US short-term bond markets could be choppy as Congress seeks to resolve the looming issue

Once again, the US debt ceiling is in focus. Since March, the US Treasury has been employing “extraordinary measures” to fund the US government, such as halting contributions to certain government pension funds and borrowing money set aside to manage exchange rate fluctuations. But those measures are expected to run out this fall.

In late July, Treasury Secretary Steven Mnuchin told Congress that the federal borrowing limit must be raised by Sept. 29 or the US government risks running out of funds to pay its obligations.1 The US Treasury projects that its cash on hand to handle emergencies and other expenses will fall to $60 billion by the end of September —well below its preferred balance of around $300 billion.2

So Congress is, again, being asked to raise (or temporarily suspend) the debt ceiling to allow the US Treasury to issue more debt and continue honoring its obligations. We expect the debate to be contentious. Some Republican House members may demand concessions in return for supporting debt limit legislation, but House Democrats may not go along. Further complicating discussions, the 2018 budget negotiations will also be underway. There may be attempts to link the two issues, either formally or informally.3 Failure to agree on a budget resolution increases the risk of triggering a government shutdown, but we believe this is a low-probability event.

Implications for short-term debt markets

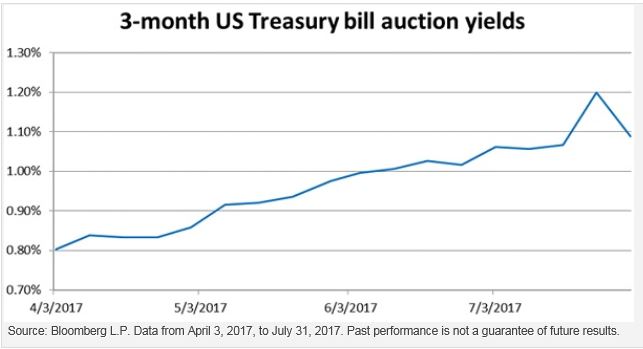

Invesco Fixed Income believes that Congress will likely raise the debt ceiling or suspend it, allowing the US government to resume normal debt issuance and financing activities. However, in the next several weeks, US short-term bond markets could be choppy. We have already seen uncertainty over the debt ceiling manifest itself in the Treasury bill (T-bill) market. Yields on 3-month T-bills maturing in October spiked to 1.18% in late July, as shown in the chart below, inverting the US Treasury yield curve.4 This quickly reversed after Secretary Mnuchin wrote to Congress urging lawmakers to act by the end of September. Yields on T-bills that mature in October remain elevated.

Reduced Treasury bill issuance

As we head toward September, we expect several developments to further impact short-term markets. It is likely that the US Treasury will reduce its issuance of T-bills to provide capacity for the issuance of longer-term “coupon” bonds (maturities of two years or more). T-bills are also the most vulnerable to fears of payment delays, which could pressure yields on October T-bill maturities upward and sharply increase government funding costs. The US Treasury is also likely to increase its issuance of cash management bills (CMB), which have maturities of less than one month.

With resolution of the debt ceiling debate likely to go down to the wire, reduced T-bill supply could exert downward pressure on T-bill yields for maturities that extend beyond October, while October T-bill yields could rise by more than 25 basis points, based on moves seen during previous debt ceiling debates.5 With T-bill supply cuts looming, we anticipate yield declines in the longer segment of the T-bill yield curve.

Once there is a resolution to the debt ceiling issue, we anticipate significant T-bill issuance by the US Treasury. The increased supply of investable short-term securities should provide relief to the market and help alleviate yield compression resulting from the debt ceiling constraints.

Resolution to debt ceiling may be hard-fought

Some politicians and policy makers have suggested prioritizing payments as a way for the US Treasury to manage its obligations without raising the debt ceiling. However, in keeping with his predecessor, Secretary Mnuchin has stated that he has no intention of prioritizing payments, thus putting pressure on Congress to raise the borrowing limit.6

Agreeing to raise the debt limit may prove particularly challenging for a Congress that has struggled to find common ground to pass other legislation. And we know from previous episodes of the debt ceiling debate that using it as a political lever can create financial market disruption and investor uncertainty. Congress faces many challenges, and it has a full agenda that includes health care and tax reform. But at present, Invesco Fixed Income remains optimistic on Congress’ ability to resolve this year’s debt ceiling debate and quell investor concerns.

- Sources: US Department of the Treasury, July, 28, 2017; The Wall Street Journal, July 31, 2017

- Source: US Department of the Treasury, July 31, 2017

- Source: Observatory Group, Aug. 2, 2017

- Source: Treasury Direct, July 14, 2017

- Source: US Department of the Treasury, Sept. 23, 2013, to Oct. 8, 2013

- Debt prioritization is an option, as confirmed by a released transcript of Fed officials during an emergency Federal Open Market Committee conference on Aug. 1, 2011, where it was confirmed that it is technically possible to prioritize US Treasury security principal and interest payments before other government obligations.

Justin Mandeville

Portfolio Manager

Justin Mandeville joined the Invesco Global Liquidity team in January 2015 as a Portfolio Manager, and is involved with the management of short-term Treasury, agency and repo securities.

Mr. Mandeville began his career with Vanguard’s client relationship management group before transitioning to Vanguard’s Fixed Income and Money Market team.

Mr. Mandeville earned his BS degree in business administration from Pennsylvania State University, and his MBA, with a concentration in finance, from Drexel University.

Important information

Blog header image: Vladitto/Shutterstock.com

Past performance is not a guarantee of future results.

Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa.

An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

Treasury securities are backed by the full faith and credit of the US government as to the timely payment of principal and interest.

Obligations issued by US government agencies and instrumentalities may receive varying levels of support from the government, which could affect the fund’s ability to recover should they default.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC, investment adviser. Invesco PowerShares Capital Management LLC (PowerShares) and Invesco Distributors, Inc., ETF distributor, are indirect, wholly owned subsidiaries of Invesco Ltd.

©2017 Invesco Ltd. All rights reserved.

The US debt ceiling saga returns by Invesco