Introduction and key points

- As an asset class, Emerging Market (EM) equities have evolved considerably in the last 25 years, but traditional valuation metrics have remained static and should not be relied upon solely to guide allocation decisions.

- A thorough assessment of risk grounded in analyzing macroeconomic vulnerability, currency risk, and political risk should be a key determinant for your EM allocation.

- Combining valuation with an explicit risk assessment can significantly improve EM allocation decisions. Since 2002, an allocation to EM guided simply by Shiller P/E would have delivered robust median annualized returns of 14%. However, combining risk assessment tools with this simple valuation measure would have resulted in annualized returns of about 30% with fewer drawdowns over the same period.

- Our overall assessment of EM today is constructive: We believe risks are significantly lower and valuations are fair.

Most of our investors are familiar with (and hopefully appreciate) the multiple lenses through which GMO analyzes an asset class. Given our two-plus decades of experience in investing in EM, this paper focuses on complementing a traditional valuation-based framework with a risk-based approach that is designed to assess the attractiveness of the EM asset class. In GMO’s 1Q 2017 Quarterly Letter, Ben Inker states that the most important decision in determining long-term returns investors can earn is how much risk the investor is prepared to take.1 While the relationship between risks and expected returns is linear, he cautions that too much risk can also spell disaster for investors. We agree with the broad set of risks2 he identifies, and as dedicated, experienced EM investors we believe Ben’s warning is particularly relevant in the context of EM investing.

Traditional approaches to determining an optimal EM allocation have remained static

2017 marks the 37th year since Antoine van Agtmael referred to a selection of developing countries as “emerging markets,” and the 29th year since MSCI first devised an EM equities index. To state the obvious, much has changed in these past few decades. In 1993, the MSCI EM index had an investable market value of $300 billion. Today, the Chinese internet sector alone is valued at $820 billion, and several other country-specific sectors – the Taiwanese technology sector and Indian private banking sector, to name two – surpass the value of the asset class in its infancy. However, when it comes to the consensus view on analyzing the EM asset class, the more things change, the more the industry and its insufficient analysis appear to remain mired in the past.

In our conversations over the last 20 years with asset allocators, we have noted that consensus has guided them toward a top-down approach to EM valuation. The three most common and seemingly robust metrics for valuations are:

1. Asset class valuations relative to history;

2. Absolute valuations; and

3. Asset class valuations relative to developed markets.

Aggregate metrics are a classic example of reliance upon heuristics – easy-to-understand rules and principles that simplify complex decision-making processes. Given the evolution of the asset class, we believe each of these three metrics – once perhaps an optimal set of heuristics – now result in an inadequate assessment of fair value.

First, measuring valuations relative to history has some merit, but we must acknowledge that the composition of the asset class has changed drastically over the last 20 years. The approach relies on comparing a current valuation metric such as the Shiller P/E to a historic average and extrapolating whether the asset class is cheap or expensive on this basis. For instance, financials contribute 35% of earnings today vs. 15% in 2003, while earnings from commodities have shrunk from 44% to 15%. Unsurprisingly, regions such as Latin America and CEMEA (Central and Eastern Europe, Middle East, and Africa) have been replaced in importance by Northeast Asia, whose contribution has grown from 40% to over 57.5% of earnings.

Second, looking at the EM aggregate index on a stand-alone basis masks its deficiencies. We believe the index has significant embedded risks in the form of single-country earnings risk (i.e., China-related earnings constitute over 41% of index earnings); so-called “government-linked companies” (companies with two masters whose earnings constitute 45% of the index); and finally, the overarching weight of financials (risk of buying a highly-levered earnings stream because financials represent 40% of the index’s book value). Therefore, when you buy the EM index or compare absolute valuations, how much of what truly drives emerging markets – rising consumption of the middle class, favorable demographics, evolving sociopolitical institutions – are you really getting? The answer is simple: very little.

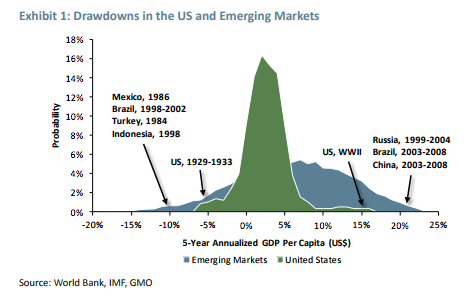

Third, comparing the valuations of a disparate group of 23 countries to the more homogeneous developed markets group and subsequently assigning a premium or discount to growth results is perilous if the comparison is blind to the varying economic volatility of the two groups. For instance, while the Great Depression was an economic event of enormous magnitude in the US, drastic drawdowns are frequent in EM countries where governments and institutions are not as mature. Exhibit 1 shows the 5-year annualized GDP per capita growth and occurrence of drawdowns across time for the US and EM countries. The fat tails on either side of the chart illustrate that from Mexico in 1986 all the way to China and Brazil (from 2003-08), emerging markets have fallen victim to a number of volatile economic events.

A risk-based approach to assess asset class attractiveness

The bedrock of any framework used to evaluate the attractiveness of EM should be an assessment of inherent risk. Since 1990, an average EM country has experienced 5 times more drawdown than the S&P. Within the EM index, each country has fallen more than 20% an astonishing 22 times. The S&P on the other hand, has fallen by over 20% only 4 times since 1990. Not only are drawdowns frequent in EM, but the time it takes to recover capital is also substantial. For instance, it took more than 15 years for the Thai and Indonesian markets to reach pre-crisis levels after their precipitous drop in 1997. As EM investors, our priority is to ensure return of capital first. Return on capital is step two.

In an attempt to quantify risk in EM, we have devised an aggregate risk metric, which is built by using country-level assessments of the following four variables:

1. Dependency on external savings to identify balance of payment risks;

2. Above-trend growth to identify economies growing in an unsustainable manner;

3. Currency valuation because currency shocks translate into economic shocks and detract from returns for developed market-based investors; and

4. Political uncertainty to anticipate event risks. In many EM countries, the absence of economic institutions with long-standing track records of independence and effectiveness allows for the possibility of an individual in power to derail or severely impact economic growth.

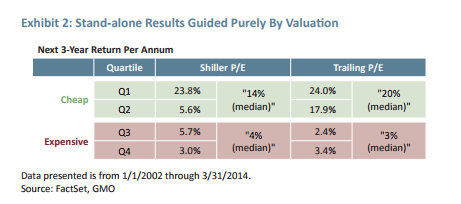

Exhibit 2 shows the results of a back test of data for allocations to EM from January 1, 2002 to March 31, 2014. Over this period, there were times when the EM index could be classified as “cheap” and those where the index was “expensive.” For the purpose of this analysis, “cheap” denotes a period when the Shiller P/E was less than the historical average, while “expensive” was when the Shiller P/E was greater than the historical average. As the table shows, a strategy based on allocating guided purely by valuation (focused on Quartiles 1 and 2 that are “cheap”), gets an investor only part of the way there – the strategy delivers median annualized returns3 of 14% based on a 3-year holding period, but this is accompanied by dispersion between quartiles that is significant. Yet, broadly, investing when the asset class is “cheap” provides a respectable annualized return.

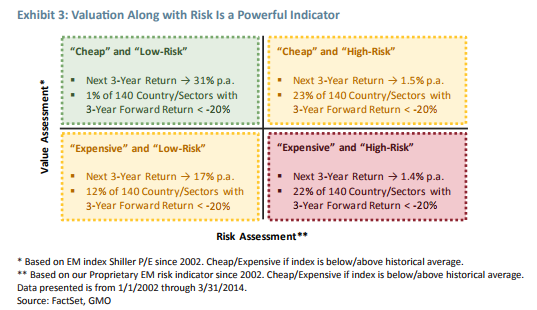

Exhibit 3 shows the benefits of combining valuation with our explicit assessment of risk. Exhibits 2 and 3 both use an identical value assessment. We have overlaid this with an assessment of risk in Exhibit 3 based on data calculated from our proprietary EM risk indicator as defined by the four variables mentioned earlier. For the purpose of this analysis and specific to our risk indicator since 2002, a period is classified as “high-risk” if the indicator is above the historical average, and “low-risk” if the indicator is below the historical average. The numbers indicate the historical returns and drawdowns if we had invested in EM when it was in each quadrant.

Investing only when valuations were cheap and risks were low delivered a median annualized return that was 2x what a valuation-driven strategy would have delivered. Moreover, drawdowns were limited to only 1% of the 140 country/sector combinations4 in EM that delivered a negative accumulated return of greater than 20%.

Returns and drawdowns when EM were in the cheap and high-risk quadrant or expensive and lowrisk zone validate the point that risk assessment, rather than valuation, matters more in guiding EM allocations.

Finally, avoiding EM when they were expensive and in the high-risk category paid off extremely well. Clearly, a “buy and hold” strategy for the broad asset class is not the right approach.

Current EM assessment based on risk and valuation

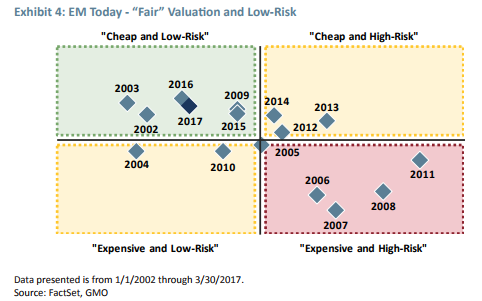

Exhibit 4 plots the movement in emerging markets from years 2002 to 2017. Clearly, EM is a welltravelled asset class, having spent time in each of the four quadrants shown. Having the right tools available to assess whether EM assets will provide returns that justify the risk is critical. We complement our risk assessment and valuation tools with behavioral gauges such as sentiment and tactical indicators. Currently, these signals are positive for the asset class. As we look ahead to the second half of 2017, we believe EM risk is lower today (than it was 5 years ago in 2012) and valuations are fair.

Implications for your asset allocation decisions

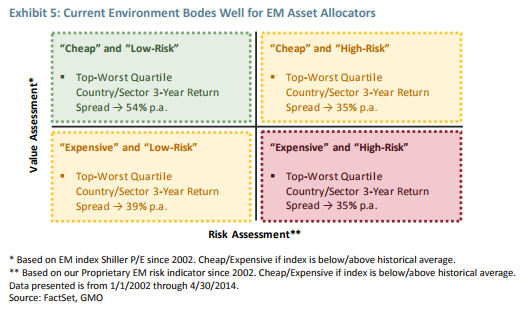

Data from 2002 to the first quarter of 2017 has shown that when the asset class is the least risky, active managers can add the most value by exploiting the divergence between the best and worst performing EM countries (Exhibit 5).

Conclusion

Frequent and significant drawdowns in emerging markets can lead to a permanent impairment of capital. To this end, taking a risk-based approach to evaluation of the asset class can guide allocators as to the timing as well as whether to opt for a broad-based EM strategy (where diversification is a key objective) or a more concentrated strategy (where return optimization is a key objective) focused on a handful of country/sector combinations. Based on individual risk capacity,5 asset allocators may opt for one or the other, or, in certain cases, a combination of the two. For either of these strategies, we use our proprietary risk indicator, along with an assessment of valuations and sentiment, to guide portfolio construction and, specifically, to determine how aggressive or defensive the portfolio will be positioned at any point in time.

Amit Bhartia. Mr. Bhartia is a portfolio manager for GMO’s Emerging Markets Equity team and oversees fundamental research. Prior to joining GMO in 1995, he worked as an investment advisor in India. Mr. Bhartia earned a Bachelor of Engineering at the University of Bombay and an MBA at the Institute for Technology and Management in Bombay. He is a CFA charterholder.

Mehak Dua. Ms. Dua is engaged in client relations and business development for GMO’s Global Client Relations team located in the Singapore office. Prior to joining GMO in 2015, she was a Vice President at PIMCO in New York where she was responsible for coverage of corporate clients. Previously, she was an investment banker at Goldman Sachs & Co. in New York and London and has also worked at HSBC. Additionally, she has served as a consultant to the World Bank. Ms. Dua holds an MBA from Harvard Business School, a B.A in Politics, Philosophy and Economics (P.P.E) from Merton College, University of Oxford, and a B.A. in Economics from Lady Shri Ram College, University of Delhi. She is also a Rhodes Scholar (Oxford, 2002).

Disclaimer: The views expressed are the views of Amit Bhartia and Mehak Dua through the period ending July 2017, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2017 by GMO LLC. All rights reserved.

1 Ben Inker and GMO’s Asset Allocation team’s objective is to construct a multi-asset portfolio that can withstand various economic environments. Given our sole mandate of investing in emerging markets, the underlying considerations vary such that our assessment of the EM asset class may at times be different than the Asset Allocation team’s views.

2 In GMO’s 1Q 2017 Quarterly Letter, Ben Inker’s “Up at Night” suggests there are “eternal” risks (e.g., depression risk and risk of unanticipated inflation) as well as those emanating from the contemporary economic, political, and environmental circumstances.

3 Median annualized return assuming a 3-year holding period; all results are in USD.

4 Existing 140 country/sector combinations defined by GICS and MSCI EM Index.

5 In the previously mentioned “Up at Night,” Ben Inker suggests that in determining how much risk investors can take, they ought to differentiate between risk capacity and risk appetite. He defines risk capacity as the extent of loss investors can take without having to significantly change their spending patterns. Risk appetite is more about a lack of education on investing such that an investor with lower risk appetite than risk capacity will wind up leaving money on the table.

© GMO

Read more commentaries by GMO