Who would have thunk it? When Theresa May announced the UK election, it looked as though she would cruise to an easy victory with an expanded majority. Instead, just a few weeks later, she found Jeremy “more money for everyone” Corbyn nipping at her heels.

Prime Minister May is now regarded as damaged goods. She is a decent person who miscalculated. It will probably cost her the Prime Ministership. As we put pen to paper, she remains in that position but there are no doubt several challengers lurking in the wings. There will, however, be some hesitancy about moving against her too soon as it may precipitate a new election. That is the last thing the Tories want at the moment — as Corbyn would probably win! What an extraordinary turn of events.

We should be used to convulsive turns in British politics. There are now plenty of examples of expectations being trampled by an unforeseen swing in the tide of public opinion. To be fair to Mrs. May, she did increase the percentage share of the Conservatives overall vote — in fact, to the highest level in more than 30 years. What caused her undoing was the flow of votes from the minor (and disappearing) parties that ended up in Labour’s pocket. And just to prove that politics is truly unpredictable, the Conservatives actually increased their vote in Scotland — winning an extra 12 seats. Their leader, Ruth Davidson, will be worth watching. And now the Brexit negotiations commence in a real muddle. Is it to be a hard, soft or just middling Brexit? Sounds like we are cooking eggs. There is a reinvigorated push to go “soft” as it is the perception of the media that the British public is in favor of a watered-down EU departure. Although, frankly the matter is so complex and so muddied by all the vested interests that we doubt that the majority of voters have the slightest idea just what it all means. Our guess is that they want all the so-called good things from being involved with the EU and none of the bad. That probably means control over immigration but membership of the customs union. This latter body ensures that goods trade freely within the EU, but common tariffs are imposed on countries outside the EU. So there goes Britain’s ability to establish free trade deals with other nations.

Many studies have demonstrated that freeing up a country’s trade (not just with a select and favored few) is of significant economic benefit. In one of its most recent releases, the OECD commented, “The empirical evidence confirms the strong link between trade and growth. More open countries, where trade openness is measured by imports plus exports as a percent of GDP, typically have a higher level of GDP per capita. Moreover, with the exception of the Russian Federation, countries that have been able to increase their exports to-GDP ratio over time have also improved labor productivity over the same period… Specialization according to comparative advantage and, increasingly, technology-driven and deeper trade integration through global value chains have created new business opportunities and increased economic efficiency. Access to a wider variety of goods and services at cheaper prices has raised well-being and consumers’ purchasing power.”

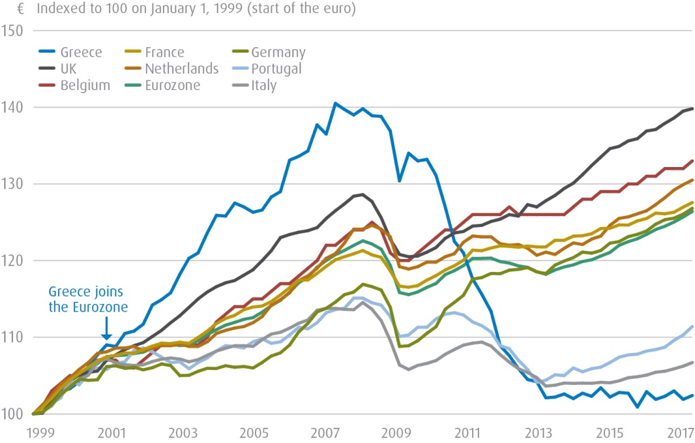

If the EU and, in particular, the Eurozone, had been shooting the economic lights out we would all be wondering why Britain would even consider leaving, but of course, that has not been the case. A straight comparison of UK GDP growth since the start of the Eurozone (January 1999) with euro-bloc performance demonstrates superior UK growth both before and after the 2008-2009 economic crisis (see chart below).

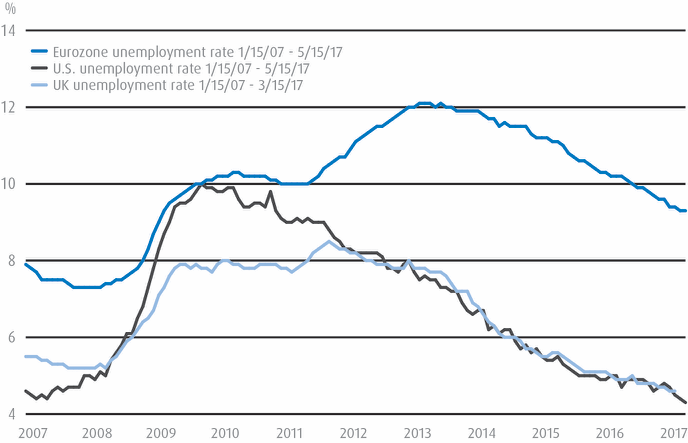

Over the same period, labour productivity growth in the UK has averaged 1% (not great) but the Eurozone has managed only 0.6%. A comparison of unemployment levels in the UK and Eurozone produces a stark result (see chart below). For reference purposes, we have included the United States as it is regarded as the poster boy for the improvement in employment trends in recent years. However, as you can see from the chart, the UK lacks nothing in comparison.

We are not suggesting that the UK economy has been performing in a stellar fashion. Far from it. But in a low-growth world (mired in what the OECD likes to refer to as a “low-growth trap”) the UK hasn’t been anywhere near bottom of the table.

Regular readers will be aware we have been optimistic about the UK’s prospects outside the “embrace” of the EU machine. Frankly, we consider the threats of the UK being “punished” by the rest of the EU as naïve. Britain is the fifth biggest economy in the world and a huge market for European goods. Put simply, the members of the EU benefit from a prosperous British economy. Now that Brexit negotiations have been thrown into disarray and the final outcome is far from predictable we will reserve further comment and judgment until more certainty emerges.

Disclosure

All investments involve risk, including the possible loss of principal.

Foreign investing involves special risks due to factors such as increased volatility, currency fluctuation and political uncertainties. High yield bond funds may have higher yields and are subject to greater credit, market and interest rate risk than higher-rated fixed-income securities. Keep in mind that as interest rates rise, prices for bonds with fixed interest rates may fall. This may have an adverse effect on a Fund’s portfolio. Investments cannot be made in an index. This presentation may contain targeted returns and forward-looking statements. “Forward-looking statements,” can be identified by the use of forward-looking terminology such as “may,” “should,” “expect,” “anticipate,” “outlook,” “project,” “estimate,” “intend,” “continue” or “believe” or the negatives thereof, or variations thereon, or other comparable terminology. Investors are cautioned not to place undue reliance on such returns and statements, as actual returns and results could differ materially due to various risks and uncertainties. This material does not constitute investment advice. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. Investors should seek advice regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Investment involves risk. Market conditions and trends will fluctuate. The value of an investment as well as income associated with investments may rise or fall. Accordingly, investors may receive back less than originally invested.

Pyrford International Ltd. (Pyrford) is a registered investment adviser and a wholly owned subsidiary of BMO Financial Corp. BMO Global Asset Management is the brand name for various affiliated entities of BMO Financial Group that provide investment management and trust and custody services. Certain of the products and services offered under the brand name BMO Global Asset Management are designed specifically for various categories of investors in a number of different countries and regions and may not be available to all investors. Products and services are only offered to such investors in those countries and regions in accordance with applicable laws and regulations. BMO Financial Group is a service mark of Bank of Montreal (BMO).

BMO Asset Management Corp. is the investment adviser to the BMO Funds. BMO Investment Distributors, LLC is the distributor. Member FINRA/SIPC. BMO Asset Management Corp., BMO Investment Distributors, LLC, BMO Private Bank, BMO Harris Bank N.A. and BMO Harris Financial Advisors, Inc. are affiliated companies. BMO Private Bank is a brand name used in the United States by BMO Harris Bank N.A. BMO Harris Financial Advisors, Inc. is a member FINRA/SIPC, an SEC registered investment adviser and offers advisory services and insurance products. Not all products and services are available in every state and/or location.

Investment products are: NOT FDIC INSURED — NOT BANK GUARANTEED — MAY LOSE VALUE.

© 2017 BMO Financial Corp. (5926798, 7/17)