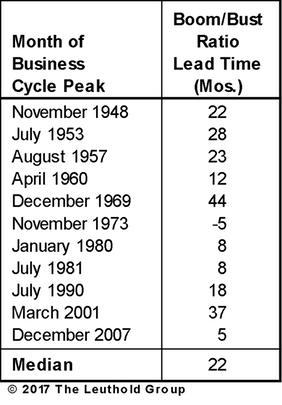

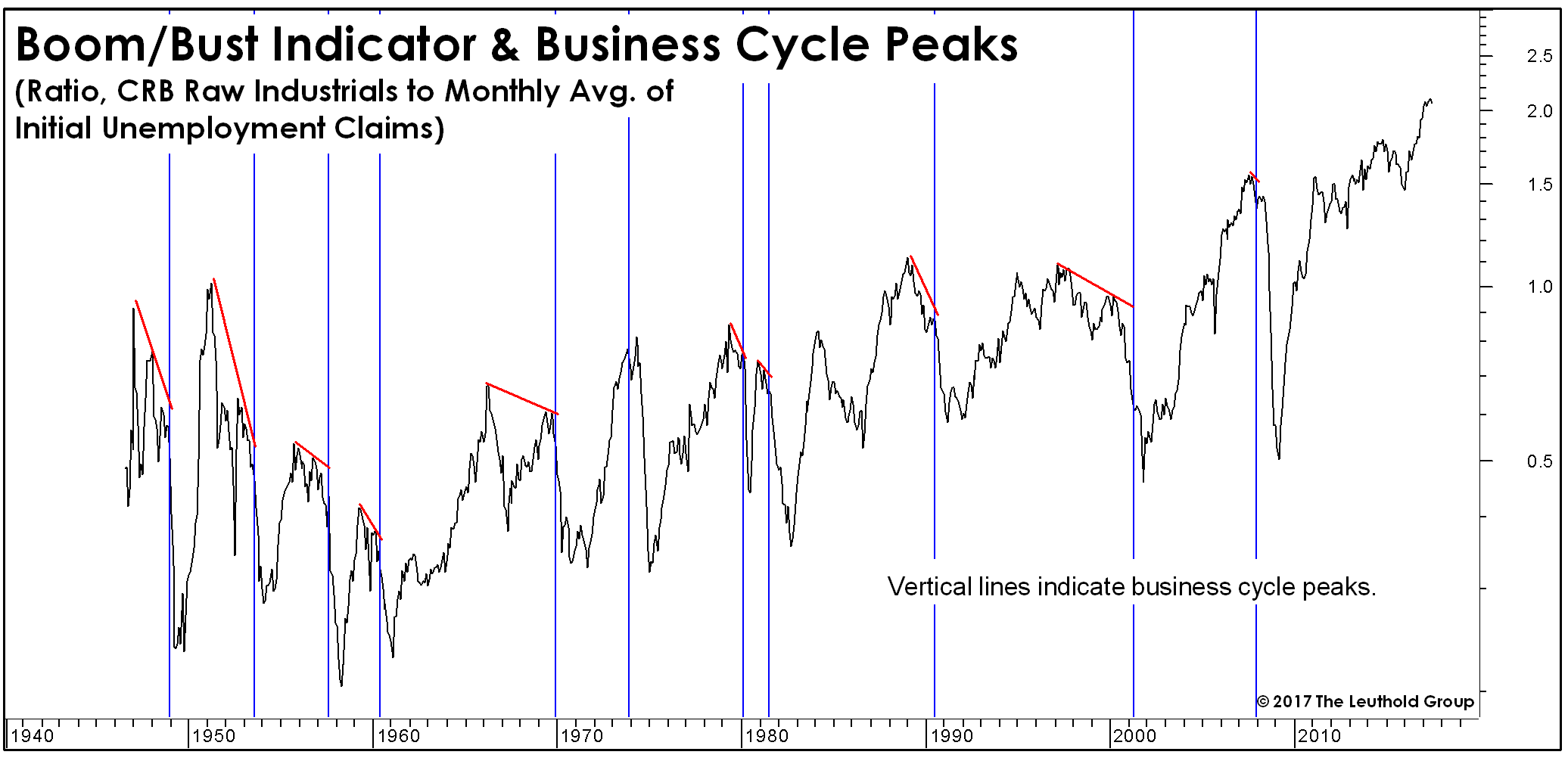

The odds of recession in the next 12 months appear low based on a number of financial indicators, including the yield curve, corporate credit spreads, and of course the stock market. We generally prefer these market-based measures over government generated statistics for economic forecasting purposes. The Boom/Bust Indicator, however, combines a market-based measure (commodity prices) with a weekly government report on the employment situation. The ratio of the CRB Raw Industrials to initial claims for state unemployment insurance typically peaks out well in advance of the business cycle, as shown in the above chart. This measure has broken sharply higher in the last year and a half as industrial commodities have rebounded from their latest trough and claims have continued to drift lower.

This indicator cannot boast the yield curve's perfect postwar forecasting record; it failed to signal any trouble in advance of the 1973–1975 recession. Generally, though, this ratio turns down at least five months in advance of the business cycle top, as shown in the below table. It's another reason we are reluctant to forecast recession despite the cycle's already extended length, along with recent signs of toppiness in the auto market and brick-and-mortar retail.