Weighing the Week Ahead: A Seinfeld Market?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsTrading desks will be closer to normal staffing. Chair Yellen’s biannual Congressional testimony will be a feature on Wednesday and Thursday, but the economic calendar is light. With little going on, the punditry will be wondering:

What should we expect for the rest of 2017?

Last Week Recap

The big economic news last week featured employment – as expected. The start of the G20 meetings and North Korean missile tests grabbed some headlines, but without much effect on stocks.

The Story in One Chart

I always start my personal review of the week by looking at this great chart from Doug Short via Jill Mislinski. Despite the Thursday selling, the result for the week was essentially unchanged (up 0.07%). Not much in the way of fireworks!

Doug has a special knack for pulling together all the relevant information. His charts save more than a thousand words! Read the entire post for several more charts providing long-term perspective, including the size and frequency of drawdowns.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

The economic news last week was good.

-

ISM Manufacturing registered 57.8, both an increase and a beat of expectations. The ISM notes that this level, if annualized, corresponds to a GDP increase of 4.6% and the figures for the YTD suggest a gain of 4.1%. (I think it is time for them to update their regression model). To provide some color, let’s look at the comments they cite.

“Overall, business is strong. We are seeing price increases for packaging and handling materials as well as some MRO supplies” (Plastics & Rubber Products)

“Overall, demand is up 5-7 percent and expected to continue through the end of the year, at least. ” (Transportation Equipment)

“Demand is picking up; meeting budget expectations.” (Electrical Equipment, Appliances & Components)

“Business is still very robust. Have continued to hire to match increased demand.” (Computer & Electronic Products)

“Business [is] steady; not great, but good and fairly solid.” (Furniture & Related Products)

“Business globally continues to show improvement.” (Chemical Products)

“Environmental regulations have strong effects on our business. We continue to watch for any changes as a result of the new administration.” (Paper Products)

“Dry weather helping demand.” (Nonmetallic Mineral Products)

“International business outside North America on the upswing.” (Machinery)

“Metal pricing continues to drag down our profit margins, but we are very busy quoting new business, so our customers have a good outlook on the rest of the year.” (Fabricated Metal Products)

“Business is strong both domestically and internationally. Supplier deliveries are quick domestically, international supply chain is slowing. We are in a hiring mode.” (Food, Beverage & Tobacco Products)

- Q2 Earnings are off to a good start. Only 7% of companies have reported so far, but FactSet notes the strong comparisons.

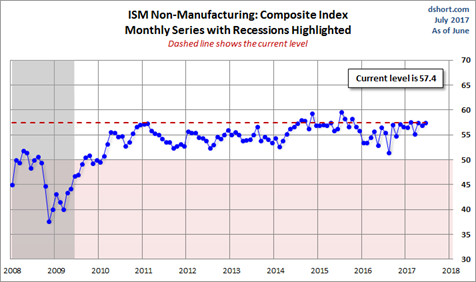

- ISM Services both increased and beat expectations with a reading of 57.4. Jill Mislinski digs into the data with useful details. Here is a key chart:

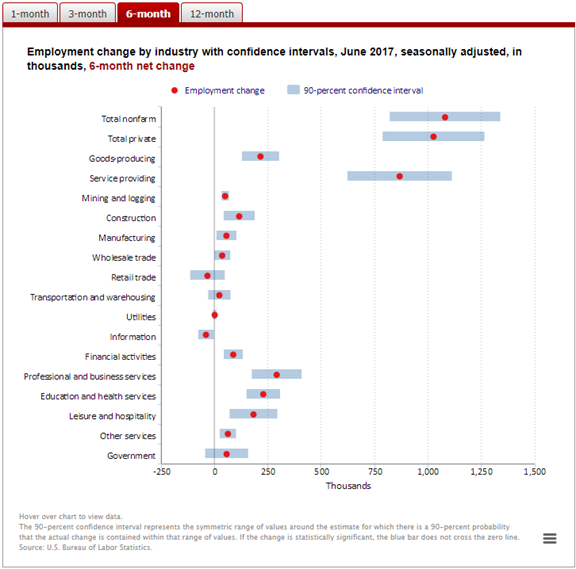

- Employment – Establishment Survey beat expectations. The gain of 222K net jobs handily beat expectations and the prior two months were revised higher. Calculated Risk calls it a “solid report.” Check out Bill’s full discussion and charts. Instead of charts from the NYT or WSJ and opinions from sell-side researchers, I suggest something different this month. The BLS has an interactive chart where you can look at various questions and zoom in for details. It is educational and fun (at least for data wonks). Since I believe that people take this report too seriously, I would like to emphasize the sampling error. This is not something that disappears after two revisions (although the benchmark revisions finally fix it). People react to this news because it is important, not because it is really accurate. The sampling error is better after a time, but by then no one cares.

The Bad

- Hotel occupancy has turned lower. (Calculated Risk).

- Factory Orders declined 0.8%, slightly worse than expectations of -0.7%. (MarketWatch).

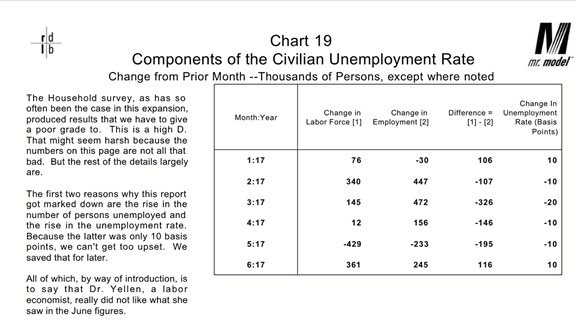

- Employment – Household Survey. Many observers jumped on the sluggish nominal growth in the hourly wage. Bob Dieli, who writes an excellent and comprehensive employment analysis each month (subscription only), gave the Household Survey a “high D.” The main reason was that more people are unemployed. It is not terrible, and only one month, but something to watch.

Bob’s analysis, unbiased and representing quality you will not see elsewhere, focuses our attention on when and if business confidence will start to show up in the numbers. You see this only via a deep study of the components.

The ADP report, which I regard as a solid independent measure, disappointed with an estimate of a net gain of only 158K private jobs.

The Ugly

Russians are now suspects in the hacking of nuclear sites. (Bloomberg). This is certainly a time for effective diplomacy.

Illinois finally got off our ugly list (after over two years) by passing a budget. While not a complete answer, it is a step. Road construction, promised educational payments, debt repayment, and Powerball will now resume.

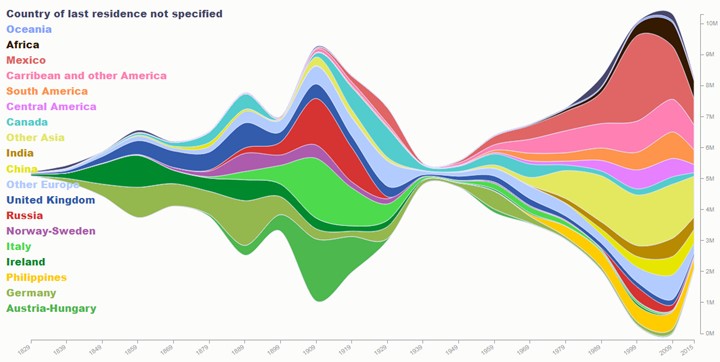

I spotted some great charts that you will enjoy (Visual Capitalist). One of them, which I cannot represent here, shows worldwide immigration over the last 200 years or so. Take a look, to see the streams of people change throughout history.

For a US focus, consider how immigration patterns have changed. Part of the changes reflect the changing identification of residents.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

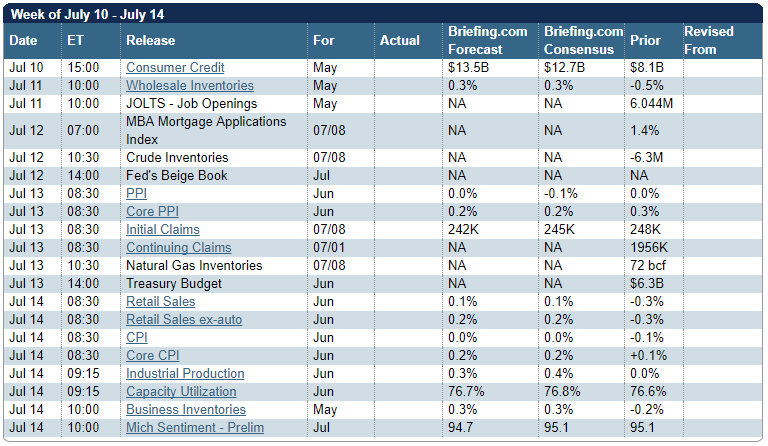

The Calendar

It is a light calendar, with mostly secondary reports. Chair Yellen’s testimony before Congress – House Financial Services Committee on Wednesday and a repeat for the Senate Banking Committee on Thursday – could prove interesting. I expect a more hawkish tone and the usual challenging questions from some. Retail sales is important. It is an important sector and there was weakness in the prior report. The inflation data will eventually be important, but not yet.

There is also some FedSpeak, and the release of the Beige Book. Those who want to focus on the Fed will have plenty of material.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

With the light calendar and low volatility, what will people write and talk about?

Mrs. OldProf provided the answer this morning at breakfast. As usual we split the Trib – sports for her and front section for me. She soon observed that it “was hard to be a Cub.” Encouraged to elaborate, she explained that whatever the specific news, the story was always about the disappointing first-half performance. A star hits two home runs. The team releases a catcher who allowed seven stolen bases in a single game. Both are treated similarly: Will this turn the Cubs around? The celebrated general manager, who was acclaimed as a genius until a few weeks ago, is expected to stir the pot somehow.

She is quite right. It sounds so familiar. Since I was thinking about this week’s theme, her comment was especially helpful. What she described is just what we are seeing in the “analysis” of the current stock market. Most stories are about the long bull market. Often there is an angle about the end of the rally. How much longer? What can go wrong?

It is a Seinfeld market. The story is about nothing, but must be described along the way. With nothing better to discuss, people will be asking:

Here is a range of opinion.

-

We are lucky to have lasted this long.

-

The Fed gaveth and the Fed will taketh away. Most of the trading community is on this side. Bill Kort examines a couple of recent examples where Central Banker comments got a strange twist. Also contra – Peter F. Way, who uses market-maker hedging as a key indicator. He sees no change in the hedging patterns, indicating no immediate problems.

-

Technical warnings. Blue Harbinger identifies some sector moves that seem to suggest “that the rally is capitulating.” Contra – the Fear and Greed trader sees a Dow Theory buy signal.

-

Everything is good, which always precedes a market top. This was Greg Ip’s call (Fox republishing a WSJ piece), Why Soaring Assets and Low Unemployment Mean It’s Time to Start Worrying. I cited my alternative viewpoint in a tweet where I suggested: You cannot use a shining sun as a predictor of nightfall. Mr. Ip courteously retweeted my link. See also The Capital Spectator.

-

Fundamentals remain strong with no sign of imminent danger. CNBC’s Michael Santoli looks at the ten-year anniversary of the prior market top. See also Scott Grannis’s outlook and an update of sixteen charts.

-

Tongue-in-cheek advice to pundits. Barry Ritholtz gives ten bullet points to consider in helping you call a market top. This post has the great combination of being both entertaining and very helpful. Here is the first bullet:

No. 1. Pick a bogeyman: This is your first step to making a top call. Find whatever it is that will precipitate the next collapse, and home in on it. Tweet about it and write 5,000-word screeds explaining why this spells doom. The specific bogeyman isn’t all that important — just so long as you have one. Some good starter examples are: the Federal Reserve (or zero interest rates or quantitative easing), the national debt, hyperinflation, or the collapse of the dollar. Or how about New York Stock Exchange margin debt or that robots will take away everyone’s job? Mix and match these or be creative and invent a few of your own.

As usual, I’ll have more in my Final Thought.

Quant Corner

We follow some regular featured sources and the best other quant news from the week.

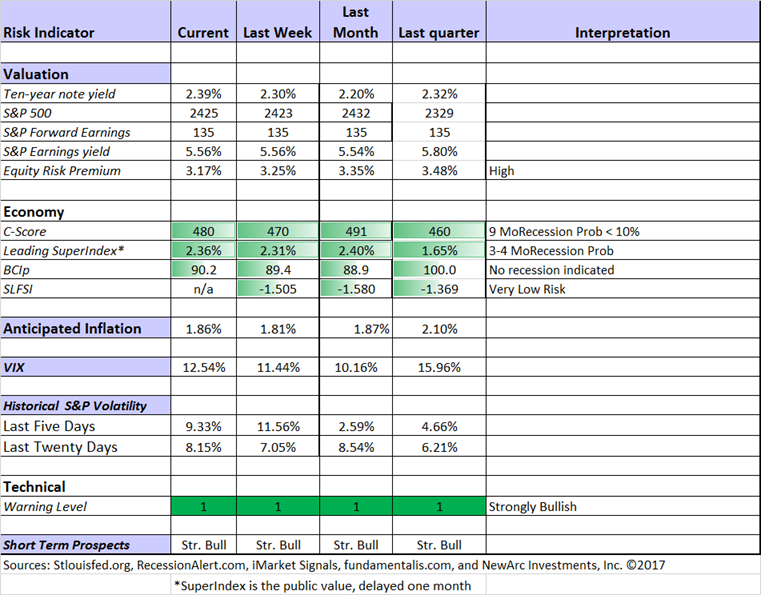

Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

The Indicator Snapshot

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score.

RecessionAlert: Strong quantitative indicators for both economic and market analysis.

Georg Vrba: Business cycle indicator and market timing tools.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

Doug Short: Regular updating of an array of indicators. Great charts and analysis.

Insight for Investors

Investors should have a long-term horizon. They can often exploit trading volatility!

Best of the Week

If I had to pick a single most important source for investors to read this week it would be Morgan Housel’s list of ten things he believes most about investing. I particularly like this example:

Many failures can be traced to the pointless pursuit of arbitrary benchmarks. Most notable is the calendar, which pushes companies and investors to cut corners before the earth completes its rotation around the sun. Swap out the sun for another celestial body and you’ve described a mental illness. Another is index benchmarks, which use something short-term and broad (industry performance) to guide something long-term and specific (a strategy to meet your goals).

Stock Ideas

Homebuilders?

24/7 Wall St. closely follows upgrades and downgrades. I do not always agree, but the Merrill Lynch call on Homebuilders makes sense to me.

Energy? Barron’s (subscription required) has an interesting article citing an expert who sees a floor in energy prices. The basic idea is that traders over-reacted to the original OPEC supply limitation, not considering a key loophole. This has led to unwarranted swings in prices. If you are interested, this is one you must evaluate for yourself. There is also an interesting stock pick on this theme.

Lee Jackson (24/7 Wall St.) cites the public statements from Merrill Lynch, with five picks based upon crude “bouncing” off a low of $42. These are generally bigger, “safer” names.

Chip Stocks? Lee Jackson has more ideas from Merrill. One of these passes some of Chuck Carnevale’s tests, so I am looking.

Capital Markets Laboratories does a comprehensive analysis of Lam Research (LRCX) which we bought a few weeks ago.

Defense stocks? A reaction to N. Korea? Peter F. Way ranks thirteen companies.

Biotech?

Bret Jensen wonders whether Gilead (GILD) could learn something from Celgene (CELG). I hope so, since I like both.

Good companies?

Chuck Carnevale examines seven attractive companies and shows how to find those worth further study. I usually prefer reading to watching videos, but Chuck covers key points in an upbeat style.

Dividends? Simply Safe Dividends does a comprehensive analysis of Archer Daniels Midland (ADM). He looks at the business history, the current revenue drivers, and all the key metrics. Readers will enjoy the helpful diagrams and charts. Over at the Stock Exchange, our dip-buying model, Holmes, is cheering at the support for his pick of the week.

Seeking Alpha Senior Editor Gil Weinreich has an interesting topic every day. This week I especially enjoyed his commentary on warnings and predictions. If you read today’s “Final Thought” you will see some ideas of how to implement this. Gil also considers 26 retirement risks from Dirk Cotton. Gil emphasizes longevity, and that is certainly a good place to start.

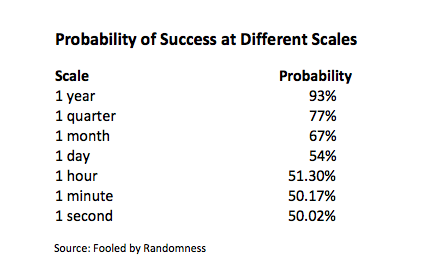

Watching stock quotes too frequently will reduce your performance (Investment Master Class). Warren Buffett does not even have a computer on his desk. Suppose you were getting a 15% return with 10% volatility – a combination that most would find attractive. Here is how this translates into returns in different time frames:

See also Bob Seawright, Worrying is a Serious Offense.

Watch out for….

Target date funds. Morningstar’s John Rekenthaler explains why the management choices might not fit your personal situation. He replaces target “date” with target “wealth.” I agree.

Final Thoughts

Most market pundits and sell-side strategists are forced to write – whether anything important is happening or not! Some of this is driven by the calendar, especially when doing an annual forecast or revising it for the second half.

Many have allowed some simplistic notions to distort their analytic framework. If you attribute the stock rally to the Fed, ignore what Shiller and Buffett really said about valuation, and use “averages” to tell you how long a business cycle will be – you are starting your risk/reward analysis at a big disadvantage.

I do not make annual market forecasts. I certainly do not get tied to a calendar. Individual investors might find this approach useful.

- Discover some trusted indicators for both risk and reward.

- Find investments that represent good companies at good value.

- Do a regular review, adjusting your stock price targets to reflect the most recent information.

- Adjust your portfolio as needed, including the risk level, asset classes, and individual stock positions.

You are not forecasting. You do not need a year-end market target. You need not call a top or bottom. You should not try to beat the market in a specific time frame, since your inexpensive stocks (at the start) will be out of step with current market perceptions.

A strong investment process is easy to describe, challenging to implement, and rewarding when done well.

What worries me…

- China, Russia, and North Korea. The second meeting between President Trump and Chinese President Xi Jinping did not turn out as well as the earlier meeting at the Trump Florida resort. The Putin/Trump meeting did not lead to much in the way of a detailed update. The cooperation of both will be needed in dealing with North Korea. Fortune’s CEO Daily had a helpful summary of this topic, including some good links.

- Trade. The EU is initiating some trade restrictions against the US. I am watching this issue closely.

…and what doesn’t

- The Fed. That includes both rate increases at a reasonable pace and the planned balance sheet reduction.

-

Stock market valuation. Stocks overall seem mildly attractive if you consider expected earnings and interest rates. More importantly, some are significantly overvalued and others are attractive. Stock and sector picking are more important than market valuation.

© New Arc Investment Managementhttp://dashofinsight.com

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All