The divergence in performance was due primarily to three factors: (1) the rise in short-term Treasury yields that coincided with the FOMC’s Fed Funds target rate hikes; (2) the decline in oil & gas prices, which dimmed the near-term outlook for the CPI and (3) the decline in long-term Treasury yields that was probably due to expectations of low inflation and moderating growth in the economy.

The average yield on TIPS jumped by 42 basis points (bp) from -0.01% at March 31, 2017 to 0.40% at June 30. The majority of the jump in yields was concentrated in the shorter maturities, where yields increased by 85 bp to 0.03%. Medium-term TIPS yields increased by 12 bp and long-term TIPS yields increased by 5 bp.

In contrast, comparable maturity Treasury yields declined by 4 bp on average to 2.03%. Short-term Treasury yields rose 8 bp; but medium-term Treasury yields fell by 12 bp and long-term Treasury yields fell by 19 bp. The decline in long-term Treasury yields translated into a very strong total return of 4.1% for the quarter.

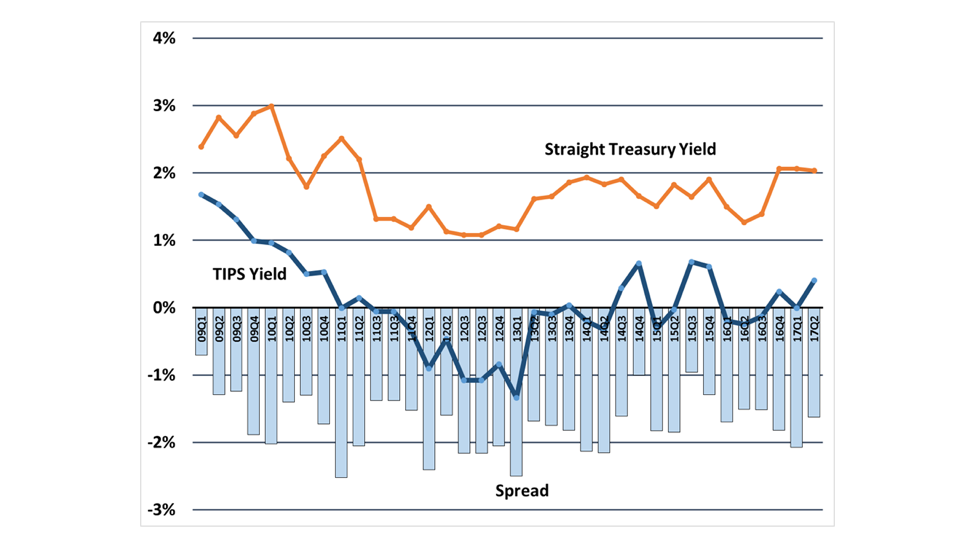

The differences in yield changes caused the spread between Treasurys and TIPS to narrow from 208 basis points in the 2017 first quarter to 163 basis points in the second quarter. Since the Treasury-TIPS spread has averaged 171 basis points from 2009 to 2017, the reduction in spread this quarter represented a reversion to the mean (with a little bit of an overshoot) from the wider-than-average spread in the 2017 first quarter.

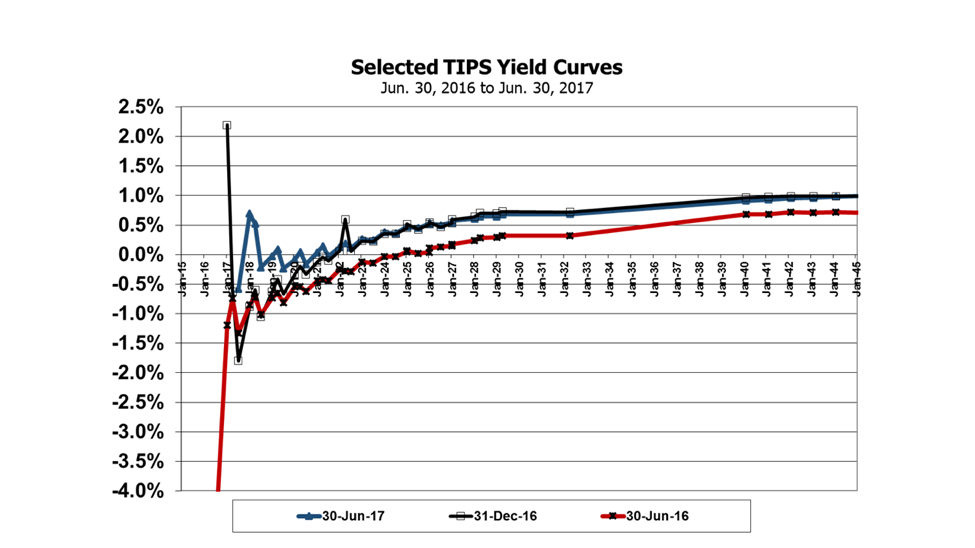

Since the 2016 second quarter the TIPS yield curve has shifted up, roughly in line with the increase in straight Treasury yields. Since the beginning of the year, the average TIPS yield has risen 16 bp, but all of the increase is due to a rise in short-term TIPS yields.

TIPS underperformed straight Treasurys for the first time in the past four quarters.

As June came to a close, Treasury yields climbed, apparently in anticipation of a normalization of interest rates. Low long-term Treasury yields have raised concerns in the fixed income community, especially as the Fed has begun in earnest the process of normalizing short-term interest rates. Although some Fed officials, including Fed Chair Janet Yellen and NY Fed President William Dudley, have indicated that the normalization process should continue despite low long-term Treasury yields, it would be surprising if the FOMC would allow the yield curve to become inverted.

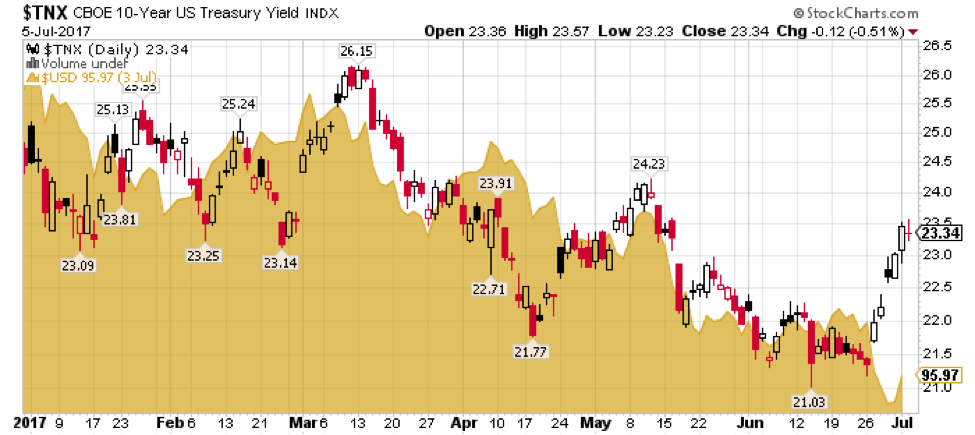

"At the end of June, the yield on the two-year Treasury was 1.38%. (It has since risen to 1.41%.) The two-year is seen as the primary indicator of Fed policy. Thus, the two-year seems to be anticipating one more increase in the Fed Funds rate probably this year."

Meanwhile, the yield on the 10-year Treasury note has risen from a recent low of 2.14% on June 26 to 2.31% at the end of June and now stands at about 2.33% as of this writing (July 5). The rise in yield coincided with comments from ECB President Mario Draghi suggesting that the central bank may begin to unwind its exceptionally accommodative monetary policies in the near future. This recently sparked a surge in the euro and sharp drop in the U.S. dollar. The rise in yield may also reflect an improving outlook for both inflation and the U.S. economy.

(It is worth noting, however, that Treasury yields have fallen steadily so far this year, along with the dollar. Still, if the dollar continues to decline, Treasury yields will eventually have to rise. The July 3 bounce in dollar futures, although probably due to short covering, could perhaps signal the start of the bottoming process; but it still too early to say with confidence that a bottom for the U.S. dollar is at hand.)

Courtesy of StockCharts.com

The outlook for TIPS for the balance of the year is obviously dependent upon the course of Treasury yields, inflation and the U.S. economy. The recent bounce in oil prices suggests perhaps a limit to the decline in inflation. However, the CPI is likely to see lower year-over-year increases or even declines for much of the balance of the year as a result of the decline in oil prices since early April.

An increase in inflation expectations is negative for straight Treasurys, but normalization of interest rates, which could result in higher real interest rates, are negative for both Treasurys and TIPS. On balance, as the outlook for the economy and inflation improves, TIPS should outperform straight Treasurys (and perhaps even other classes of fixed income securities), but TIPS they could still produce negative returns.

© Lark Research, Inc. All rights reserved.

Stephen P. Percoco is an independent security analyst covering equities and fixed income securities. He is the publisher of the Income Builder newsletter and the Risk-Reward blog. (http://www.larkresearch.com/risk-and-reward).

Read more commentaries by Lark Research

Courtesy of StockCharts.com

Courtesy of StockCharts.com