Imagine an asset class with a decently positive expected rate of return, little to no equity beta, and little to no interest rate duration. A unicorn? We think not.

It’s no secret that we at GMO have concerns today about the valuations of traditional asset classes. The S&P 500, as measured by the Cyclically Adjusted Price to Earnings Ratio, sits above its 2007 levels and within a whisper of levels seen just before the crash of 1929. Our published forecast for US large cap stocks, and many other parts of the global equity markets, sits in solid negative territory.

For bonds, US 10-year treasury yields hit 1.36% only 12 short months ago, the lowest ever recorded in American history. And last spring, interest rates in Europe were the lowest in four centuries. (Dare I even mention that the 50-year Swiss bond’s nominal yield went negative?) You cannot make this stuff up. Our forecasts for most bond markets around the planet are pretty bad, as any form of normalization of rates is likely to cause some pain.

When we see both equities, generally, and bonds, generally, with poor to even negative expected real rates of return, we ask ourselves a simple question: Is there an asset class out there that has the following attributes:

a) a decently positive expected rate of return;

b) little to no equity beta; and

c) little to no interest rate duration?1

For a significant chunk of the last 150 years of US capital markets history, the answer was typically… cash! (Please note that in 2007, when we were warning about a global risk bubble and negative expected rates of return for almost all risk assets, T-Bills were yielding 4.7% nominal, or almost 2% real!) Today, we cannot say that. T-Bills, even with the recent Fed hikes, are still paying a negative real yield.

So, we ask again: Is there another asset class out there with these seemingly magical attributes? Or are we searching for a unicorn?

No unicorns here. No magic required. It’s called Merger Arbitrage (Merger Arb, for short).

Positive expected return

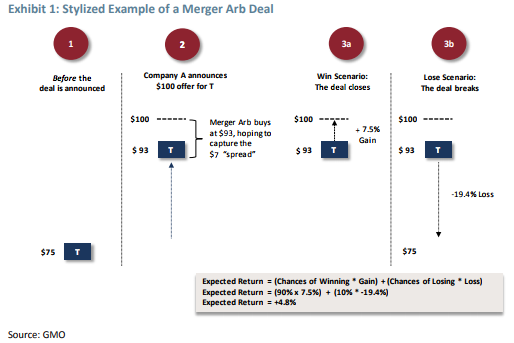

First, let’s do a quick review of what a Merger Arb portfolio typically holds. We’ve provided a pretty clean example in Exhibit 1. Imagine that company “A” (Acquirer) makes an offer to buy a publicly traded company “T” (Target). Let’s assume it’s an all-cash deal. Exhibit 1 lays out the sequence of events. In Step 1, Company T is trading for $75 before the announcement. In Step 2, Company A announces to the world that it wants to buy Company T for $100, or a premium of $25. Within seconds, the price of T’s stock moves upwards; it gets very close to the $100 offer price. Does it go all the way? Typically not. In our example, the price moves to $93. Why? Because the deal typically takes six to nine months to actually close and during that period some bad things could happen. For example, a regulatory body might put a stop to the deal; the Acquirer might not be able to line up the financing for an all-cash deal; or due diligence unearths some hidden liabilities connected to Company T. You get the idea – there is some uncertainty, or risk, that the deal collapses, or “breaks,” in industry parlance. This $7 spread is what Merger Arb players are interested in: They would step in to buy Company T for $93, hoping to earn the $7 spread as compensation for taking on those latent risks. This, of course, is the arbitrage.

Over the next few months, the price of T will oscillate, depending upon the market’s changing perceived odds that the deal will close or break. The return profiles of each outcome are strikingly different. In Step 3a, we suppose the deal closes: T’s price moves to $100, and the Merger Arb investor books a gain of 7.5% (a $7 return on an initial $93 investment). However, if the deal breaks (Step 3b), T’s price will likely collapse to the pre-deal price of $75, costing the investor $18, or -19.4%. Now, why would any investor do Merger Arb given the asymmetry of a modest gain relative to the risk of a sizable loss? The answer lies in what we call “Expected Return.” As it turns out, Merger Arb deals close more often than not historically, with roughly 90% of announced deals actually closing.2 In our example, we can now calculate a simple Expected Return, given these probabilities. (See the blue box in Exhibit 1, where we multiply the probabilities of winning or losing times their respective gains or losses, or +4.8%. Not bad.)

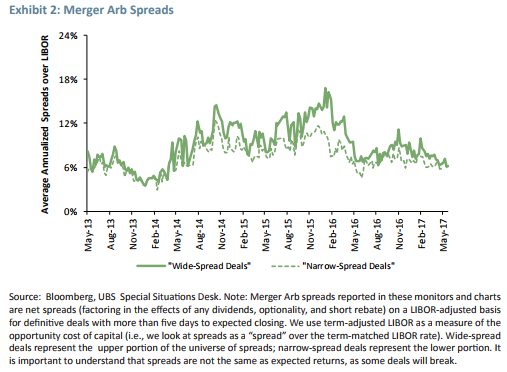

Today, the opportunity set that we see in Merger Arb is quite decent, and very good relative to cash. Exhibit 2 tracks the annualized spreads (over LIBOR) of different collections of announced, or what are called “definitive,” deals. While these spreads can vary through time, today’s annualized spreads look to be in line with those of the past few years, and are in what we might call a decently attractive zone. Okay, we’ve checked the first box.

Little to no sensitivity to the stock market (beta)

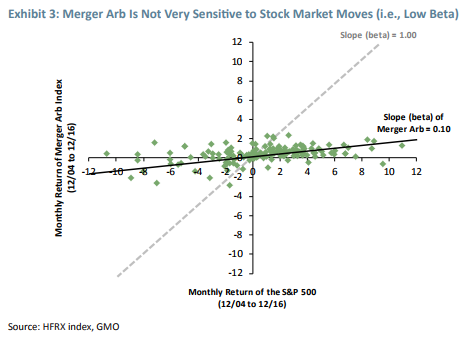

Beta is a measure of how sensitive or risky a portfolio is relative to the broad stock market itself (we’ll use the S&P 500 as a proxy). It turns out that Merger Arb portfolios typically are not very sensitive, i.e., they have low equity beta (see Exhibit 3). Each diamond in the exhibit represents the monthly return of the S&P 500 vs. a Merger Arb index. If Merger Arb returns were similar to the S&P 500 returns, the diamonds would have formed a diagonal-looking line with a slope (beta) of 1.0. A steeper line would mean a portfolio’s return is more sensitive (higher beta) to stock market returns, while a flatter line would mean that the portfolio is less sensitive (lower beta). The Merger Arb line, obviously, is quite flat, with a slope of 0.102, which means it has low beta and low sensitivity to what the stock market does in any given month, whether up or down.

This makes sense: Once a company is “in play,” it stops behaving like traditional equity. It, in essence, swaps its market beta for the particular idiosyncrasies of the merger deal. Those idiosyncrasies will now drive the price movement, not “the market.”

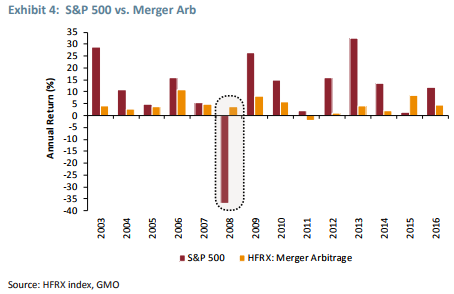

If we needed further proof of this, we could look to how this index performed during a dramatic market move, like that in 2008, when the S&P 500 lost 37%. That same year, the HFRX index actually made a little bit of money.3 Exhibit 4 is just another way of suggesting that Merger Arb has little sensitivity to the movement of the stock market. Let’s be perfectly clear: Merger Arb is not risk-free. If you hire a poor manager who consistently invests in deals that break, or if the economy encounters a catastrophic shock, Merger Arb can be a real problem in your portfolio. But day-to-day, the risk profile of a Merger Arb portfolio is simply quite different from traditional equity beta. Okay, we can check box number two.

Little to no interest rate duration

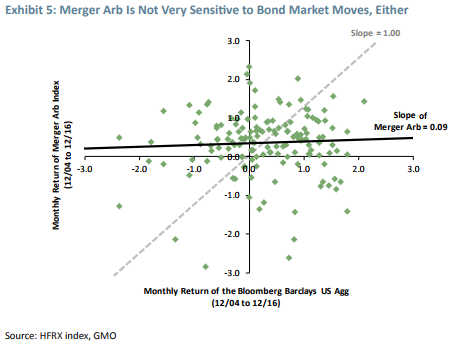

Intuition would tell us that Merger Arb should have very little interest rate duration, as duration is deeply influenced by the length of time of cash flows. Cash flows that occur well into the future have high exposure to interest rate movements, i.e., duration risk. Because most merger deals either close or break in a very short time frame (typically six to nine months), we can safely assume that Merger Arb portfolios have low duration. We can confirm this intuition by measuring the sensitivity of Merger Arb returns to movements in the Bloomberg Barclays US Aggregate Bond index, a common bond portfolio proxy, similar to the exercise we did with the stock market. Exhibit 5 shows the same flat line found in Exhibit 3.

The takeaway is that interest rates can rise or fall during any six- to nine-month time frame, but their movement will have little effect on whether a merger deal goes through or not. Given how historically low interest rates are today (and the higher likelihood that they will begin to normalize), we would prefer strategies that have low duration. Voilá, Merger Arb checks box number three.

Conclusion

In our flagship Benchmark-Free Asset Allocation Strategy, we have made an allocation to our Merger Arb team as part of a larger 20% allocation to alternatives, generally. Most of the traditional asset classes we look at today are looking very – in some cases, even dangerously – expensive. While unicorns are hard to find and no asset class is magically impervious to all risk, Merger Arb looks particularly attractive to us in this environment due to its “unicorn-like” attributes: a decently positive expected rate of return, little to no equity beta, and little to no interest rate duration.

1 For thoughtful commentary regarding our views of duration today please see “The Duration Connection,” a GMO white paper by Ben Inker (July 28, 2016). This paper is available to registered users at www.gmo.com.

2 This 90% number is, of course, a generalization. The incidence of deal closure can vary industry by industry, so the analysis of any Merger Arb deal needs to be extensive (Source: GMO).

3 While the broad index, overall, was seemingly unaffected by the collapse of the equity markets, the Leveraged Buy Out segment of the market did suffer. In addition, some Merger Arb indexes, with slightly different construction techniques, posted losses in 2008 in the -2% to -3% range. The larger message, of course, is that Merger Arb typically does not behave like the stock market. Under extreme economic duress, it is possible that the correlations between Merger Arb and the overall stock market could increase and we could see a collapse of Merger Arb activity.

Peter Chiappinelli: Mr. Chiappinelli is a member of GMO’s Asset Allocation team. Prior to joining GMO in 2010, he was an institutional portfolio manager on the asset allocation team at Pyramis Global Advisors, a subsidiary of Fidelity Investments. Previously, he was the director of institutional investment strategy and research at Putnam Investments. Mr. Chiappinelli earned his MBA from The Wharton School at the University of Pennsylvania and his B.A. from Carleton College. He is a CAIA charterholder, and was the founding President of the CAIA Boston chapter. He is a CFA charterholder.

Disclaimer: The views expressed are the views of Peter Chiappinelli through the period ending August 2017, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Copyright © 2017 by GMO LLC. All rights reserved.

Copyright © 2017 by GMO LLC. All rights reserved.

© GMO

Read more commentaries by GMO